Staking a permanent geographical claim to a part of the style box can be detrimental to a fund’s performance. Being geographically flexible, on the other hand, can be helpful. Recently, for example, avoiding energy exposure and gaining exposure to sectors normally found outside of the value managers’ typical habitats have been a boon for 27-month old value fund, DoubleLine Shiller Enhanced CAPE (DSEEX).

Before digging into this young fund and comparing it to its peers and relevant indices, it’s worth reviewing the recent history of value and growth indices. A value index isn’t always cheaper than, or poised to outperform, a growth index even for a decade. Value stocks may outperform growth stocks over multi-decade periods, as Fama and French showed, but they can lag for decade-long periods or more as well. And they can lag not because growth or glamor stocks are soaring manically, but because, somewhat counterintuitively, value stocks aren’t cheaper at all times.

Value isn’t always cheaper

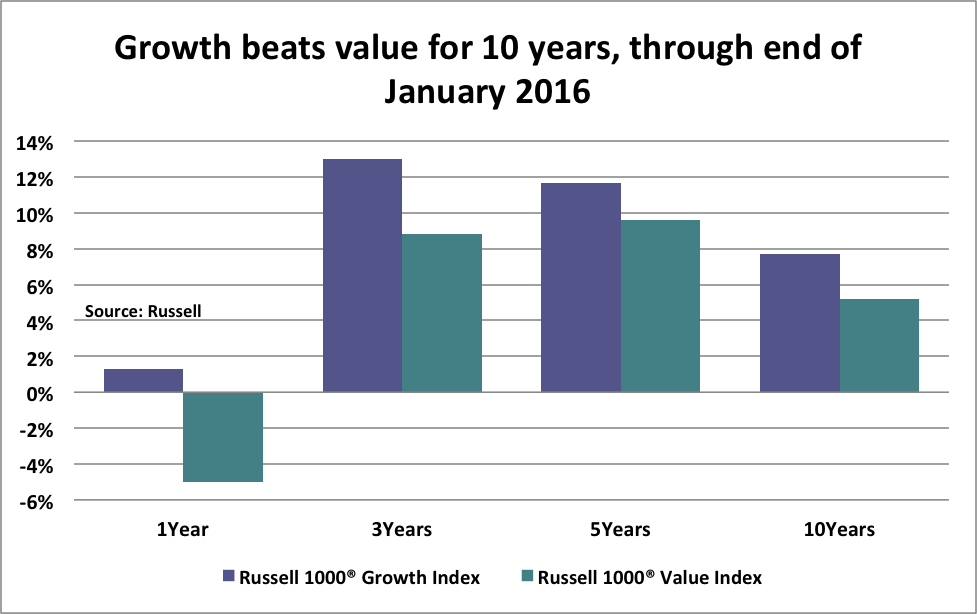

A glance at the Russell 1000 Growth and Value Indices shows that growth beat value consistently for 10 years through the end of January 2016. That outperformance likely resulted from the fact that growth stocks became cheap in the aftermath of the technology bubble bursting.

Many so-called quality businesses, with consistently high returns on invested capital, such as brand-name consumer products companies like Coca Cola, Colgate and Procter & Gamble found themselves in the bargain bins for a few years after the 2000-2002 meltdown, and especially after the stock market meltdown of 2008. The same is true for large technology companies such as Microsoft, Intel, and Cisco. From roughly the end of the crisis up until recently, for example, Grantham, Mayo, van Oterloo, which uses the Shiller PE among other metrics, has asserted that “quality” stocks were the cheapest within the U.S. market.

However, those companies never made it into value indices because they remained steady, slow growers with consistently high profits and continued to be priced higher on one-year trailing multiples than financials or energy. As a result, these companies got cheap enough to outperform for the subsequent decade through January 2016. This shows one-year trailing multiples may not provide the best assessment of value.

Likewise consumer discretionary stocks had strong runs after getting smashed during the financial crisis. They bounced back on the support provided by access to new (mostly Asian) markets of wealthy consumers seeking luxury brand goods. While the world entered recession in 2008, wealthy people didn’t stop spending for long.

