Last week’s data reaffirmed that inflation pressures remain the defining narrative across the economic landscape.

When we talk about inflation, the conversation usually centers on periods (like now) when inflation is especially high. But we can overlook a possibly bigger problem: other than a few short breaks, you and I have never seen a time when inflation wasn’t rising. Inflation isn’t some problem that pops up occasionally. Inflation has become normal – so normal we let it accumulate for years without complaint.

The AI boom goes from strength to strength. Big technology companies are pouring hundreds of billions of dollars into chips, data centers and power-hungry infrastructure. One estimate puts annual AI infrastructure investment above $650 billion in 2025 and potentially over $800 billion in 2026..

Model portfolios have helped many advisors solve for scale. The next challenge is more nuanced: how do advisors keep that scale while delivering more personalization, tax awareness and differentiated value to clients?

Before your firm starts using AI across operations, client service, reporting, or advisor workflows, there’s one basic question leadership needs to answer: what kind of AI are we talking about?

Investors now have more optionality when looking for Nasdaq 100 exposure. State Street Investment Management (SSIM) just launched the State Street SPDR Portfolio Nasdaq 100 ETF (QNDX). It will invariably go heads up with the Qs, namely the Invesco QQQ ETF (QQQ) and the Invesco NASDAQ 100 ETF (QQQM).

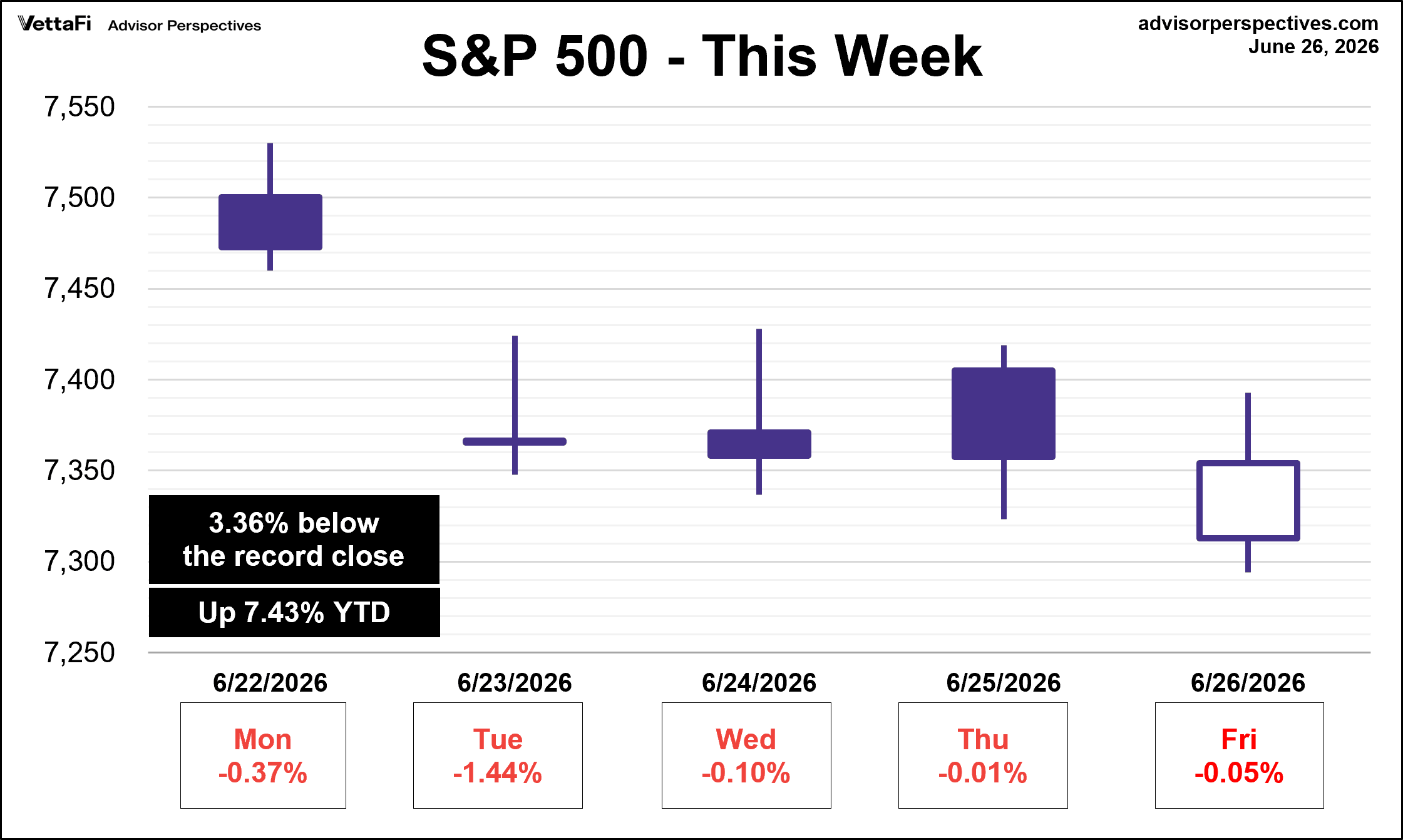

The S&P 500 fell every day this week, its longest losing streak since last August. Ultimately, the index closed the week down 2.0%, marking its first decline in three weeks.

