Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

There is considerable evidence that high-dividend equities have significant advantages for growing income and wealth. In particular, a high-dividend-equity strategy addresses three major income concerns: getting sufficient yield, keeping up with inflation and outliving available funds. Such a portfolio produces higher income per dollar invested, growing income and principal over time, higher total returns, lower volatility and a reduced risk of outliving savings. I will address each of these advantages separately.

Higher income per dollar invested

A high-dividend-yield portfolio can produce two to three times the income per dollar invested versus a traditional low-default-risk bond portfolio. This means a smaller portion of an investor’s portfolio is dedicated to income generation. For example, a $1 million portfolio invested in 10-year Treasury Bonds generates, at current interest rates, about $25,000 annually. On the other hand, the same amount invested in an equity-dividend portfolio yielding 6.0%1 generates $60,000 annually, or more than twice the T-bond portfolio. In addition, dividend income grows over time while bond income remains the same.

Dividend growth keeps up with inflation

Unlike the income produced by fixed-income securities, equity dividends grow at a rate likely to exceed the inflation rate. Not only do investors start with more income per dollar invested, but dividend income will likely provide a longer-term inflation hedge.

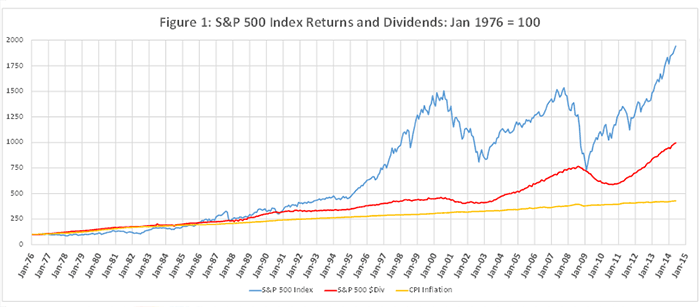

Figure 1 shows S&P 500 dividends for January 1976 through June 2014, while Table 1 shows annual statistics. This time period was particularly demanding for equities and dividends, with the high inflation of the late 70s and early 80s, the three-year 2000-02 market decline, the market crash of 2007-09 and the worst dividend decline since World War II occurring in first quarter of 2009. In spite of these challenges, dividends proved to be an excellent income source over this time period.

Each series is scaled to equal 100 in January 1976. S&P 500 Index does not include dividends. S&P 500 dollar dividends are trailing 12-month totals. CPI Inflation is the All Urban Consumers, All Items index. Sources: Thomson Reuters Lipper, St. Louis Federal Reserve FRED database.

Table 1: Jan 1976 – Jun 2014 Annual Statistics (%) |

|

Growth Rate |

Standard Deviation |

Max Drawdown |

S&P 500 Index |

8.03 (11.3)* |

15.0 |

-52.0 |

S&P 500 Dividends |

6.16 |

1.4 |

-23.5 |

CPI Inflation |

3.86 |

1.3 |

- |

* Total S&P 500 annual return including dividends.

Strikingly, dividends grew almost as fast as did the index (6.16% versus 8.03%), at less than 1/10 the volatility (1.4% versus 15.0%). Both the index and dividend growth easily surpassed this period’s 3.86% inflation. S&P 500 dividends provided a reasonably stable, growing source of income that more than offset the rising cost of living.

Dividends are largely unaffected by the many ups and downs of the market. Just because the equity market drops does not mean that dividends will experience a similar drop. This is an important relationship to remember, since in order to feel comfortable with dividends as an income source, it is necessary not to get emotionally caught up with the short-term ups and downs of the market. The fact that dividends had only a small response to market volatility provides an emotional buffer for the investor.

Some may find it surprising that dividends grew so consistently over time. The reason is that dividend decisions are based on the future prospects of the company, which in turn are dependent on the future prospects of the economy. Year-to-year dividend growth is more reflective of stable economic growth than emotionally charged market volatility.

