The Fed may be intent on raising interest rates, but a wide range of market indicators should give it pause to reconsider, according to Jeffrey Gundlach. Indeed, he said the biggest challenge to a rate hike is the weak inflation readings in the U.S.

Gundlach is the founder and chief investment officer of Los Angeles-based DoubleLine Capital. He spoke to investors via a conference call on December 8. Slides from that presentation are available here. The focus of his talk was DoubleLine’s flagship total-return mutual fund, DBLTX.

“The Fed’s biggest problem in justifying the rate increase is the inflation numbers make this anything but the moment to act on raising interest rates,” he said.

And the Fed faces other problems.

In an eerie premonition, Gundlach said that, “It will be interesting to see if the meeting can come and go without the market deteriorating further.” He noted that, “We are looking at some real carnage in the junk bond market.”

Three days later, the high-yield market was rocked by the gating of Third Avenue’s high-yield fund, followed by a similar move by Stone Lion Capital Partners, a distressed-debt hedge fund.

I’ll look the problems in the junk bond market. But first, let’s look at the range of indicators that Gundlach said argue against a rate increase, as well as a few that point in the other direction.

The landscape facing the Fed

On the day Gundlach spoke, there was an 80% likelihood of a rate increase, based on data from the capital markets. Moreover, he said that 100% of economists are predicting an increase. If there is an increase, Gundlach said it would be 25 basis points – no more, no less.

Looking at the historical data, Gundlach said that real GDP growth and unemployment are consistent with levels at past increases.

But nominal GDP is not consistent with prior rate increases. Gundlach said nominal GDP growth is lower than it was in September 2102, when the Fed considered the economy so weak that it began its third round of quantitative easing (QE3).

Gundlach called the ISM survey data a “disaster.” It is at its lowest level since the Great Recession. That weakness is confirmed by industrial production, which Gundlach said is flat on a year-over-year basis. The ISM is highly correlated to nominal GDP, he said, and the implication is that a rate hike would put “downward pressure on nominal GDP.”

European policy contrasts bluntly with a rate increase. Inflation is lower in the U.S. than in Europe, he said, if one compares the data on an equivalent basis. U.S. GDP growth is a mere 60 basis points greater than in Europe, which Gundlach said exposed an inconsistency between Europe’s aggressive quantitative easing and a Fed rate hike. “There is just something seriously wrong with this picture,” he said.

Lack of inflation worries Gundlach the most. He called it a “bugaboo that is affecting the markets right now, and may cause a problem for the Fed.”

The Fed uses the PCE as its inflation indicator. Gundlach said that headline PCE is growing at only 20 basis points annually, and core PCE is 42 basis points lower than when the Fed started QE3.

“The Fed is working on a philosophical program and wants to boost its credibility for having promised nearly a rate rise in 2015,” he said. “It looks like they are going to find out what might happen if they raise rates. It will be an interesting experiment.”

Other central banks have experimented similarly, most notably Sweden, which had to cut rates after a premature rate hike. Gundlach said the median time from a rate hike to a reversal has been 16 months among those central banks that had to reverse course.

What the market is saying

On a broader basis, Gundlach said that markets are encumbered by a lack of global growth.

“Global growth is insufficient to keep all countries at a positive growth rate,” he said. “There are many countries now at a negative growth rate and you end up with currency devaluations.”

Raising rates, he noted, strengthens one’s currency, and this partly explains why some countries had to undo rate increases.

The Fed regularly releases a dot diagram, which shows the sentiment of individual members toward a rate increase. If the Fed followed the consensus represented by the dots, Gundlach said, rates would increase to 1.38% in the next year. That is inconsistent with Fed statements about a “gradual” increase, Gundlach said. He predicted that, if the Fed were to follow the dots, the yield curve might invert.

That is because the long bond has already priced in a rate increase. It is “respecting the carnage,” Gundlach said, in commodities, emerging markets, junk bonds and bank loans.