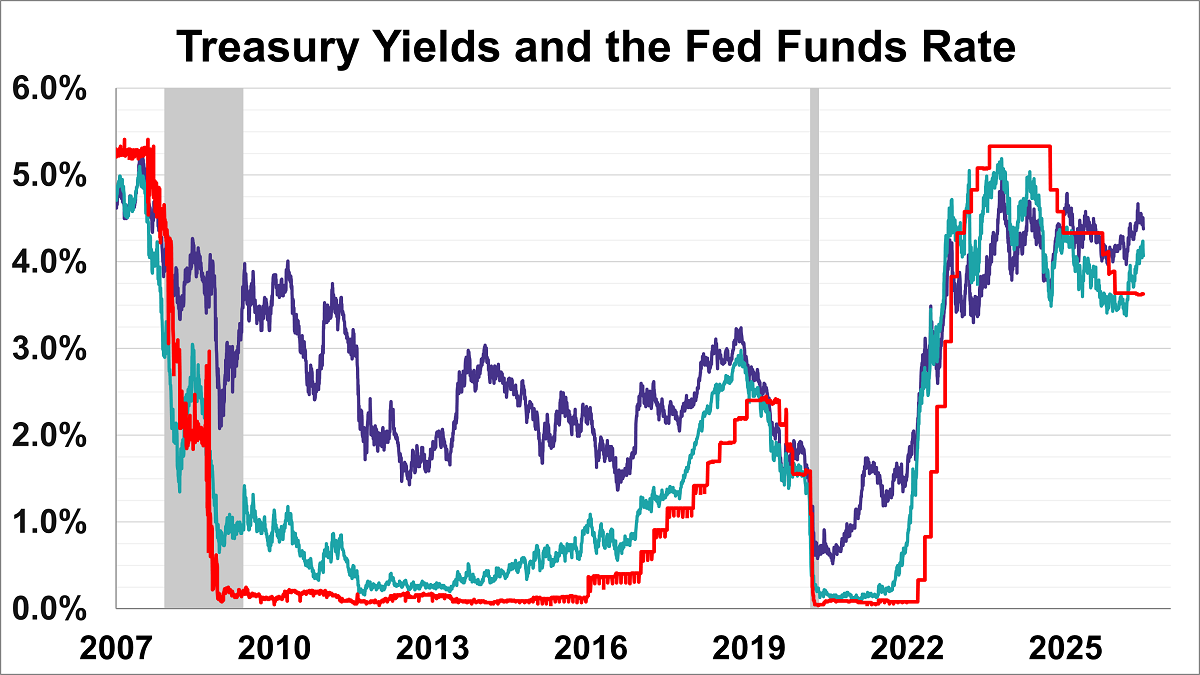

The yield on the 10-year note finished June 26, 2026 at 4.38% while the 2-year note ended at 4.07%.

GraniteShares and VettaFi are coming together for a state-of-the-category briefing: the flow data behind the surge, the structural reasons advisors are making room in income sleeves, how the category has held up across different rate and volatility regimes, and the diligence questions worth asking before adding it to a model.

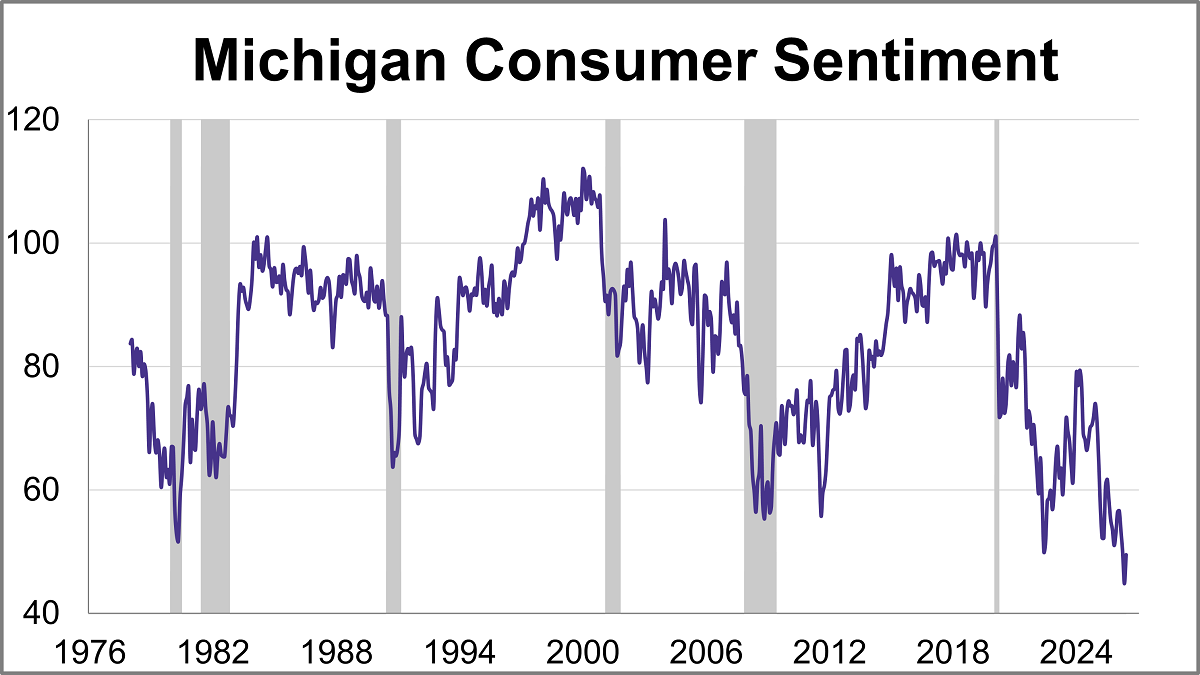

Consumer sentiment improved for the first time in four months as gas prices eased but remains historically low amid ongoing inflation concerns. The final June reading for the University of Michigan Consumer Sentiment Index came in at 49.5 marking a 10.5% (4.7 points) increase from April and beating the expected reading of 48.9.

This roller-coaster week for tech stocks from Seoul to New York fueled by extreme investor positioning and worries over chip demand is sending a strong signal: the case for the artificial-intelligence trade is still strong, but the days of everything going up in a straight line appear to be over.

The dollar is wrapping up one of its best months in a year as a raft of Wall Street banks see a turnaround of fortunes for the US currency.

SpaceX’s blockbuster bond sale is weakening so quickly in the secondary market that traders say they can’t recall another recent deal that widened this sharply.

Bitcoin’s collapse is forcing crypto veterans to confront the question every bear market eventually asks: when does mass panic create a buying opportunity? The answer, according to many of the investors and analysts who have lived through previous boom-and-bust cycles, is: not yet.

Private credit is having a moment in the headlines. Higher interest rates and a pullback in certain types of bank lending have pushed more financing activity into private markets. Investors may be left with a simple question: What exactly is private credit?

In a world of high starting yields and rupturing economic alliances, investors who actively diversify across regions, sectors, and currencies can be better positioned to pursue durable returns.

As the market continues to broaden in 2026, a balanced approach matters more than ever.

AI is both a foundational technology and the ultimate replacement product, which we believe explains why it has attracted unprecedented levels of capital and why the investment opportunities are so compelling.

New Fed Chair Kevin Warsh is already reshaping policy communication by reducing forward guidance, questioning the dot plot’s future and emphasizing real-time data, potentially increasing Treasury market volatility.

JPMorgan Chase & Co. named Troy Rohrbaugh and Doug Petno co-presidents as the abrupt departure of consumer banking chief Marianne Lake marked another twist in the race to succeed Chief Executive Officer Jamie Dimon.

Kevin Warsh, the newly appointed Federal Reserve chair, led his first committee meeting in June. The decision to leave short-term interest rates unchanged didn’t surprise anybody, but there was plenty for markets to chew on. Warsh seems likely to make structural changes that may not impact near-term monetary policy but could matter much more to the US economy over the long run.