Thus it should not be surprising to discover that most companies pursue a policy of growing dividends. Research shows that companies increase dividends 60% of the time, keep them unchanged 36% of the time and reduce them only 4% of the time. That is, increased and unchanged dividends outnumber decreased dividends by 27 to 1. While dividend reductions or, worse yet, dividend suspensions are a concern of many, the reality is that they are quite rare and their impact can be largely eliminated within a properly diversified portfolio.

Income growth guarantee: Setting up a safety fund

Since dividend payments are tied to the economy and the economy is expected to continue growing over time, there is good reason to believe that dividends will also grow over time, as was the case for the nearly-40-year time period presented in Figure 1. But over shorter periods, growth may not be sufficient to overcome inflation.

The worst S&P 500 dividend drawdown occurred in late 2008, when dividend income dropped by 23.5% from November 2008 through October 2010, based on trailing 12-month dividends. This was exacerbated by the slowest economic recovery since WWII. If you had the misfortune of investing at the beginning of this period, you would have taken a serious hit to your income in the ensuing two years. As mentioned, the first quarter of 2009 was the worst dividend quarter on record, so it is understandable that dividend income suffered during this period. However, dividends began to grow again in late 2010 and returned to their 2008 high in late 2012. But in the four-year journey to arrive where they were previously, investors experienced a significant income deficit.

What size safety fund would be needed in order to make up for this cumulative inflation-adjusted income deficit? Based on month-by-month calculations assuming a 6% dividend yield, the four-year cumulative deficit was roughly 3% of the initial amount invested or, in other words, six months of dividend income. For example, a $1 million initial investment means a $30,000 (i.e., 3%) risk-free safety fund would have been sufficient to cover four years’ cumulative inflation-adjusted income deficit. This is a surprisingly small amount to guarantee an inflation-protected income stream.

Note that the safety fund would only be needed in the extreme case of having invested in November 2008. Investing in any other month during this 40-year period would have resulted in a smaller withdrawal than $30,000 or no withdrawal at all. The latter would be the case in many months, as dividends grow faster than inflation, and consequently, the fund would become increasingly redundant.

This argument is based on an assumed initial dividend yield of 6.0%. If the initial yield is lower, then the fund could be a bit smaller, while if higher, it would a bit larger. The size of the safety fund is roughly equal to one-half of the dividend yield times the amount invested or six months of income.

With a small portion of the initial investment set aside in a risk-free fund, the risk of short-term inflation-adjusted income declining can be virtually eliminated.

Initial dividend yield as the safe withdrawal rate

There is an ongoing debate regarding the safe withdrawal rate. The proposed rates range from below 4% to over 5%. But even with a lower rate, there remains a chance of running out of money over longer time periods if the required withdrawals exceed the income generated by the portfolio, forcing the investor to fund a portion of future income needs by dipping into principal.

When this is the case, there always exists a number of return time series that will wipe out the initial principal. When dipping into principal, there is no way to avoid this problem.

In today’s low-interest-rate environment, the chance of running out of money increases as the allocation to fixed income increases. For this reason, fixed income is a poor choice for generating a growing income stream.

To avoid running out of money, it is important to create a portfolio with a high initial income yield accompanied by growth. A high-yield equity portfolio satisfies both these requirements. A high-dividend yield means that substantial income can be generated with a smaller initial investment, and since dividends are expected to grow faster than inflation, they will likely satisfy future income needs without dipping into principal. This substantially reduces the chance of running out of money.

Thus the initial dividend yield becomes the safe withdrawal rate. So if the initial yield is 6.0%, then the safe withdrawal rate is 6.0%. This is even more the case if the safety-fund strategy described in the previous section is employed. The 6.0% yield exceeds the rates currently put forward as safe. A high-yield equity portfolio thus dominates both the fixed-income and low-yield-equity alternatives that are the focus of most current analysis.

