Simon Derrick is a managing director of BNY Mellon and is head of its markets strategy team. Simon established the team more than 10 years ago and developed it into a preeminent center of excellence within BNY Mellon. His views on currency policy matters and on developments within the euro zone are frequently quoted in the financial media.

I spoke with Simon on February 14.

You’ve said that easy money policies in developed markets – the U.S., Europe, Japan and the U.K. – led to capital flows into emerging markets, a process that is now reversing. Was the Fed’s tapering the trigger to that reversal, and can you elaborate on how you see that reversal unfolding?

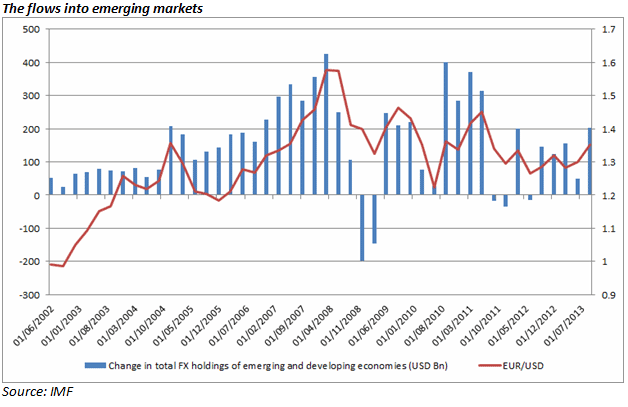

It's always hard to make the explicit connections. However, one of the things that is very apparent is that we have run easy-money policies since 2002. One of the simplest ways of measuring that is to look at the average Fed-funds rate versus average headline-inflation rate. It is clear that since the institution of those policies there have been substantial flows into emerging markets. One measure is to have a look at the increase in foreign-exchange reserves in the emerging markets, which have gone from $800 billion at the start of 2002 to something like $7.75 trillion at the end of the third quarter of last year.

Fed tapering will lead to a slowdown of flows into emerging markets. At the start of this year, the World Bank estimated that since 2009, approximately 60% of the inflows into emerging markets had been driven by international factors. It very pointedly included the story of U.S. interest rates as a catalyst. If I look at flows in recent times, since the introduction of QE, you can see that when an additional program came along, more often than not, is when you see an increase in foreign-exchange reserves.

If we are moving towards tapering, then that will have a fairly direct impact on sentiment in certain emerging markets. Bernanke started talking about asset bubbles on May 10 of last year, and then in his testimony to Congress, which was on May 22 of last year, and that was when the discussion of tapering began. That was almost exactly the point problems started in a number of emerging-market nations, and that continued through July and August.

On July 1 of last year, Stanley Fischer gave an interview to the Financial Times. He said, “Look, we expected pressures to emerging markets in the aftermath of what we did. We aren't particularly surprised.”

Looking at this year, the fresh pressures that formed in the emerging world began at the end of December, almost exactly at the point the Fed was getting ready to start tapering its purchases. Now, that may well have been a knee-jerk reaction rather than a direct impact of the slowdown of growth in the money supply, but nevertheless that was when the pressures in emerging markets started.

What will be the impact of tapering in the emerging markets?

For the majority of the emerging world, there have clearly been upward pressures on their currencies over the course of the last few years, which a lot of them disliked. So easing of those pressures allows their currencies to move back to what they would consider to be fair value, which is a good thing, not a bad thing.

The emerging markets are in a far stronger position than they were 15 years ago. One simple example of that is that they have $7.75 trillion of reserves to defend their currencies and ease their path on the way down. We should not be talking about this as being a crisis. It's far more about the easing of pressures – that were possibly unwarranted – within the emerging markets.

Some nations, though, clearly have issues. What’s been interesting is that over the course of 2014 so far, the nations which have seen their currencies come under pressure were Argentina, Brazil, Turkey, South Africa and Russia. This is the group that found their currencies under pressure in the run up to 2002, when monetary policy eased in the West.

It is almost as if some people started to contemplate the tap being turned off. They suddenly started to look at the structural issues a lot of those nations faced, asked whether any real material changes had taken place and where they haven't they reduced their risk in those countries. We know Russia remains heavily commodity-dependent. The same is probably true for South Africa. Turkey has domestic political issues that have continued to surface over the last 12 months.

What is even more telling, though, is that the one nation that was in crisis back then, but quite clearly isn't at the moment, is South Korea. South Korea did reform its economy over the last 15 years. It made a very conscious effort to move away from being a low-cost alternative to Japan to move further up the food chain. Samsung is the most obvious example of that. You don't talk about Samsung as being a low-cost alternative to Sony; it is a direct competitor to Apple. That is a measure of how they've changed. The facts that that occurred and you had that structural shift in the South Korean economy are very clear reasons why it's no longer in the group that it was in 15 years ago.