Halfway through 2026, this market perspective is harder to write with confidence than most. That’s not a phrase I use lightly. Over four decades of markets, there have been plenty of uncertain moments, but the number of significant, unresolved issues I’m watching right now is unusually high.

The ETF landscape includes plenty of exciting ETFs. Not all, however, can claim to combine high current income and outperformance. The ProShares Russell 2000 High Income ETF (ITWO) has done just that so far this year with its innovative approach to covered calls.

VettaFi currently has index products tied to ETFs issued by American Century, Victory Capital, and ALPS ETFs, but the addition of RAFI products issued by Invesco and PIMCO that are fundamentally weighted is really exciting, according to Rosenbluth.

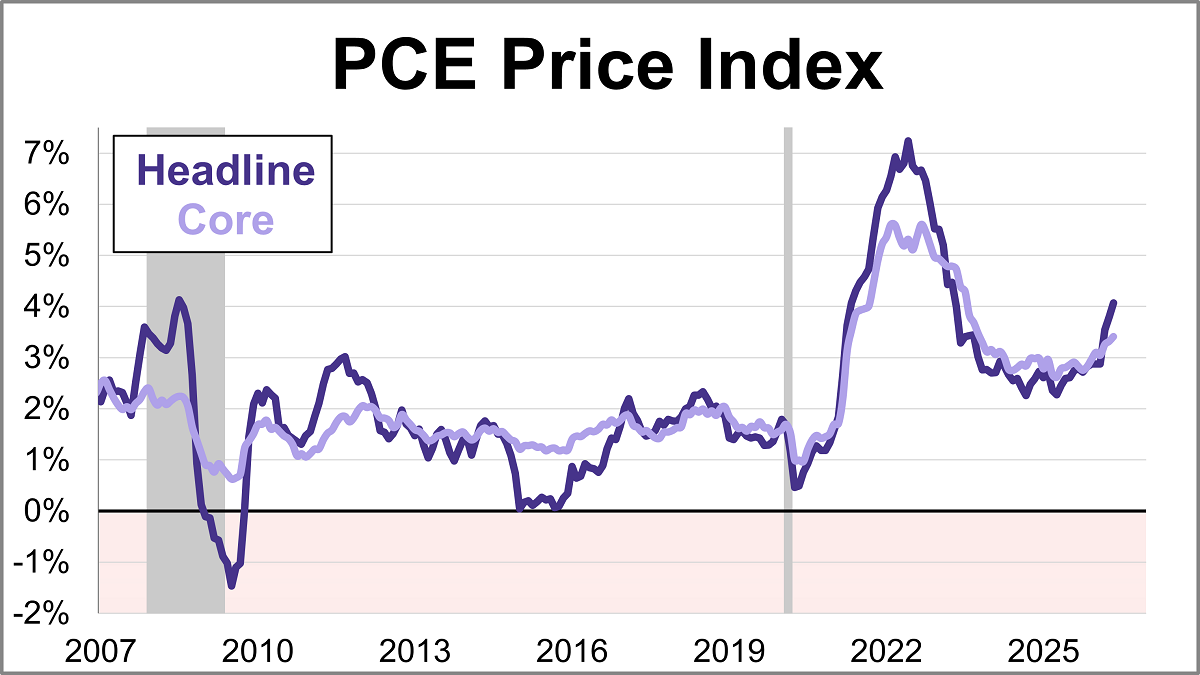

The Federal Reserve’s preferred inflation gauge, the core PCE price index, climbed 3.4% year-over-year in May. This marks the highest level since October 2023 and marks a pickup from April's 3.3% reading. On a monthly basis, core prices rose 0.3%.

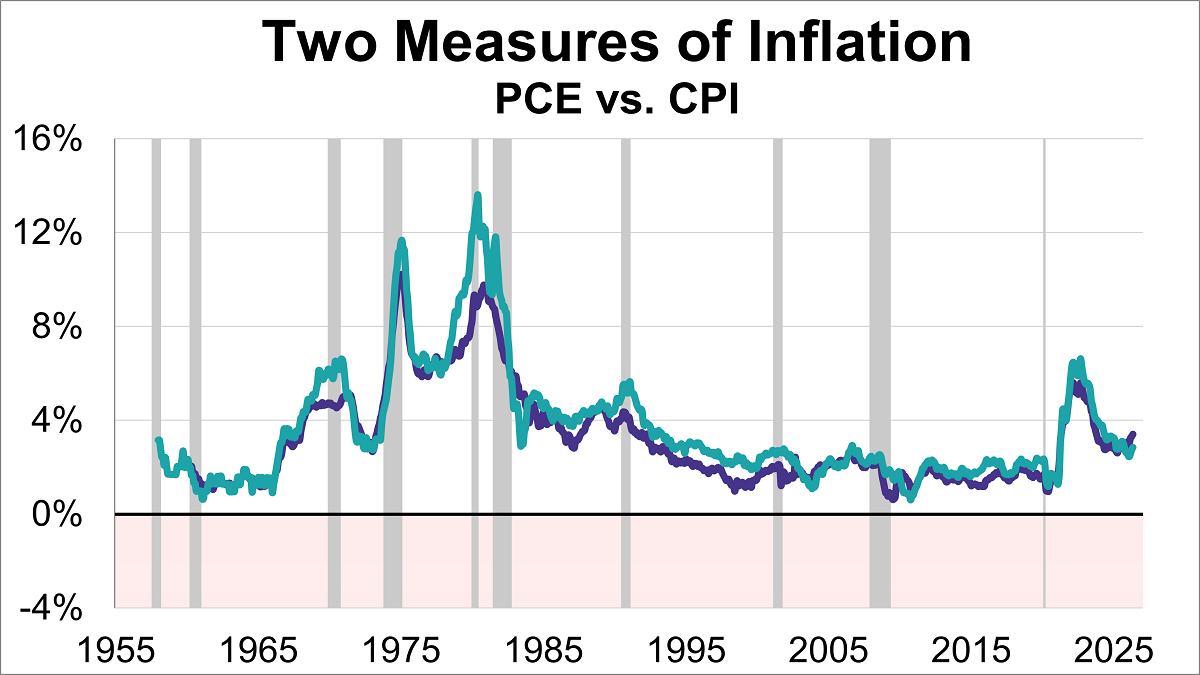

Inflation remains a hot topic, directly impacting everything from your grocery bill to interest rates. As of the latest data, two key inflation gauges — the Personal Consumption Expenditures (PCE) Price Index and the Consumer Price Index (CPI) — show that prices are still above the Federal Reserve's 2% target, with the core PCE at 3.4% and core CPI at 2.9%.

