On Friday, Fed Chairwoman Janet Yellen said that the nine-year wait for an interest-rate increase would likely end

this year. Three days earlier, though, Jeffrey Gundlach said that a rate increase this year is unlikely, given the

mix of bad news and uncertainty in the world markets. Which view prevails will be the focus of bond market

participants in the months ahead.

On Friday, Fed Chairwoman Janet Yellen said that the nine-year wait for an interest-rate increase would likely end

this year. Three days earlier, though, Jeffrey Gundlach said that a rate increase this year is unlikely, given the

mix of bad news and uncertainty in the world markets. Which view prevails will be the focus of bond market

participants in the months ahead.

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital, a provider of

fixed-income mutual funds and ETFs. He spoke to investors via a conference call on July 7. Copies of the slides from

his presentation can be found here.

“With the Shanghai price movement and what is going on in Greece and Puerto Rico and other places, it is

increasingly unlikely that the Fed is going to be raising interest rates in September,” Gundlach said. There

is consensus; he said the futures market is pricing in less than a 50% chance of a Fed hike at its next meeting, in

September.

Yellen, however, said that “it will be appropriate at some point later this year to take the first step to

raise the federal funds rate and thus begin normalizing monetary policy." But, perhaps mindful of the factors

Gundlach cited, she added, "I want to emphasize that the course of the economy and inflation remains highly

uncertain, and unanticipated developments could delay or accelerate this first step."

Gundlach also offered some asset-class forecasts and predicted the Greece would leave the euro. But, first, let’s

look at what he said are the key issues that will influence the Fed’s rate-increase decision.

The odds of a Fed rate hike

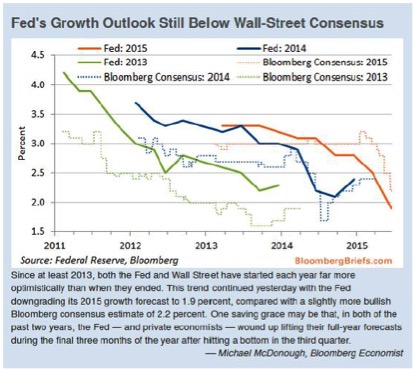

For the last four years, the Fed has been consistently downgrading its economic forecasts, as can be seen in the

chart below:

The orange line shows the Fed’s forecast from 2013 to 2015. It started less optimistically than in the prior

two years, and has been declining steadily. It is now lower than at any time during 2013 or 2014, Gundlach said.

“It is remarkable that people are talking about the Fed raising interest rates when the Fed’s own

forecast for 2015 growth is lower than it has ever been and lower than the actuals for 2013 and 2014,” he

said.

An unbiased observer would surely advise the Fed to ease – and not tighten – credit conditions based on

this data, Gundlach said.

Gundlach repeated what he has said in the past, “The Fed does not want to be at zero. It’s looking for

reasons to do it. But this exhibit certainly does not give them any such reason.”

The precipitous decline – which Gundlach called a “crash” – in China’s equity markets

(the Shanghai index) will weigh against the likelihood of a rate increase. He said the Shanghai market resembled the

NASDAQ in the fourth quarter of 1999, when the dot-com crash unfolded.

“When you have a major stock market, the strongest stock market in the world reverse from a frenzied

bubble-type condition into what can only be called something of a crash,” he said, “the only thing you

can say about it is that it is not a good indicator for other things.”

The price decline in copper, which had just hit its low for 2015, signals economic weakening, further reducing the

odds of a rate increase, Gundlach said.

“I hardly think the Fed would be wise to raise interest rates with all of the trouble in the sovereign markets

coupled with the Chinese stock market coupled with what’s going on with commodity prices,” he

said. “The Fed is having a hard time or will have a hard time finding justification for getting off of zero

because data hasn’t been very supportive.”

Gundlach said the Fed should try to avoid the mistakes made by the central banks in Australia, South Korea, Denmark,

Norway, Sweden and New Zealand, all of which had to ease monetary policy after prematurely increasing rates.