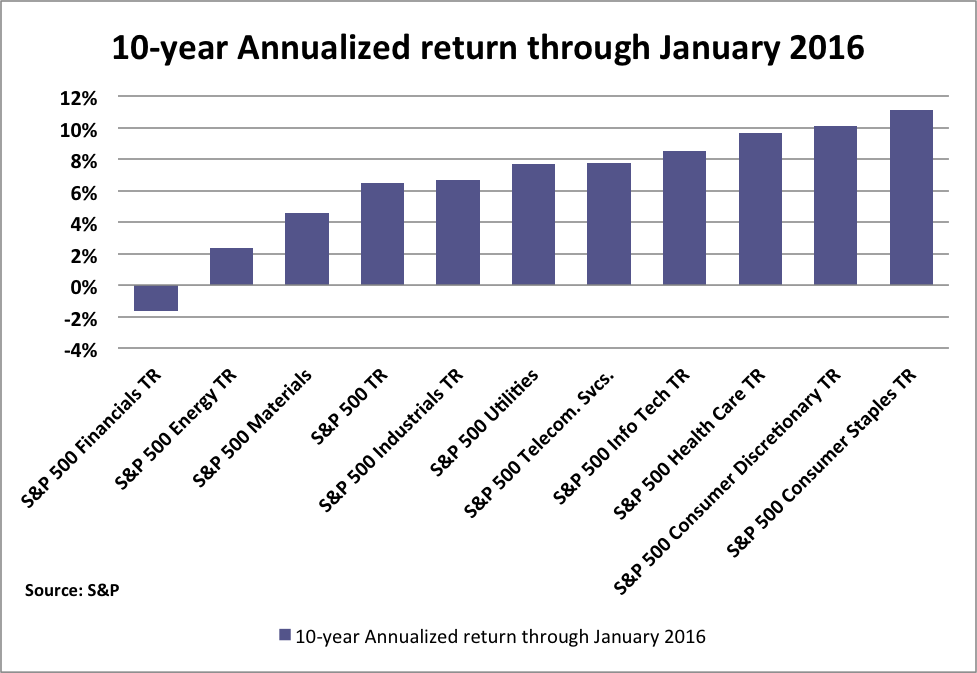

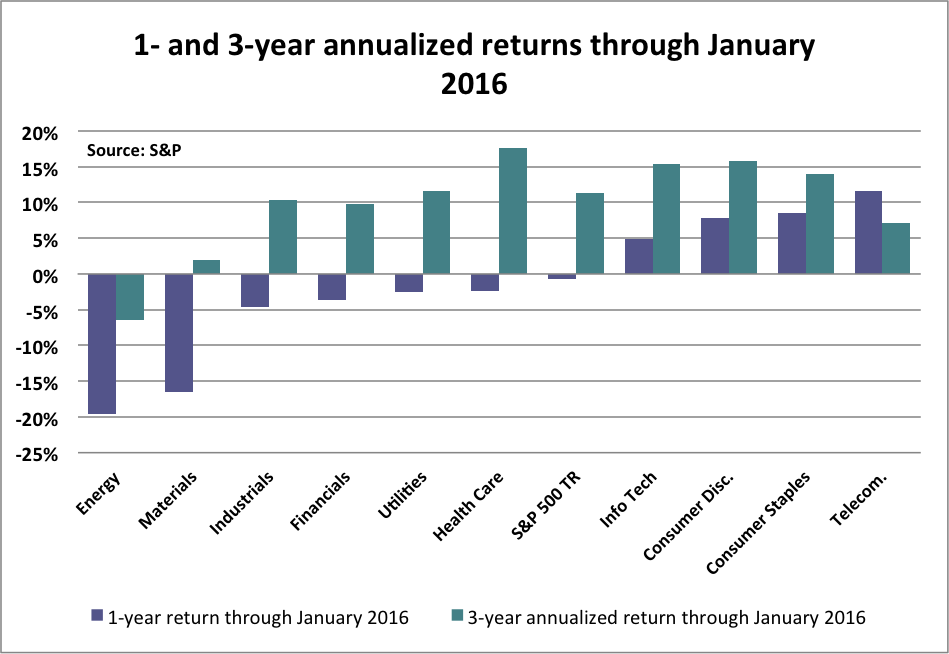

In contrast, traditional value stocks like financials that trade at typically low one-year trailing P/E ratios have had a difficult run owing to the financial crisis. And, most recently, energy and materials stocks, which are significant components of value indices and found in abundance in many value funds, have been terrible performers.