What if the debt crisis investors have feared is not still ahead, but already here, unfolding in plain sight? In his June insight, Richard Bernstein, Global Head of Macro & Customized Investing, makes the case that the market may already be penalizing U.S. fiscal excess, not through a dramatic collapse, but through a slow burn with real consequences for investors and the broader economy.

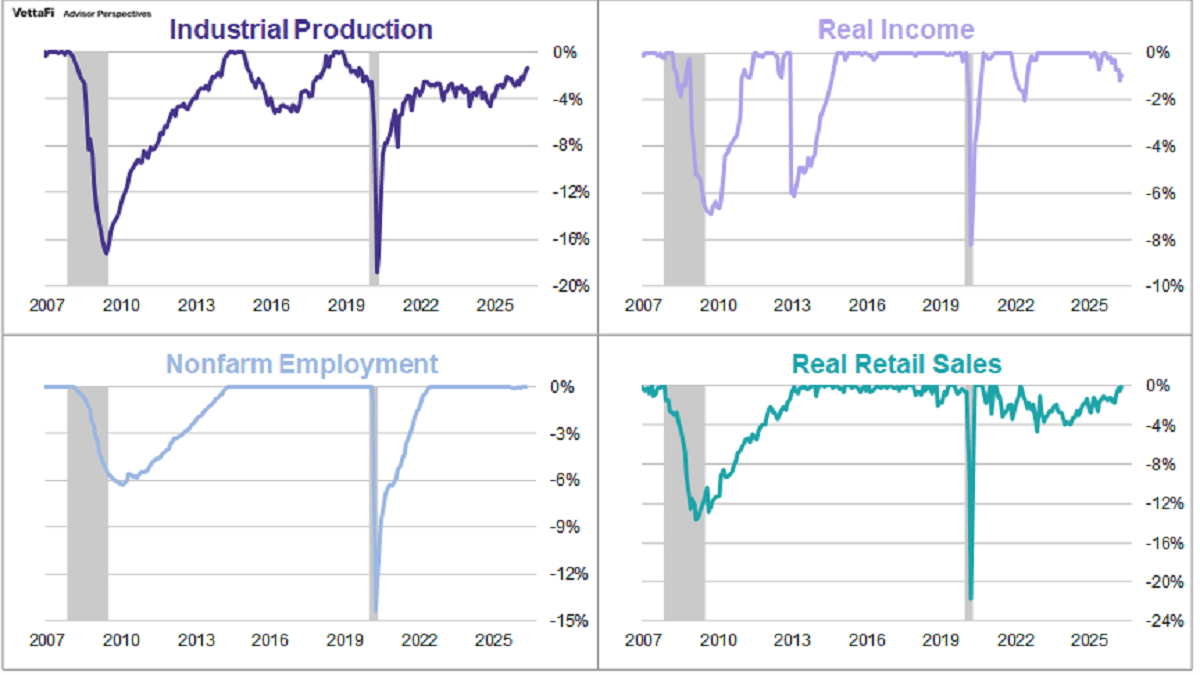

Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process.

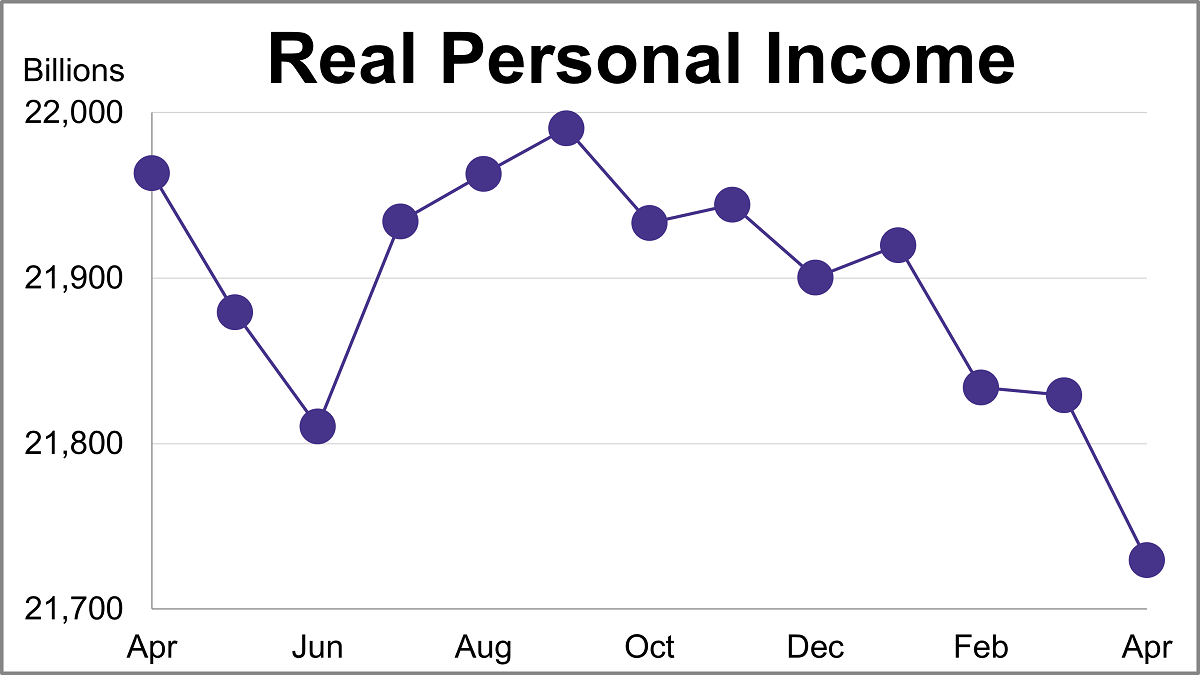

Personal income (excluding transfer receipts) was up 0.70% in May and was up 3.62% year-over-year. However, when adjusted for inflation using the BEA's PCE Price Index, real personal income (excluding transfer receipts) was up 0.25% month-over-month and down 0.43% year-over-year.

Market professionals already on edge about the staying power of soaring artificial intelligence stocks are starting to grapple with another risk: public anger toward the technology.

