Stocks should be the asset class of choice for the long run, according to Wharton Professor Jeremy Siegel – and he has provided the data to prove it. But that paradigm has been challenged by Boston University Professor Zvi Bodie and others, who have shown that stocks become riskier the longer one owns them. Either view has profound implications for whether equity allocations should increase or decrease over time. Using Monte Carlo simulations, we provide guidance for the advisory profession.

In two recent articles, we have introduced the basics of Monte Carlo simulation and expanded on some of the practical applications of Monte Carlo analysis. In this article, we expand on a concept touched on briefly in both: time diversification. Time diversification has implications for how advisors build portfolios for clients and how we depict the probability of outcomes over longer investing periods.

The idea that stocks are good long-term investments is ubiquitous in financial planning, but it drives a lot of economists up the wall. Economists think that all things, including stocks and bonds, are priced fairly according to the risk preferences of buyers and sellers. Stocks are risky and therefore should have a higher average return. But risk means that sometimes stocks will have a lower return than bonds, even in the long term. Otherwise, they wouldn’t be risky. If we always did better investing in stocks over a 30-year time horizon, then only idiots wouldn’t buy them for retirement. And economists don’t like to believe that investment prices are set by idiots.

Many investors do appear to be idiots, unfortunately — or at least they were in the past. If you look at the historical data for developed countries, stocks have been less risky for long-run investors. And that’s not just some of the time, but pretty much all of the time.

We’re left with the very unsatisfying conclusion that stocks are the best asset class choice for long-run goals, even for risk-averse investors. Although unsatisfying for many economists and others who believe that it should be risk tolerance, not time horizon, that determines portfolio recommendations, it is best to at least understand how time diversification impacts optimal portfolios if future investments continue to behave as they have in the past.

Our Monte Carlo simulation results show how incorporating time diversification can have a large impact on portfolio recommendations compared to Monte Carlo simulations that ignore the effect. First, however, let’s look at the challenge researchers face when modeling time diversification. We’ll then turn to how Monte Carlo simulations can overcome those hurdles and how we constructed our model.

The role of Monte Carlo analysis

A simple Monte Carlo analysis assumes that returns are independent of one another. Simulated returns don’t include recessionary periods when stock prices fall too much and expansions when they rise too much. Some of the simulations will have the appearance of these scenarios (e.g., multiple consecutive negative returns). But there is no underlying force tethering the returns from getting too far out of line. Rising and falling stock prices in recessions and expansions create short-run volatility, but the cyclical nature of rising and falling valuation means that stocks aren’t too risky for long-run investors.

The ebb and flow of stock valuations results from mean reversion. Stock returns (or, more accurately, the excess return over bonds, known as the equity risk premium) go up and down with investor sentiment. This predictable short-term volatility gets smoothed out over the long term. So an investor who doesn’t care about short-run volatility gets rewarded with high returns and lower long-run risk.

The mean reversion and market sentiment story has been validated in finance literature. This is good news for investment advisors who can earn their fees by keeping clients from selling out of the market when valuations are most attractive (remember March 2009?). But it is bad news for Monte Carlo simulations if they are built on the assumption that mean reversion doesn’t exist. Estimations won’t give enough credence to what appears to be a very real phenomenon of time diversification.

Time diversification is the idea that stocks become less risky over the long run yet still earn a high risk premium. This is the part that most bothers economists who believe in efficient markets. If it were true, corporations could just issue long-term bonds, invest in stock mutual funds and earn a riskless profit. Bodie (1995) emphasized that time diversification violates the Black-Scholes option-pricing model and should show up in the prices of long-term stock options. But it doesn’t, leading him to conclude that stocks are indeed riskier over the long run. Despite Bodie’s research, there is a growing body of evidence that time diversification exists in the historical market-return data.

Siegel (2008) noted that stocks have been less risky over long holding periods based on historical equity returns in the U.S. going back to 1801. There is a growing body of literature dedicated to this topic, including our own research. The advantage of stocks as long-run investments may just be a historical anomaly, but it’s a historical anomaly that holds up in just about every country we looked at over a very long period of time.