Many analysts are concerned that there could be a repeat of the Asian crisis of 1997. What do you see as the likelihood that that could actually happen, and what would the conditions be that could potentially lead to that?

I don't think we are going to have a repeat of 1997. For one thing, we don't have the same level of dollar-denominating debt that was such an issue back then. The other huge difference is that today you have this phenomenal level of reserves with which these nations can protect their currencies.

Now, they clearly have to be sensible in the way they use those reserves. Drawing a line in the sand rarely helps. But ensuring that the markets have adequate liquidity and giving investors confidence that things won't go radically wrong should there be a decline and they want to get out puts those countries in a far better position.

There are things that nag away, though. The one great unknown, of course, remains China. It's a command economy. We see these very clear attempts to reform the economy under the new politburo. That is very encouraging, but the country still has this massive debt overhang. That is of concern. We want to make sure that that gets handled well and there aren't any major issues. I'm sure the government will do it and they will have a soft rather than a hard landing.

But over the course of this year, if there is anywhere within the emerging world we have to keep a close eye on beyond that initial group, it is what is happening in China.

Genuinely, I am an optimist. I think China will also move towards having its currency float without any major problems, but it is a fairly substantial task that it faces. We need to recognize that.

How successful will Japan be in its quest to devalue the yen?

Well, quite clearly Japan would deny that its policy of quantitative easing is designed to weaken the yen. It has been very careful to come out time and time again to make that point. The one thing that contradicts that was some of the comments Mr. Abe made before he became prime minister. In November 2012, he said he wanted to work very closely with the Bank of Japan to help weaken, or at least get a more competitively priced, yen. Those comments say there was definitely a desire to have a more competitively priced currency.

How successful will it be? Well, it is questionable, because for a sustainable move to take place, you need to actually see investors going out and selling yen. One of the things that's not been surprising, but on the surface is a little surprising, is that during 2013, Japanese investors didn’tput money into overseas markets, particularly overseas fixed-income markets. Those data come from Japan’s ministry of finance.

If you think about it for a second it makes sense, because the big yield pickups that were available 10 or 12 years ago simply no longer are. The interest-rate differentials are far narrower. Of course, Japanese markets have been performing far more positively. So Japanese investors have taken the rational view of, why try and pick up small interest-rate differentials in the U.K. or Europe and have the currency risk when they can stay at home and have a healthy return from the Nikkei or from the local housing market? So they haven't necessarily been big players.

International “real money” investors were probably sellers of yen in the early parts of 2013, to reduce the currency risk on the Japanese assets they had. There probably was not a great deal of selling of the yen from that community the second half of the year. In contrast, if you look at the data that came out from the futures markets – the CFTC data – it suggested that by the end of last year, the leveraged community had the largest short-yen position that they've had since summer of 2007. That tells me that the latter stages of the yen's move last year were driven by hot money and more speculative flows. If we did have a little more of a risk-averse environment, you could see money flow back into Japan. That could come as a little bit of a surprise, if in the opening months of 2014 there is a surprise appreciation in the yen.

Will Japan continue to successfully weaken of the yen? The jury is out.

Let's switch to a different part of the world. Many people believe the euro now is at an unsustainably high level. What has been propping up the value of the euro and how do you see that exchange rate moving in the future?

There are several factors. One is the shift in focus within the investment community over the last two years away from opportunities in the emerging world to those in the developed world. That has been a very noticeable shift. It is understandable when you see the forecast that came from the World Bank, which said the best economic growth relatively speaking is going to come in the developed markets in 2014. As part of that, there has definitely been a shift toward euro-zone equities, for example. We see that when we look at our own data.

Beyond that, the most obvious thing that has helped keep the euro at these high levels is simply the fact that monetary policy within the euro zone remains relatively tight. We have an ECB that continued not to move on policy despite the fact that levels of inflation continued to decline. From that perspective, it has been a yield play more than anything else that has kept the euro where it is. Perhaps the way that has been expressed most clearly is simply the fact that within the peripheral euro zone – whether we are talking about Portugal, Spain or Ireland or mainstream Italy — you still have a reasonable yield differential over and above core Europe, or indeed over and above a large part of the rest of the developed world. There is still an interest-rate spread that people can pick up. Perhaps more than anything else, that explains why we have a euro where it is today.

I am concerned for two reasons. Monetary policy for the euro zone is too tight relative to its needs. Headline inflation is just not 0.7% for the region. If you get to the peripheral countries, it is flat, and in Greece you are actually talking about deflation. That is not necessarily a positive backdrop for a region that is struggling at the margins. The core numbers are continuing to improve but once you start to look beyond Germany and the other core nations there are still an awful lot of problems.

There is a need for looser monetary policy. I just don't think we are going to see it yet.