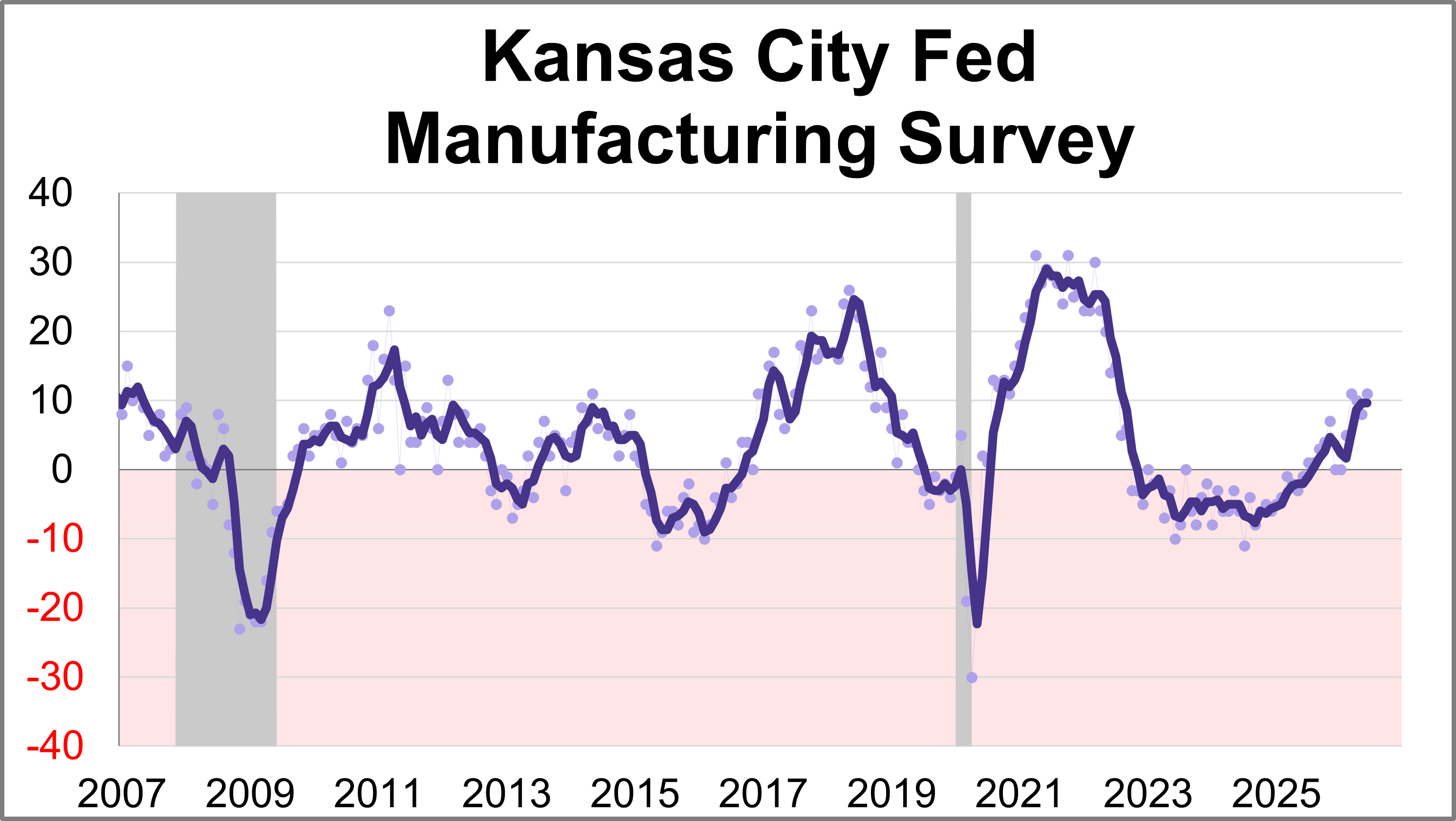

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

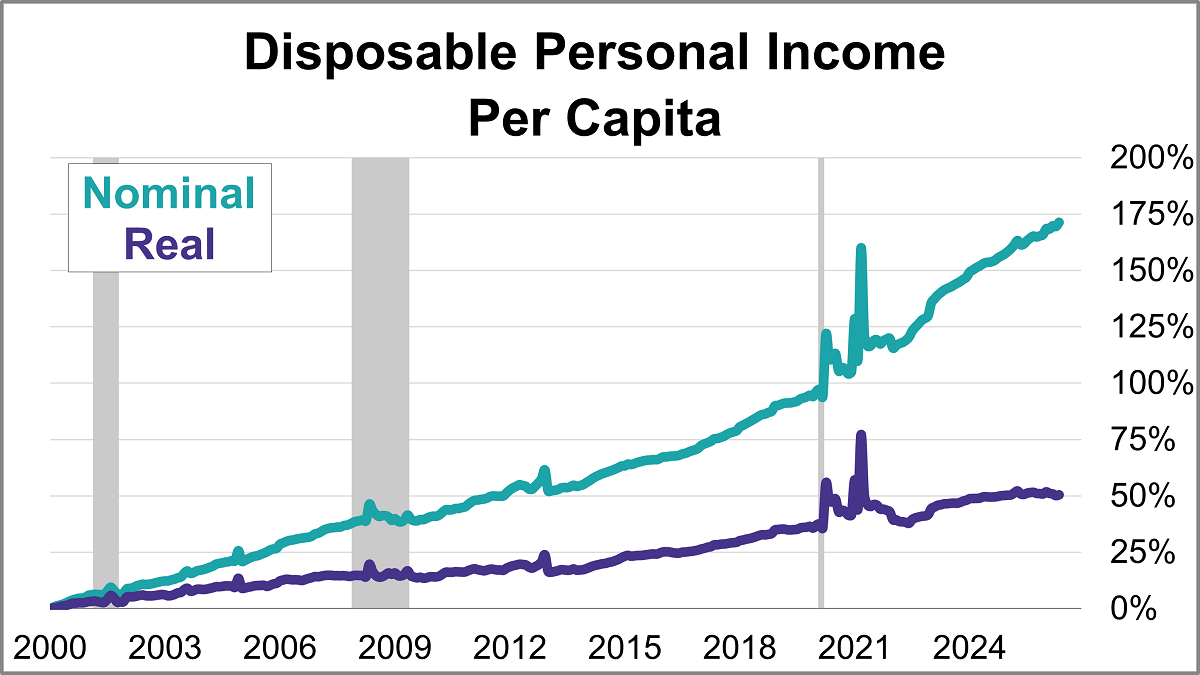

With the release of May's report on personal incomes and outlays, we can now take a closer look at "real" disposable personal income per capita. To two decimal places, disposable income per capita was up up 0.68% month-over-month. But when adjusted for inflation, real disposable income per capita was up 0.23%.