It is therefore desirable to build an equity portfolio with a high initial yield. Before I discuss how to create such a portfolio, let me address the common misconception that there is a tradeoff between higher yield and total portfolio return.

High dividend growth and yield mean high total returns

Research shows that the higher the dividend growth rate or the higher the dividend yield, the higher is the subsequent total portfolio return. At the overall market level, studies (see here and here) reveal that higher cash payout and dividend yields are indicative of higher future market returns. More specifically, research reveals that dividend yield is a good predictor of future earnings growth, so a period of rising dividend yield bodes well for future market returns.

This belies the common belief that companies increase dividends when investment and future growth opportunities are poor. On the contrary, company management is actually signaling higher future cash flows by increasing dividends, which in turn foretells higher stock returns.

At the individual stock level, dividend payout and yield are predictive of future earnings growth and future returns (see here). Among other things, this body of research has found that dividend changes contain information about future earnings that cannot be found in other market data, company profitability and future positive earnings surprises. Other research has found that companies experiencing financial distress rely more heavily on dividends for communicating with investors.

The overall conclusion is that rising dividends signal improved company performance and, in turn, higher individual stock returns. The market myth that higher-yielding stocks produce lower total portfolio returns is consistently rejected by evidence.

Higher returns, lower volatility

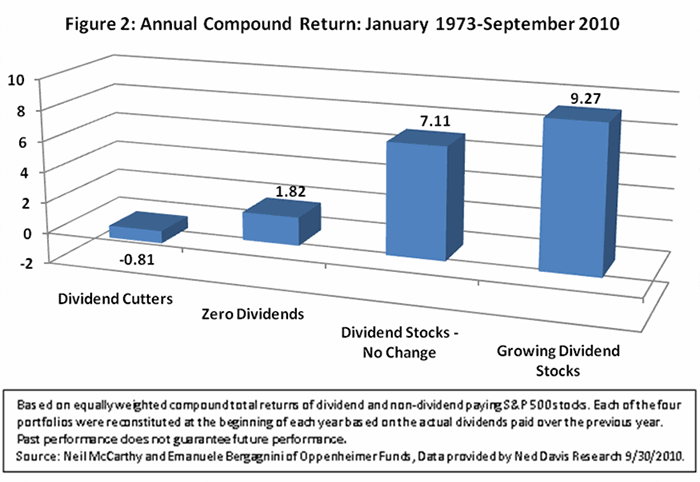

In order to appreciate the power of dividends, consider the average annual compound returns for S&P 500 stocks from 1973 to 2010, as reported in Figure 2 below. Over this period, S&P 500 stocks that paid growing dividends outperformed dividend-cutting S&P 500 stocks by an astonishing 10% annually. Growing dividends are predictive of strong future stock returns, while zero or reduced dividends are a predictor of poor stock returns.

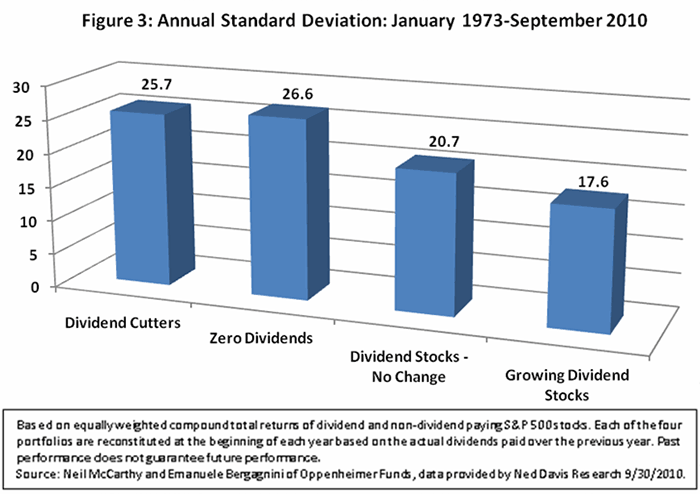

Even more surprising, volatility declines as dividends increase. Figure 3 below reports the annual standard deviation for the four portfolios reported in Figure 2. In general, volatility decreases as dividends – and accompanying stock returns – increase. In particular, the dividend-growing portfolio experiences roughly one-third less volatility than does the dividend-cutting portfolio.