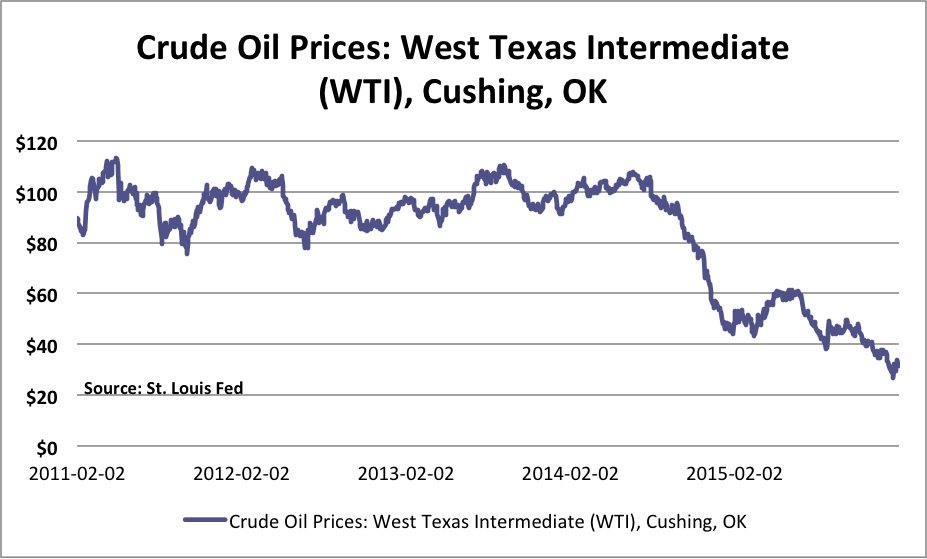

While nearly all commodities have dropped over the past few years, the decline in the price of oil has been particularly breathtaking.

Weak commodity prices have caused the energy and materials sectors to deliver particularly poor performance in recent years.

Tough times for value funds

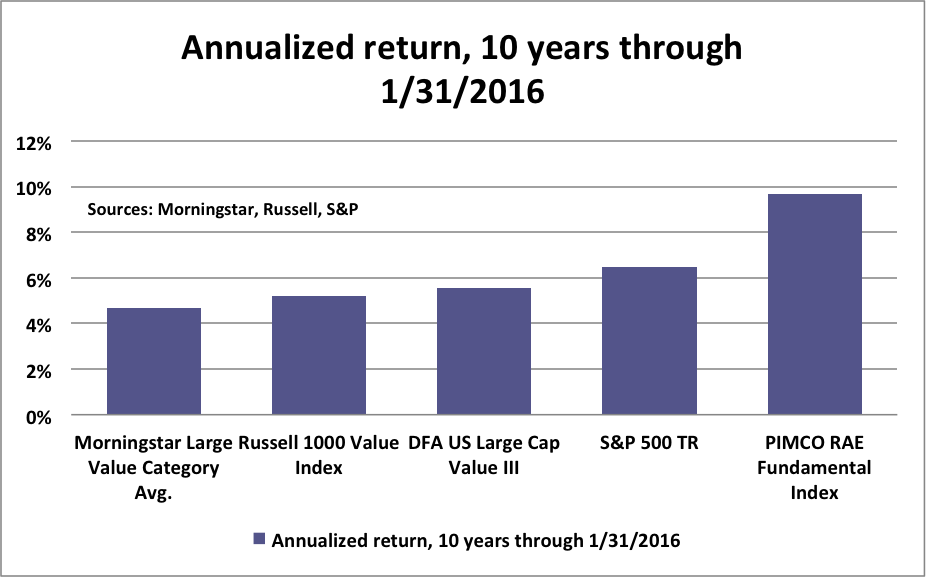

The following chart shows that value funds in aggregate have had a difficult time over the decade ending January 31, 2016. The Morningstar large-value category fund average annual return was 4.66% for the decade, while the Russell 1000 Value Index returned 5.19% annualized over that time. Both of those fell short of the S&P 500 Index’s 6.48% average annual return over that period.

OK, so much for the performance of value strategies under passive management -- market-cap weighted indexation -- and active management. How did rules-based value strategies perform over the same timeframe?