Join the industry’s leading strategists for the Midyear Market Outlook Symposium—a comprehensive briefing designed to help advisors audit their current allocations and prepare for the opportunities of the next six months

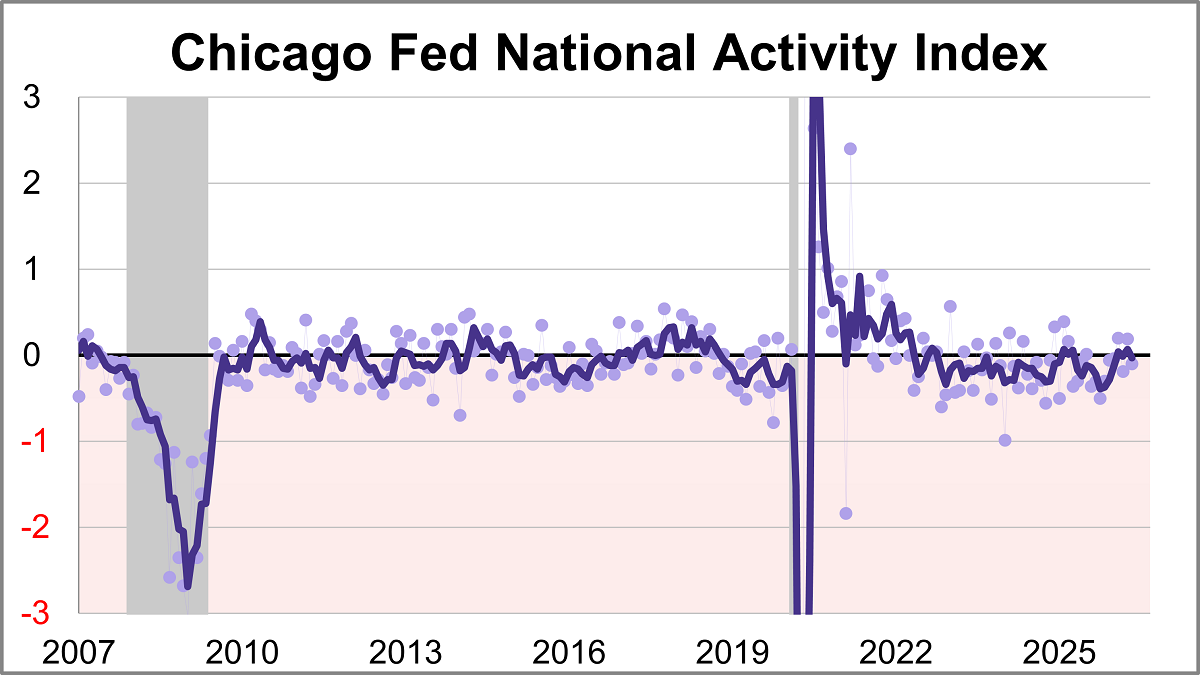

The Chicago Fed National Activity Index (CFNAI) fell to -0.10 in May from +0.19 in April. Two of the four broad categories of indicators used to construct the index decreased from April, and three categories made negative contributions.

President Donald Trump signed executive orders Monday aimed at accelerating quantum research, laying the groundwork for federal agencies to adopt the technology and strengthen US defenses against cyberattacks.

Alphabet Inc.’s addition to the Dow Jones Industrial Average marks another step in the benchmark’s effort to catch up with a market increasingly defined by Big Tech.

With back-to-back announcements this week, SK Hynix Inc. and Micron Technology Inc. have solidified the memory chip market as the hottest part of the AI industry.

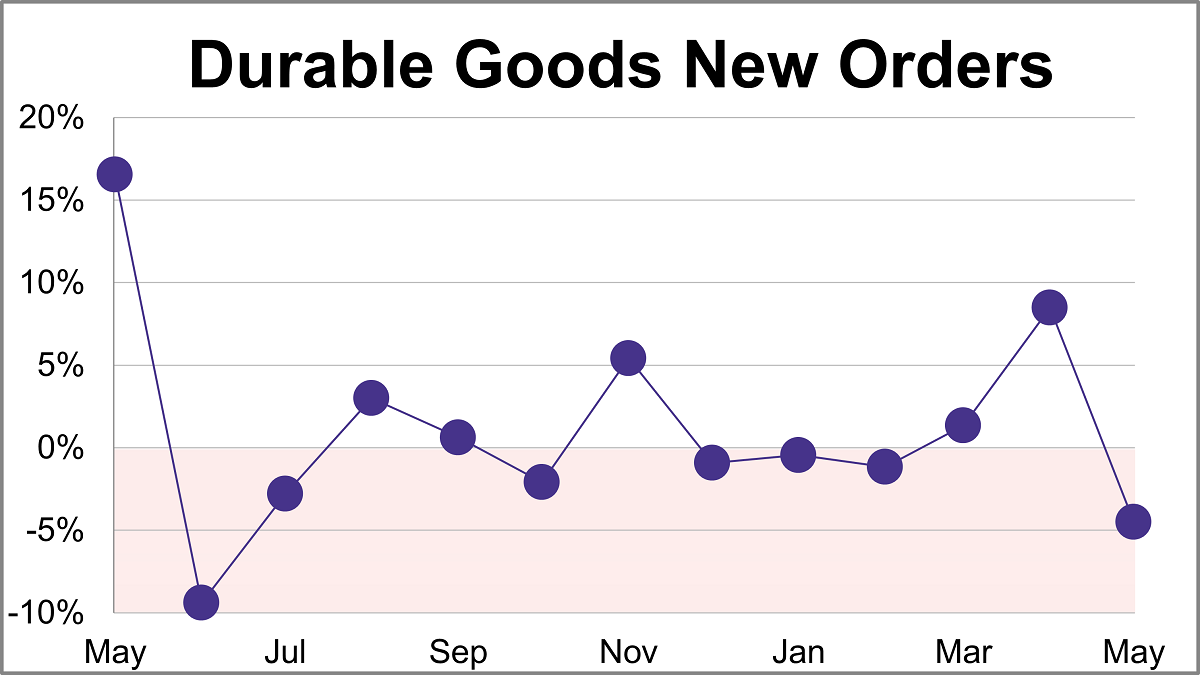

New orders for manufactured durable goods sank 4.5% in May to $332.05B, slightly less than the projected 5.0% monthly decline.