And principal grows too!

Not only do dividends grow over time, but so does the principal, even if all dividends are paid out and not reinvested. As we saw in the last section, the higher the yield, the higher the return. For example, with a dividend yield of 6.0%, we would expect principal growth of greater than 3%, based on an average annual stock market return of 10%.2 This means that without dividend reinvestment, both dividends and principal are expected to grow at or above the long-term inflation rate of 3% annually.

You can “have your cake and eat it too” with both growing income and principal. A high-dividend yield portfolio dominates a traditional low-risk bond portfolio in terms of dividend yield and growth as well as growing wealth.

But what about short-term volatility?

The one downside to a high-dividend equity portfolio is short-term price volatility. But stock price volatility has little impact on the dividend stream paid, since, as discussed earlier, firms follow a stable or growing dollar dividend policy and very infrequently reduce dividends. In addition, short-term price volatility disappears, as downward movements are more than offset by upward movements over time. Thus, principal grows over the long run.

But market volatility is a highly emotional issue and is a challenge for many investors to get beyond. The rational argument is that short-term volatility is diversified away over long time periods. The challenge is to get clients to focus on their long-term investment horizons rather than falling prey to short-term volatility.

Investing in high-yield equity to grow income provides further separation between market volatility and income. As I argued earlier, the dividend income stream generated by an equity portfolio is little impacted by market movements, since dividend decisions are based on the future prospects of the company, which in turn are driven by overall economic activity. There is a better chance of getting clients to look past emotional short-term volatility when investing in high-yield equity for income generation than when investing in stocks for capital growth.

Go global, go conviction, go high yield

There are a number of ways to build a high-yield equity portfolio. Including both U.S. and international stocks in such a portfolio provides both a diversification and a yield benefit. These two asset classes have less than perfect correlation, while international stocks tend to pay a higher dividend. It is also possible to change the weighting between these two based on return expectations in the markets.

In selecting stocks, it is possible to choose among the high-conviction stocks held by the best U.S. and international active equity-mutual-fund managers.3 The spread between the lowest- and highest-conviction stocks is from 4% to 6%, so focusing on the highest-conviction stocks provides an attractive pool from which to select stocks for inclusion in a portfolio.4 From this pool, a diversified portfolio of high-yield global stocks can be built.

Both yield and return can be further enhanced by weighting the portfolio by dividend yield and expected return. The expected-return weights are based on the expected returns in both the U.S. and internationally, with larger weights for the higher expected return market.5

Test results

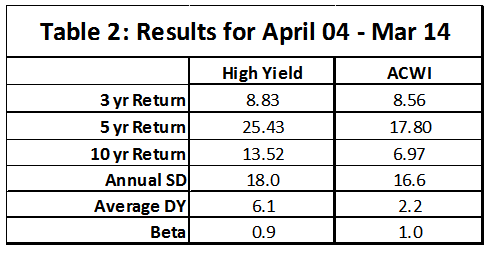

Table 2 shows the results for a test of the high-yield approach just described from April 2004 to March 2014. On average, the portfolio holds 41 mid- to large-capitalization stocks and is invested 63% in the U.S. All decisions are based on mechanical decision rules, using only data available at the beginning of each of the 120 months during the test period.

The high-yield portfolio dramatically outperforms the MSCI All Country World Index (ACWI) both in terms of 10-year return (13.52% vs 6.97%) and yield (6.1% vs 2.2%). These results are consistent with the global, high-conviction and high-yield research described earlier. What is more, these strong results are accompanied by a below-average beta of 0.9. The portfolio delivers superior returns and yield accompanied by average to below-average risk.