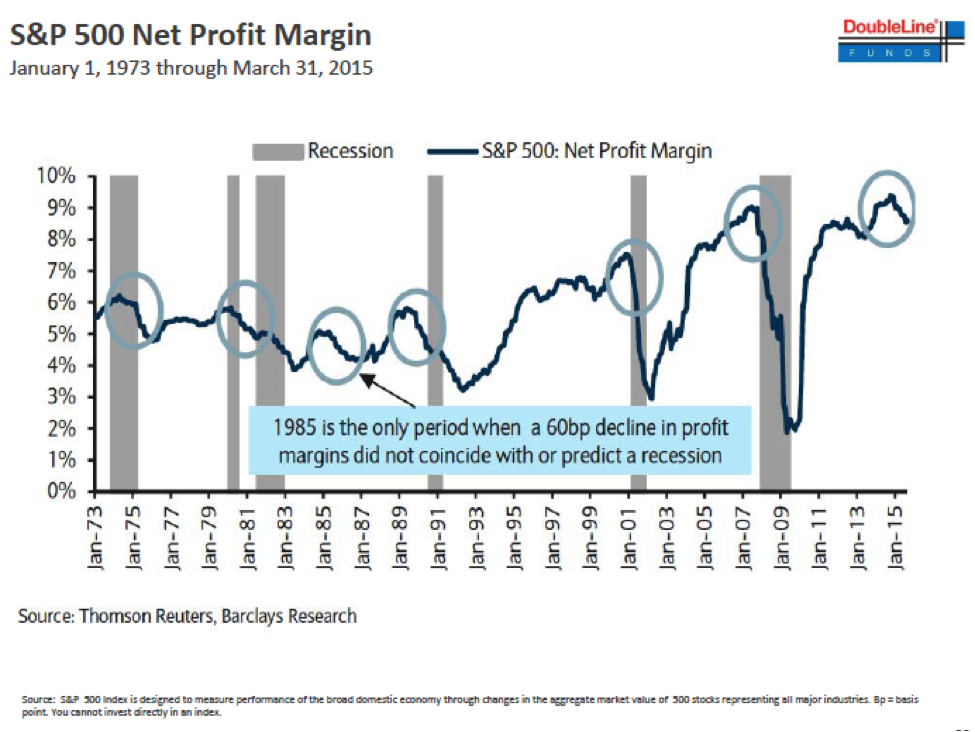

“If you want to stay up at night worrying about something, you can stare at this chart,” Gundlach said.

The chart shows that the drop in net profit margins in the S&P is of the magnitude that has correlated with recessions, according to Gundlach.

High-yield bonds and more

The junk-bond ETF, JNK, closed at 34.4 on the day he spoke. It finished the week at 33.7, its lowest value in over six years.

“High-yield spreads have never been this wide prior to a first rate hike,” Gundlach said.

In 1994 they were 350 basis points over Treasury bonds and, in 1999 and 2004 the spread was approximately 400 basis points, he said. It is now over 600 basis points.

“The junk bond market has already really tightened up conditions on companies borrowing money,” he said. “It would be unthinkable using this indicator for the Fed to raise interest rates. But again, they want to raise rates next week.”

Leveraged loan prices reinforce the view that the economy is weak. Those loans have floating rates, and Gundlach said their price is down 10% since June of 2014. “This is really a little bit disconcerting that we are talking about raising interest rates with the credit markets and corporate credit absolutely tanking,” he said. “They are falling apart.”

Repeating something he has said in previous webcasts, Gundlach predicted that time is running out for energy companies that may have benefited by hedging the price of oil two or three years ago. Those hedges are about to expire, he said, and will lead to further weakness in the junk-bond sector.

Gundlach cited weakness across the global markets. The Shanghai composite, he said, “looks really, really bad” and is at its lowest level in eight years. Business activity in China is negative, he noted, and that contributes to the weakness in commodities.

Brazil’s GDP is “really ugly,” he said, and it is effectively in a depression. Its GDP is down 4.45% over the last three quarters.

Weakness extends in the emerging markets. Gundlach said that the price of the EEM ETF is down 28.4% since September 2014. So we’ve got junk bonds down 18%, bank loans down 10%, and emerging market equities down 29%.

He called commodities the “widow maker” because it is suffering from “monstrous” declines. The CRB index is down 43% since June 2014, according to Gundlach. Copper, the industrial metal that’s often used as a barometer of the global economy, is down 37% since July 2014. Even lumber is down, he said – 25% since September 2014.

The problem in the energy markets, according to Gundlach, is simple: Oil production is too high – higher than it was when prices started to decline in 2014. U.S. crude inventories, he said, are “massively” higher than in either 2013 or 2014.

When asked if he would buy junk bonds, Gundlach said he was waiting for a time when prices aren’t “going down every single day.” “Those of us that have been around the block a few times know that catching a falling knife is one of the most dangerous things to do in market speculation,” he said.

He offered two investment recommendations. Rather than buying junk bonds or MLPs and betting for a recovery in those asset subclasses, he said investors should “buy oil.” But he did not say how prospective investors should structure that position. He also said that closed-end funds trading at deep discounts were very attractive relative to stocks.

Gundlach reiterated his prior forecast that U.S. entitlement spending (primarily Social Security and Medicare) will place a much higher burden on government finances, although he did not say precisely when that will occur.

The buildup in government debt, he said, “tries to prop up the economy at the expense of the future.” Zero-interest-rate policy pushes consumption forward and changes the discounting mechanism, he said. Indeed, there no discount mechanism, he said, so you “fully value everything.”

“Once you’ve done all of those things you are quite a few yards into the tractor pull,” he said. “And that sled is getting heavier and heavier and heavier. That is why it is getting harder and harder to make money.”

Read more articles by Robert Huebscher