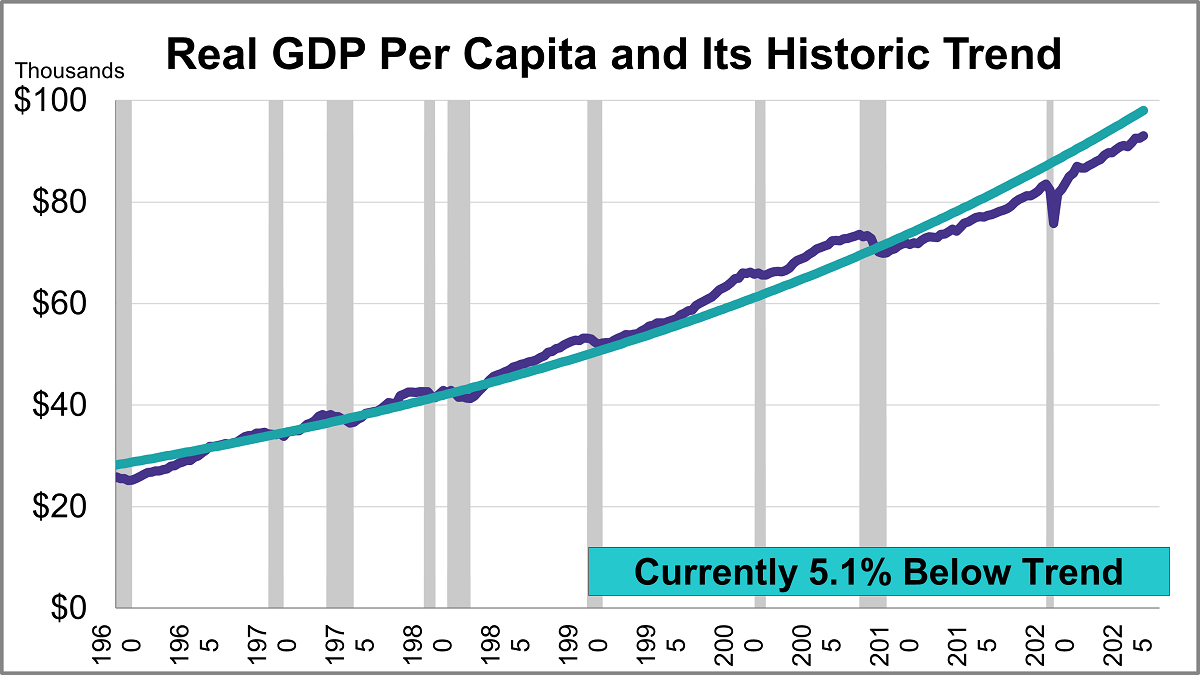

The third estimate for Q1 GDP came in at 2.09%, an acceleration from 0.48% for the Q4 final estimate. With a per-capita adjustment, the headline number is lower at 1.91%, a pickup from 0.18% for the Q4 headline number.

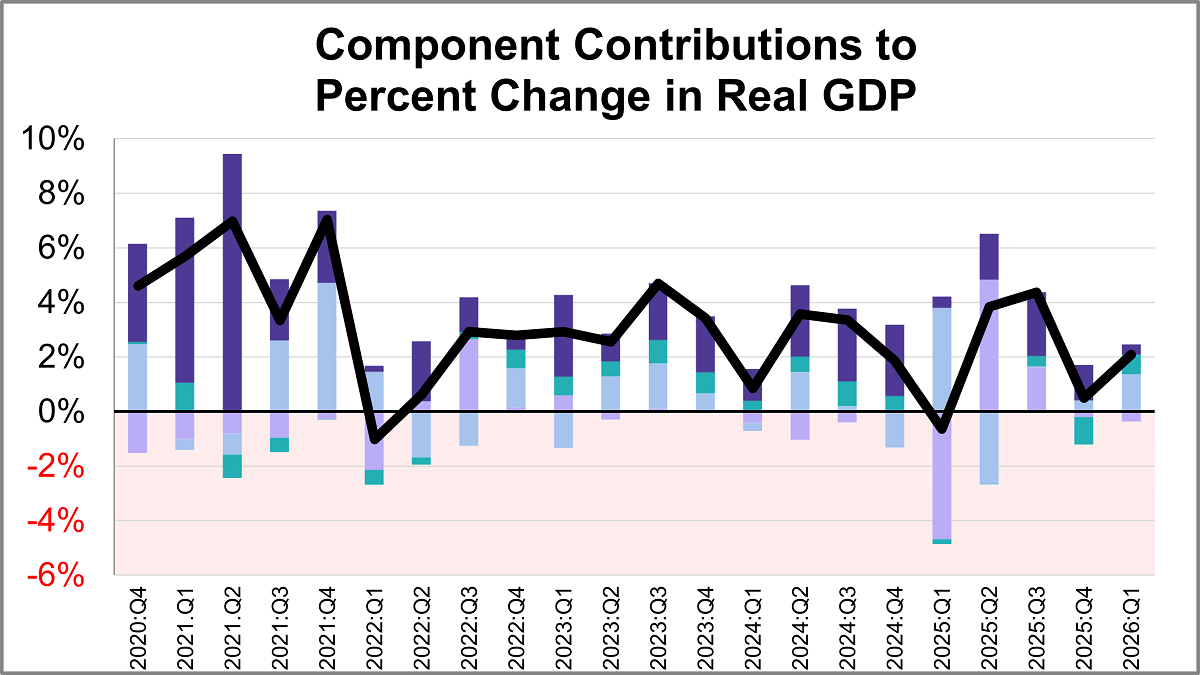

Real gross domestic product (GDP) is comprised of four major subcomponents. In the Q1 2026 GDP third estimate, three of the four components made positive contributions.