Testing for time diversification

A variety of methods can be used to determine whether time diversification is a reliable phenomenon. Previously, we showed how the historical distribution of returns for the U.S. stock market (based on an illustration by Dick Purcell) has been narrower than would be the case if returns were in fact random over time. This suggests stocks exhibit some level of autocorrelation, or serial correlation, meaning that returns in one period are correlated to those in prior periods.

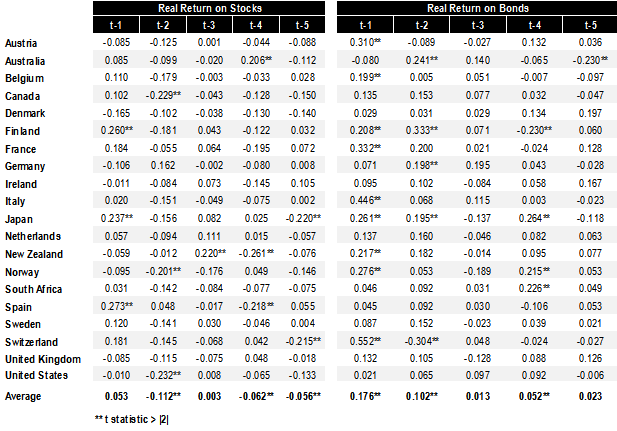

Rather than just looking at U.S. market returns, which is the most common means for testing for time diversification, we rely on the historical returns from the Dimson, Marsh and Staunton (DMS) dataset of historical returns for 20 of the largest global markets going back to 1900. We focus on the real return for stocks and bonds in each respective country (based on that country’s local currency and inflation rate).

Our goal is to see whether historical returns in the past predicted returns today. In other words, does last year’s stock return predict this year’s return? Or does the return five years ago do a better job of predicting returns today? To test for time diversification, we ran an autoregressive regression (with five prior years of stock returns, or an AR(5) model) against the real return for stocks (S) in a given year (t) versus the return in previous years (t-1, t-2, etc.) for each of the 20 countries introduced in Equation 1 in the Appendix. In the following table, t-1 is last year’s stock returns, t-2 is stock returns two years ago, etc.

AR(5) coefficients by country for stocks and bonds

Each number in this table is a correlation between current and prior returns. A negative value indicates that positive returns have led to future negative returns, and vice versa (which is unfortunate for those who think that 2014 is a great year to get back in the market). Greater values (either positive or negative) and statistical significance (stars) indicate stronger and more consistent correlations.

The results vary significantly by country. However, most lack a high degree of statistical significance. However, there are some notable differences in the average results when comparing stocks and bonds. The average coefficients for the second, fourth and fifth lags for stocks are negative. This means that when all 20 countries are combined, returns in the past appear to predict returns in the future.

To be clear, this is not an invitation for market timing. But it does suggest that when simulating long-term planning, negative returns have been followed by positive returns.

This negative relation between returns today and returns in the near future suggests the existence of time diversification. Also, the lags for bonds are positive and have larger coefficients than those for stocks. This suggests while stocks become less risky over time, bonds become more risky.

Time diversification and Monte Carlo simulation

If stocks become less risky over time and bonds become riskier, this has important implications for modeling. However, the overwhelming majority of Monte Carlo tools assume that returns are not related from one period to the next (or i.i.d., which stands for “independent and identically distributed”). This is both a simplifying assumption and consistent with how the markets should behave.

The strong international evidence of time diversification has important implications for financial modeling — in particular for Monte Carlo simulations, which are commonly used to estimate the range of potential portfolio outcomes for different types of clients. The majority of estimates used in Monte Carlo simulations do not incorporate an autoregressive model (i.e., they assume that stock returns are i.i.d.) and implicitly assume time diversification doesn’t exist. This will lead to different optimal portfolio allocations for equity investors, especially those with longer investment horizons.