The expectation for such a portfolio, beyond an above-average yield, is that both dividend-generated income and principal, without dividend reinvestment, grow over time. The results reported in Table 3 confirm this to be the case. Dividend income grows by an impressive 8.1% annually, while principal grows 6.0% per year. Note that this period includes the market crash of 2007-09 and the worst dividend quarter in recent history, the first quarter of 2009.

The result is that the strong 6.1% yield is accompanied by an even stronger growth in income and an equally strong growth in principal. This portfolio generates substantial income per dollar invested, produces an income stream that grows at a rate two to three times the inflation rate and yields principal growth resulting in real wealth gains. Indeed, investing in a high-yield equity portfolio does allow you to have your cake and eat it too!

The advantage of high-dividend equity

High-dividend equity addresses three major concerns facing investors when building an income-generating portfolio: getting sufficient yield, keeping up with inflation and outliving available funds. The dividend decisions made by companies are based on the future prospects of the company. The growth in a portfolio’s dividend income is closely tied to the growth in the economy, rather than to the short-term movements in the stock market. Companies rarely cut dividends, so these adverse effects largely disappear in a properly diversified portfolio.

The combination of high-yield and growing dividends essentially eliminates the risk of outliving available funds. This is because it reduces the need to dip into principal in order to meet income needs. Liquidating principal for this purpose has associated with it a chance of running out of money. Finally, a small risk-free safety fund can be set up to insure against the unlikely event of short-term dividend declines.

A high-yield equity portfolio can be created in a number of ways. In this paper, I presented an approach that includes both U.S. and International stocks, which takes advantage of the lower correlations between these two groups of stocks and the fact that international companies frequently pay higher dividends than their U.S. counterparts. The yield is further enhanced by initially considering a larger pool of high-conviction stocks, as signaled by active equity-mutual-fund managers, and dividend weighting the portfolio. Our research and experience in managing such portfolios suggest that a dividend yield exceeding 6% can be maintained over time.

To appreciate the advantage of high-dividend equity over other alternatives for funding income needs, consider the following hypothetical example. Assume you have $1 million to invest in one of three alternatives: a 10 year T-bond (2.5% coupon), 10 years in Barclay’s High Yield Index (7% coupon) and 10 years in high-dividend equity (6.0% yield). Assuming a 7% coupon rate is available throughout the 10-year time period and that final maturity matches the 10-year time horizon, here are the estimated total income and principal appreciation for each of these alternatives.

|

10 year T-bond |

High Yield Bond |

High Dividend Equity |

Total Income |

$250,000 |

$700,000 |

$830,000 |

Principal Appreciation |

$0 |

$0 |

$600,000 |

Total Return on $1 mil |

$250,000 |

$700,000 |

$1,430,000 |

There is no guarantee that the 7% coupon rate will be available, as the bond(s) would have to be rolled over several times during the 10-year investment period. I also assumed initial dividend yield of 6.0%, dollar dividend income growth rate of 6%, principal growth of 6% and 1% fees deducted from the principal. The 6% growth rates are based on research conducted by Athena and others.

High-dividend equity dominates the other two alternatives, both in terms of total income and principal appreciation. In fact, it generates six times the total return as compared to the T-bond and more than twice that of the high-yield bond. This provides further evidence of the advantage of high-dividend equity for generating income.

It is important to get past the emotions of short-term market volatility to reap the benefits of high-dividend equity. The fact that dividend income growth is closely tied to the growth in the economy, and less to emotionally charged market volatility, provides a buffer for the investor. At almost every level, high-dividend equity represents an attractive income solution.

C. Thomas Howard, PhD is professor emeritus at Daniels College of Business, University of Denver, CEO of AthenaInvest Advisors and portfolio manager of AdvisorShares Athena High Dividend ETF (DIVI).

Read more articles by C. Thomas Howard, PhD