Let’s look at rules-based funds DFA Large Cap Value III – DFUVX – and PIMCO RAE Fundamental Index Plus – PXTIX. These are among the few value-focused, rules based funds with long enough track records to compete in this decade-long derby when value lagged both growth stocks and the S&P 500.

I used a relaxed definition of “rules-based.” The DFA fund uses discretion to fulfill its strategy to tilt a capitalization weighted index toward value stocks and smaller stocks, and the PIMCO fund gently modifies the rules of the Fundamental Index, which ranks stocks based on sales, cash flow, dividends and book value.

While the DFA fund has an explicit mandate to own value stocks (specifically stocks with low P/B ratios), the PIMCO fund does not. The Fundamental Index skews toward smaller stocks and value stocks, but it does that indirectly. That skew is more of a byproduct of its process to weigh companies on their economic footprint – sales, cash flow dividends and book value.

Both funds arguably “break the link” between market size and index weighting, as Research Affiliates, the creator of the Fundamental Index used (and modified) by the PIMCO fund, defines smart value, but they are not purely mechanical in their approaches or in fulfilling their objectives.

DFUVX and PXTIX both scored victories against the 4.66% annualized return of the Morningstar large value fund category and the 5.19% annualized return of the Russell 1000 Large Value index with 5.57% and 9.68% annualized returns. The DFA fund, however trailed the S&P 500 by 89 bps annualized.

The PIMCO fund’s raging success for the decade shows that a skew towards value didn’t hurt it. It’s possible that its skew toward small stocks overcame its value bent, but one might have expected that from the DFA fund as well. The Fundamental Index (and the tweaks PIMCO makes to it) thrived in an environment one might have expected to be unfavorable toward it.

Indifferent to style box geography

In contrast, the DFA fund couldn’t match the S&P 500 for a decade, hampered by its value bent. And the average fund in the Morningstar large-value category trailed the S&P 500 by 182 basis points annualized for a decade.

This leads to the question of whether there is a form of value investing that isn’t limited to one locale in of the style box. If stocks that generally trade at higher one-year trailing multiples than financials and energy companies can get too cheap but still not wind up in the value part of the style box, must investors in all value funds miss exposure to them?

Certainly individual active managers can notice that growth stocks represent better values than value stocks. Indeed tracking some good investors’ portfolios reveals a “style drift” or migration from value to growth over the past decade. But is it possible to construct a rules-based approach to seeking value that is indifferent to style box geography?

A value fund not limited to value sectors

The DoubleLine Shiller Enhanced CAPE fund represents that kind of approach. DoubleLine actively invests the fund in a fixed income portfolio, which generates a return for investors. The portfolio backs derivatives contracts giving the fund exposure to the Shiller Barclay’s CAPE Sector Index. This index is composed of sectors of the S&P 500 Index that are determined to be the cheapest on a cyclically adjusted P/E or CAPE basis.

The CAPE metric, devised by Yale economics professor and Nobel Laureate Robert Shiller, relates the price of a stock or an index to its 10-year average real earnings. It is most commonly used to value the entire S&P 500 Index by comparing the current CAPE to the historical average, but in the case of this index it applies to the ten sectors comprising the S&P 500.

Every month, the Shiller Barclay’s CAPE Sector Index identifies the five cheapest sectors on a CAPE basis relative to their historical averages. Then, in an effort to avoid value traps, it applies a filter to exclude the sector with the worst one-year total return. The index consists of the four remaining sectors.

As a result of applying the CAPE ratio to the S&P 500‘s sectors, the fund – while certainly a value fund -- isn’t limited to any part of the style box. The process chooses the cheapest sectors on a CAPE basis relative to their own histories. This means it could choose the most growth-oriented sectors and wind up in the growth part of the style box if those were the cheapest on a CAPE basis.