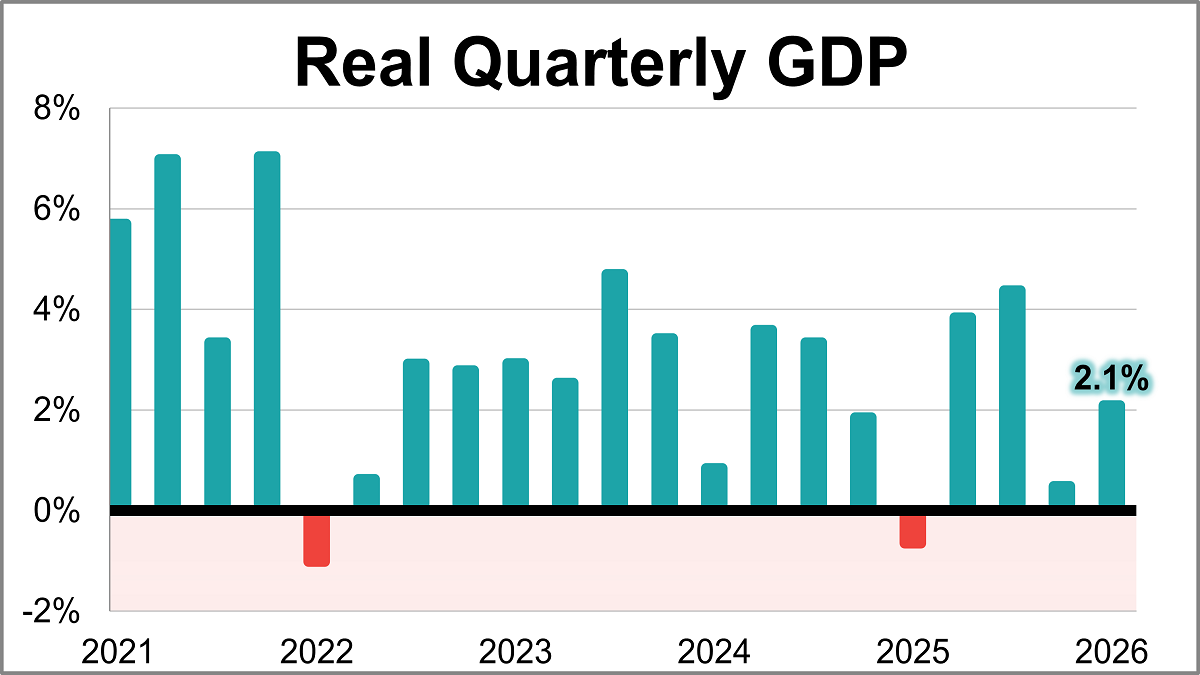

U.S. economic growth rebounded at the beginning of 2026, according to the BEA’s latest estimate. Real GDP rose at a 2.1% annual rate in Q1, exceeding the 1.6% forecast and marking a sharp acceleration from the 0.5% final estimate seen in Q4 of last year.

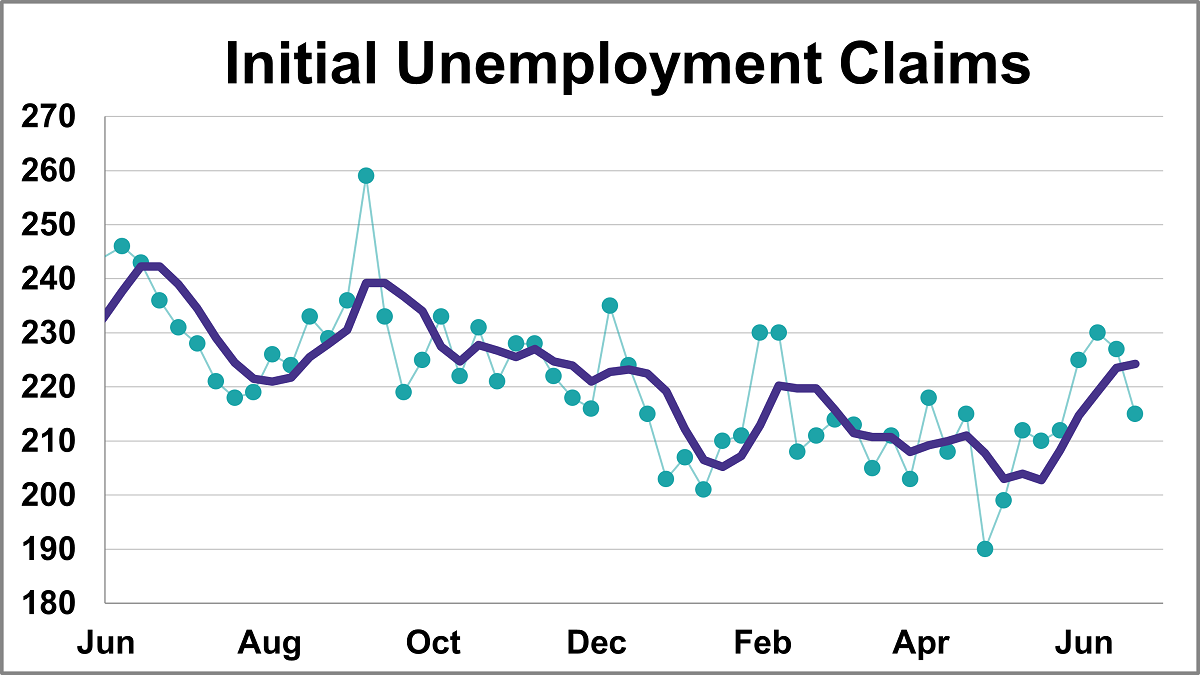

In the week ending June 20th, initial jobless claims were at a seasonally adjusted level of 215,000. This represents a decrease of 12,000 from the previous week's figure and was lower than the forecast of 225,000.

Federal Reserve Chair Kevin Warsh is changing how the central bank conducts monetary policy. A fresh look is appropriate, especially given the Fed’s failure to achieve its 2% inflation objective for more than five years. But this needs to be done with greater care than Warsh has shown to date.

According to Gleason, the freezing of Russian assets following the 2022 invasion of Ukraine accelerated the global push toward de-dollarization. Nations around the world took notice that access to the dollar-based financial system could be restricted, increasing the appeal of gold as a reserve asset that cannot be frozen or sanctioned by foreign governments.

Kevin Warsh’s first Federal Reserve meeting as chair mattered less for the rate decision than for what he revealed about how the Fed intends to operate. Warsh signaled a shift toward less guidance and more flexibility.

On May 5, 2026, researchers from Cleveland Clinic, RIKEN, and IBM successfully simulated a 12,635-atom protein complex using quantum-centric supercomputing, a problem relevant to drug discovery that classical computing could not match at comparable speed and accuracy.

Municipal bonds often see a seasonal lift during the summer months. This pattern, known as summer technicals, stems from a straightforward supply and demand imbalance that tends to favor bond prices. Over the past ten years, the summer months (May through July) have generally been positive months for the Bloomberg Municipal Bond Index, with monthly returns averaging +0.83%, +0.43%, and +0.82%, respectively.

Total-portfolio thinking is gaining momentum across institutional investing, with investors looking to adopt portfolio-wide approaches that integrate risk, liquidity, and capital allocation decisions. As institutions manage broader opportunity sets and place greater emphasis on portfolio integration, total-portfolio thinking is increasingly influencing how they set objectives, allocate capital, implement strategies, and govern portfolios.

The international ETF landscape has become quite popular with investors over the last year. Investors flocked to ex-U.S. equity opportunities over the last 12 months, driven by high domestic valuations and persistent concentration risk. By contrast, emerging and international markets have both offered lower costs and healthy diversification.

In a digital-first environment, reputation is no longer a byproduct of success; it is an asset class in its own right. For ultra-high-net-worth families, reputation capital can influence investment opportunities, business partnerships, philanthropic impact, and multigenerational legacy. It can also be exposed, amplified, or undermined in real time.