In order to better approximate the historical risk of equities over time, we use the results for the U.S. in the AR(5) model in the previous table. We select U.S. equity returns since they are relatively similar to the 20-country average, although in reality any country could be selected.

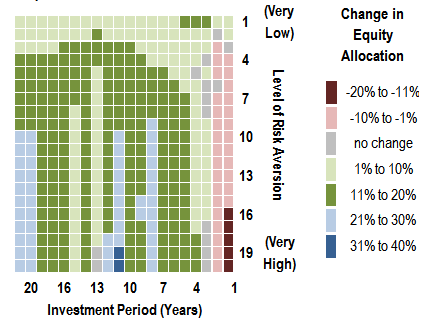

We estimate the real return of stocks (rrs) using Equation 2 and the real return on bonds (rrb) using Equation 3, both of which are included in the Appendix. We conducted a 10,000-run Monte Carlo simulations to determine the optimal equity allocation for investment periods from one to 20 years (in one-year increments) and risk-aversion coefficients from 1.001 to 20 (again, in increments of 1) for the 21 different stock and bond combinations in which the allocations, from 0% equities to 100% equities, change in 5% increments. For each scenario, we compared the optimal allocation for the model that incorporates autocorrelation to the one that doesn’t to determine the relative impact of autocorrelation on Monte Carlo simulations. The results are included in Figure 1.

Figure 1: Change in optimal equity allocation when incorporating autocorrelation by risk aversion level and investment period

There are notable differences in optimal portfolios for different types of investors when autocorrelation is factored into the analysis. First, more conservative investors (i.e., those with a higher level of risk aversion) should invest more conservatively. This can likely be attributed to the positive autocorrelation associated with real bond returns, which increases the potential risk over shorter investment periods. The relative benefit of equities increases the longer the investment horizon, especially for more conservative investors. For example, the optimal allocation to equities increases by 25 percentage points (from 40% stocks to 65% stocks) for an investor with a 20-year investment time horizon and a risk-aversion level of 10.

Implications

Although an AR(5) model is not essential when running a Monte Carlo simulation, it captures the historical level of time diversification associated with U.S. equities. Not using such a model makes the implicit assumption that time diversification does not exist. While this is inconsistent with historical international stock returns, there is no guarantee that time diversification will persist in the future. An ideal recommendation would be to temper historical findings with the reality of future uncertainty, although the empirical evidence supports an increasing allocation to equities with longer time horizons.

Our results lend greater credence to the time-segmentation strategies preferred by many advisors for designing retirement-income portfolios. In such a strategy, short-term spending is covered by maturing bonds and with long-term spending is funded by a growth-focused equity portfolio, with the idea that this will prevent the need to sell stocks after market downturns.

David M. Blanchett, CFA, CFP® is the head of retirement research for Morningstar Investment Management in Chicago, IL.

Michael Finke Ph.D., CFP® is a professor and director or retirement planning and living in the personal financial planning department at Texas Tech University in Lubbock, Texas.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at the American College in Bryn Mawr, PA. He is also the director of retirement research for inStream Solutions and McLean Asset Management. He actively blogs about retirement research. See his Google+ profile for more information.

References

Bodie, Zvi. 1995. On the Risk of Stocks in the Long Run, Financial Analysts Journal, 51, 18-22.

Siegel, Jeremy J. 2008. Stocks for the Long Run, 4th ed. McGraw Hill, New York, NY.

Appendix

Equation 1: for this equation we attempt to determine the relation between the return on stocks in the current year (St) and the return on stocks in previous years (t - 1, t - 2, etc.).

Equation 2 and 3:

For both equations the coefficients are based on the average coefficients for regressions across the20 countries included in the DMS dataset. For equation 2, is assumed to have a mean of 0.0% and standard deviation of 23.26%. For equation 3, is assumed to have a mean of 0.0% and standard deviation of 12.90%. We chose these standard deviations they produce a series of returns which will match the standard deviation (i.e., riskiness) of the asset classes found in the historical data that cannot be explained with our model.

Read more articles by David Blanchett, Michael Finke and Wade Pfau