The other concern is the yields on the peripheral euro-zone debt are starting to come down to the levels of German and French debt. We have moved to a world where the risk premium is relatively modest. It's moving very close to where we were in 2009. That concerns me because one of the main causes of the euro-zone crisis, if you'd like, was that people didn't price risk appropriately. More succinctly, they didn't take into account the lack of a fiscal union. For example, in 2007, there was no difference between the yield on Spanish and German debt. Yet clearly there should have been, because there was greater risk for Spanish than for German debt. What worries me is that we are forgetting the lessons of 2010 and 2011, and forgetting that Europe is still not a fiscal union. This isn’t going to be an immediate issue; it is nevertheless a problem that suggests that we are under-pricing risk within Europe at the moment.

What do you see happening now in the oil markets and how will that play out in the currency markets?

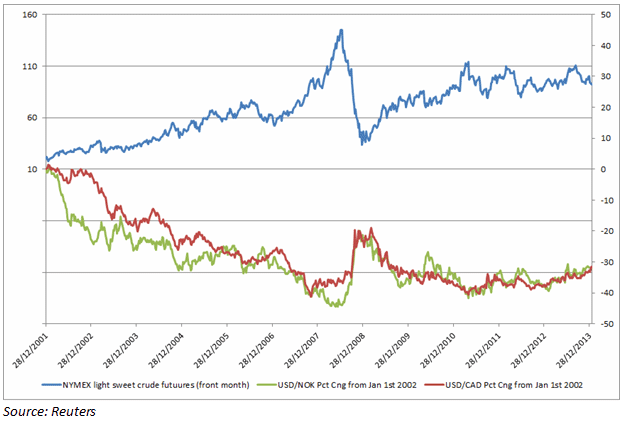

Certain currencies over time have naturally tracked oil prices – the Canadian dollar, the Norwegian krone and the Russian ruble. It’s entirely reasonable that those currencies would follow oil closely.

All three of those currencies have had a degree of pressure on them over the course of this year so far. In the long run, oil prices should head lower. The arguments for that are relatively straightforward. Clearly there are some specific supply issues in places like Libya and Iraq. However, the fact that sentiments towards, or relations with, Iran are starting to ease in the longer term opens up the possibility of Iranian oil being available to the West. The reports at the start of this year that the Iranian oil minister had been talking to the major Western oil companies were a positive for supply. We know that the demand growth in China has been slowing steadily. It's still increasing, but at a far slower pace than three or four years ago. We know the improving story on energy production in the U.S. — this year there was even talk for the first time since the early 1970s of allowing U.S. oil to be exported. You have this fantastic increase in production.

All those things say to me that over time you should expect to see oil prices that are closer to $70 a barrel than $95 a barrel. The only issue is that oil prices over the last six or seven years have been somewhat sensitive to monetary policy.

The good news is that we are tapering here in the U.S., and that should lead to slightly lower oil prices. But the flipside is Japan, where we've already had one round of QE and we might possibly have another round later in the year. Monetary conditions overall still remain pretty easy throughout the developed world, and that is why things like oil and other commodities aren’t as weak as we might expect. But if we look beyond the short term, we should be looking at lower oil prices. As a reflection of that, things like the Canadian dollar will continue to weaken, but not at a fast pace – a slow steady decline to maybe 1.15 or 1.20 is entirely reasonable. Similarly, I expect the ruble to remain under pressure. The Norwegian krone will gently decline.

The direct relationship between monetary policy and oil prices

The indirect relationship between monetary policy and oil prices

As long as the dollar maintains its status as the reserve currency, will it remain strong against all other major currencies in the long term?

That’s quite an interesting question, because the dollar’s role as a reserve currency has declined slightly since 2002 in percentage terms. The IMF produces a quarterly report that tells you about the growth in reserves and, to an extent, how countries used their reserves. You can get a partial picture of what emerging-markets nations are doing with their reserves. But if you look at that data, the percentage that they've kept in the dollar has fallen from around 75% to somewhere close to 60%.

But you've also got to remember that in absolute terms, their holdings of dollars have gone up, because their reserves have grown so much.

We have moved to a multi-reserve-currency world, but it is hard to see a continued meaningful shift away from the dollar. Plenty of other currencies have their own major issues with regard to being reserve currencies. We've already seen the unwarranted or unwanted strength of the euro. Others are not large enough in terms of liquidity to be credible major alternatives to the dollar.

In terms of what it means for the performance of the dollar, the dollar has declined 30% against the trade-weighted basket of currencies over the course of the last 20 years while being a major reserve currency. Reserve status didn't make that much of a difference at the end of the day.

Over the course of the next few years, though, I am a dollar bull. That's because the U.S. is ahead of the curve relative to the rest of the world in terms of economic recovery. I like the fact that we've had the oil story. That makes a major difference to the deficit and to energy independence. We have a Fed that has said quite explicitly they're concerned about asset bubbles. That's great. I like the fact that it’s worried about that kind of thing. Over the course of the next few years I would expect to see the dollar gently strengthening.

Read more articles by Robert Huebscher