Disciples of factor-based investing need to respond to a new challenge. According to Mark Kritzman, investors will be better served by a strategy based solely on allocating to asset classes.

Kritzman is the founding partner and chief executive officer of Boston-based Windham Capital Management. He spoke on November 9 at Windham’s annual research summit, held in Boston. His presentation was based on an unpublished paper, “Facts about Factors,” which he co-authored with Paula Cocoma, Megan Czasonis and David Turkington of State Street Global Advisors.

By “factor-based investing,” Kritzman means more than just attributes like value, size and momentum; he is also including allocations to fundamental factors such as inflation and economic growth, as well as what he calls “principal components.” Principal components are based on a statistical analysis that breaks down the universe of stocks (or other assets) into subgroups that are uncorrelated to one another.

Instead of a factor-based approach, Kritzman advocated adjusting one’s allocations to asset classes based on overall market risk – a metric he calls turbulence. He believes that markets are macro-inefficient; asset classes are over- and under-valued at points in time. His firm, Windham, manages assets through separately-managed accounts and sub-advised mutual funds based on those principles.

I’ll discuss what Kritzman said about his investment approach, but first let’s look at the four reasons why factor-based investing is inferior to asset-class-based investing.

The four flaws in factor-based investing

Kritzman gave four reasons why he dislikes investing in factors.

Proponents of factor-based investing, Kritzman said, often make the claim that factors are less correlated than assets and, therefore, offer greater diversification benefits. That claim, he said, is false.

“The idea that factors provide more opportunity for diversification than assets is nonsense,” Kritzman said.

Many of the claims of diversification benefits, according to Kritzman, rely on misleading data. He said that is because researchers use short positions to give factors the appearance of greater diversification.

Since investing in factors ultimately requires selections of individual assets, he said it is “mathematically impossible” to create a more diversified portfolio with factors than with assets.

The second myth about factors is that they reduce the “noise” when compared to assets. This claim relates to the fact that, when securities are consolidated into factors the means of the returns of those groupings are less noisy than the means of the returns of securities. But this would be just as true if securities were consolidated into asset classes. Kritzman also pointed out that consolidation does not reduce noise in covariances.

The third claim that Kritzman countered was that factors are easier to predict than asset classes. Some people, he said, are more skilled at predicting factors than asset classes – and vice versa. He said this argument is investor specific and cannot be tested generically. But those who choose to predict factors face the additional challenge of predicting how these factor values map onto factor mimicking asset groupings.

“At the end of the day, you must invest in assets,” Kritzman said.

The mapping of factors to assets introduces a potential error that does not exist in an investing strategy based solely on assets, and so it puts factors at a disadvantage.

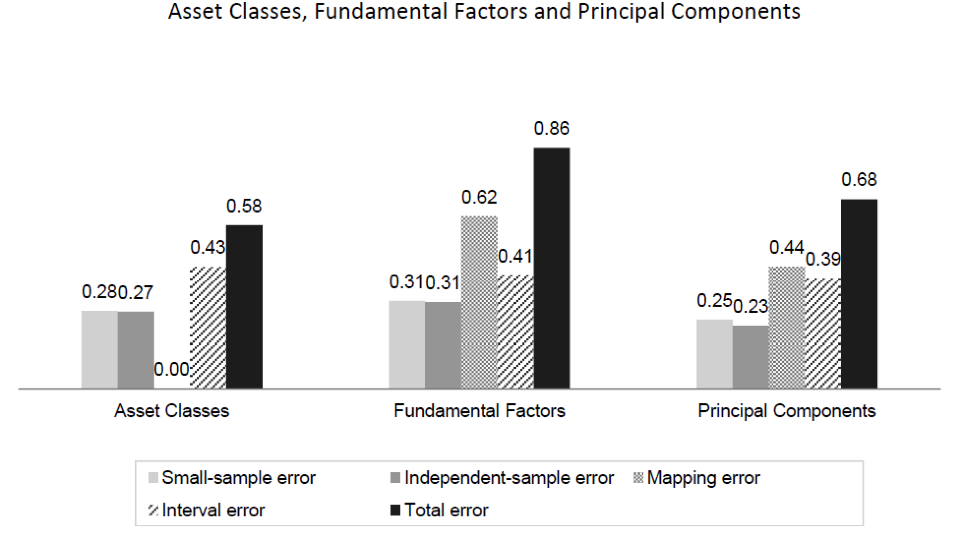

Kritzman’s final critique of factor investing is that it increases estimation error. That is, the ability to use historical data to project future returns. Both factors and assets are subject to three common sources of error: small-sample error, independent-sample error and interval error. But factor investing, unlike investing directly in assets, is subject to mapping error.