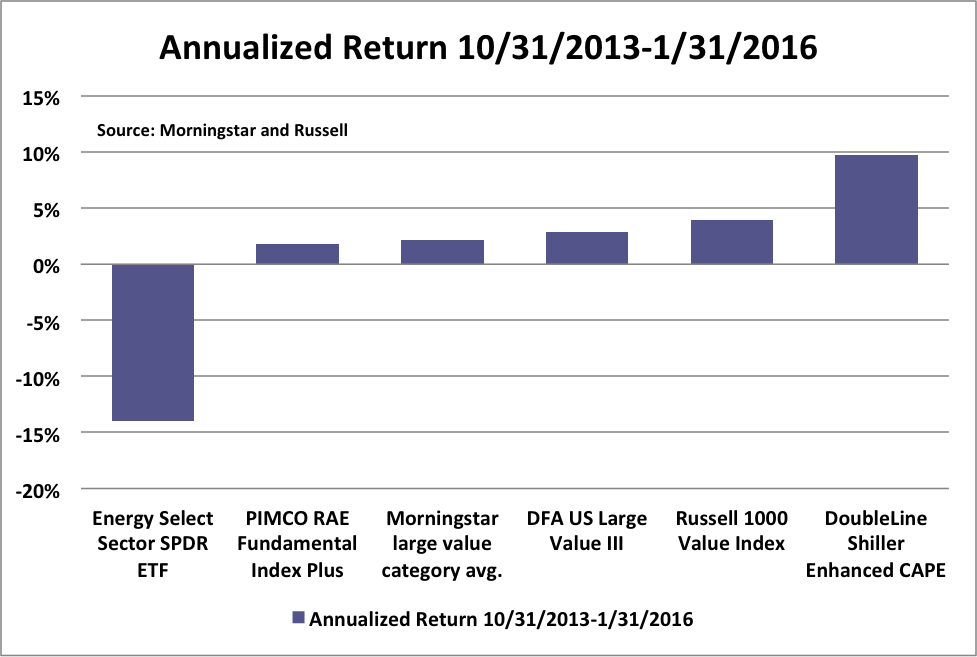

The fund has posted impressive performance for its 27-month existence. It has returned nearly 10% annualized while the Russell 1000 Value Index has returned less than 5%. Additionally, the DFA fund has posted a 3% annualized return, while the PIMCO fund has produced a 2% return.

The DoubleLine fund’s negative total return filter eliminated energy from the portfolio since the end of September 2014, despite the sector being cheap enough to make the initial cut for value on the CAPE metric. The elimination of energy has helped it considerably.

Interestingly, when the filter eliminated energy, consumer staples entered the fund. While not a fast-growing sector, staples are by no means deep value under conventional valuation metrics. Consumer staples companies often sport wide moats or sustainable competitive advantages through their brands, and post consistently high returns on invested capital. Their trailing one-year price multiples often reflect those strengths, excluding them from the value corner of the simplistic style box.

The fund has had exposure to consumer staples since October 2014, with the exception of October 2015 when the fund exchanged staples for materials. That trade lasted only one month, however. The staples sector replaced materials in November and has remained in the portfolio until January 31, 2016.

The rest of the portfolio consisted of technology, health care and industrials. With the exception of industrials, few stocks in these sectors are often found in the value part of the style box.

The negative total return filter has helped the fund considerably, but investors shouldn’t overlook that the fund has also benefited from its “pre-filter” agnosticism regarding sector choices and style box positioning.

The fund hasn’t received a position in the Morningstar style box yet because it doesn’t have a three-year track record. In nine months, when it reaches its three-year anniversary and Morningstar reveals its position, it may well not be on the value side of the style box.

Conclusion

While 27 months of outperformance isn’t reason to buy a fund, a sound, rules-based value approach is, and the DoubleLine Shiller Enhanced CAPE fund has one.

Warren Buffett has often said “growth is a part of value,” meaning value investing isn’t limited to or defined by, stocks and sectors with the lowest trailing one-year P/E and P/B multiples that aren’t growing. Lower trailing multiples don’t always indicate value, and higher multiples don’t always indicate ephemeral glamor that will never deliver returns.

Low trailing multiples can certainly deliver higher returns. But, it’s also true that high trailing multiples may not indicate an overpriced sector when evaluated on a cyclically adjusted basis. In the DoubleLine Shiller Enhanced CAPE fund, investors have a rules-based value fund that approaches the world with similar flexibility.

John Coumarianos is a freelance writer. He has worked as a branch representative at Fidelity Investments, a mutual fund and equity analyst at Morningstar, and a writer at Capital Group. He also runs the website/blog Institutional Imperative.

Read more articles by John Coumarianos