He offered two signs that would support a rate hike: increased inflation expectations and higher expectations for

hourly earnings. He cautioned, however, that expectations do not necessarily translate to reality. And he added

that, while inflation expectations were increasing for the CPI, they were not for the PCE, which is the Fed’s

preferred metric for gauging inflation.

Asset class valuations

Gundlach offered his assessment of relative valuations for a number of asset classes within the bond market.

Investment-grade bonds, he said, had cheapened relative to high-yield bonds as of the end of June. He said he

increased his allocation to investment-grade at that point, which turned out to be a good decisions.

High-yield bonds are modestly overvalued, according to Gundlach. He said that they will not provide a “cushion”

in the event of a Fed rate hike. He noted that since April, Treasury rates rose from 2.1% to 2.5%, but high-yield

bonds rose by even more – from 4.25% to 4.75%. Gundlach said he is fearful of high-yield bonds several years

from now, when the number of bonds maturing spikes. (For an opposing view of this issue, read this commentary

from GMO.)

For most of the last two years, Gundlach has been bearish on TIPS, saying that “TIPS are for losers.”

But he said their valuations are starting to look more attractive relative to nominal bonds because he expects the

CPI to increase. With the stated yield on most TIPS maturities near zero, the return consists mostly of inflation as

reported in the CPI.

Yields on German bunds, the benchmark European sovereign debt, are headed to 1.25%, he said. Those yields were below

zero earlier this year.

Gundlach reiterated his forecast that interest rates would end 2015 roughly where they began the year; the 10-year

bond yield was up a mere eight basis points so far. But, he added that there was the possibility of a “flight

to quality melt up” that would lead to lower rates. As a result, he said he increased the duration on some of

his funds.

Gundlach doesn’t hold any convertible bonds in any of bond funds, and he said they were extremely overvalued,

reflecting overvaluation in the U.S. equity markets.

He does not own any Puerto Rican bonds either. But if they get cheaper, he said he might want to “play around”

with them in some of his funds.

Whither Greece?

Greece is going to leave the euro, but Gundlach did not say when this will happen.

He said Greece’s and the Europeans’ ability to “keep their fingers in the dike as the cracks

expand” was truly remarkable.

Nonetheless, he said, “It’s a slow-motion deal and I don’t think it’s going to work.”

Gundlach said there was a group of “basket case” countries, including Greece, keeping the euro lower. If

they leave, he said the value of the euro would be pushed higher. “With Greece leaving in a certain sense it’s

theoretically good for the euro,” he said.

But there is a “Pandora’s box” of risk surrounding a Greek exit. Ultimately, Gundlach said it

would mean the end of the euro. Despite being only 2% of Europe’s economy, Greece’s exit would be like

when South Carolina left the Union in the 1860s. It was not long before all 13 Confederate states had seceded.

“When one leaves others join them, or at least potentially join them,” he said, adding that Greece is

but one of many weak European economies. “There is never one cockroach.”

“The euro is like Rasputin; it doesn’t want to die but eventually there will be enough bullet holes,

stab wounds, burns, decapitation until ultimately the thing doesn’t play out,” he said. “But for

now they certainly are fighting it tooth and nail.”

Read more articles by Robert Huebscher

On Friday, Fed Chairwoman Janet Yellen said that the nine-year wait for an interest-rate increase would likely end

this year. Three days earlier, though, Jeffrey Gundlach said that a rate increase this year is unlikely, given the

mix of bad news and uncertainty in the world markets. Which view prevails will be the focus of bond market

participants in the months ahead.

On Friday, Fed Chairwoman Janet Yellen said that the nine-year wait for an interest-rate increase would likely end

this year. Three days earlier, though, Jeffrey Gundlach said that a rate increase this year is unlikely, given the

mix of bad news and uncertainty in the world markets. Which view prevails will be the focus of bond market

participants in the months ahead.