Today’s financial planning tools, including the new generation of “robo” advisors, have profound shortcomings, according to Dan diBartolomeo. DiBartolomeo says that the technology most advisors use suffers from serious problems – from prescribing a costly regimen of ongoing portfolio rebalancing to failing to incorporate a holistic balance sheet of assets and liabilities – and these problems are unwittingly depleting their clients’ assets.

DiBartolomeo’s company, Northfield Information Services, has introduced a new product, WealthBalancer, to address those shortcomings. DiBartolomeo is the founder and CEO of his Boston-based firm, and I spoke with him on April 14.

Northfield’s core business is in providing analytical tools to institutional investors. This effort extends the availability of its product suite to the advisor market.

“The problem we are trying to solve for investment professionals – mostly the advisor community, who deal with the range of household investors – is that most of the analytical tools they use aren’t very good,” diBartolomeo said.

Background

The genesis for WealthBalancer was in 2005, when the CFA Research Foundation asked diBartolomeo, Jarrod Wilcox and Jeffrey Horvitz to write a textbook on how managing taxable household assets is different from institutional money. “As you think about how a family evolves through time,” diBartolomeo said, “things change much more than institutions.”

Along those lines, he said, the “preference functions” of families are much more complex and nuanced than those of institutions. For example, households deal with a constantly evolving suite of financial needs, ranging from education expenses to retirement planning, whereas institutions have far more predictable cash-flow needs.

About six or seven years ago, diBartolomeo and Wilcox began to develop WealthBalancer, which he said has “the right mix of concepts and functionality to serve everyone from a traditional trust company to an RIA to a salesforce at an insurance company or a broker dealer.”

How it works

A WealthBalancer user enter three sets of information. First is the lifetime balance sheet, which contains a series contingent assets and liabilities. For example, a contingent liability might be the money necessary to send a child to a private school, but with the caveat that he or she might go to a public school instead. An example of a contingent asset is an inheritance of an uncertain amount.

WealthBalancer lays out all one’s financial needs and goals simultaneously and holistically. It looks at the whole picture and asks, “How much risk can this client afford to take?” This is not necessarily the same as what the client considers acceptable. Risk in this sense is measured by how leveraged one’s life is; it compares one’s household assets to liabilities to determine leverage.

DiBartolomeo said that this approach is unique in that it is analytical (not a “gut feel”) and it can be projected over time, showing how one’s risk varies over one’s lifetime.

Second, WealthBalancer understands asset allocation and asset location (i.e., whether a fund is held in a taxable or tax element account)

The third element is what diBartolomeo called “arbitrary preference functions.” Every firm has a questionnaire, he said, but the problem is that firms use the answers haphazardly. Using a scientific approach taken from the field of industrial engineering, WealthBalancer analyzes client responses to the questionnaire.

The firm running WealthBalancer sets up the questionnaire, which is completely customizable. It can be tailored to the type of investor. For example, the questionnaire can ask whether a client has a preference for socially responsible investing, plans to live abroad or has certain risk tolerance characteristics.

“What’s unique is how the math works behind the scenes,” diBartolomeo said.

What clients will see

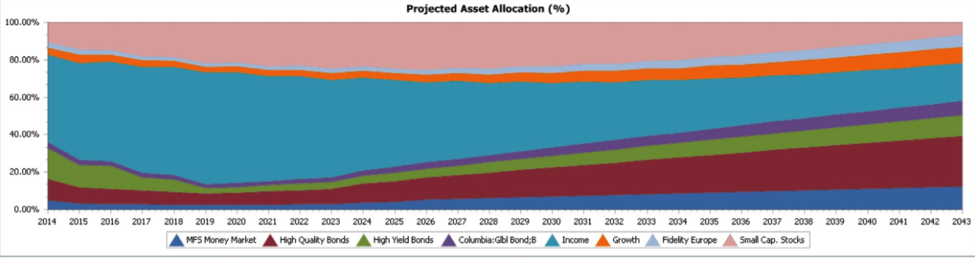

The output of WealthBalancer is something diBartolomeo said is very unusual. Most systems, he said, provide an asset allocation, but WealthBalancer provides an asset allocation now and over one’s lifetime, as in the example below:

That’s important, diBartolomeo said, because it allows the investor to manage the transitions to different asset classes through cash flow rather than rebalancing. This is particularly relevant for taxable money, he said, because moving funds is costly. With WealthBalancer’s “forward view,” he said, one can make better judgments about whether clients will reach their goals, and it makes investing much cheaper by reducing taxes and transaction costs.

“Every time something changes in one’s life or in the market, you revise the input and get a new plan,” he said. “You minimize rebalancing and manage asset allocation though cash flows, which is a lot less costly.”

“Every commercial you see on television talks about a plan,” diBartolomeo said. “But they aren’t really plans because they lack a set of intended or contemplated actions. They say this is what to do now, and we will come back in a year or two and revise it.”

With WealthBalancer, advisors and their clients get plans that are dynamic over time and incorporate multiple cash-flow streams that represent the assets and liabilities that a household anticipates.

WealthBalancer is product agnostic. When a firm implements the product, it defines its own asset classes and products (including individual securities, ETFs, mutual funds and annuities), along with assumptions about returns, correlations and the tax consequences of the products it uses. Firms also control the definitions within the questionnaire and the mapping of preferences. For example, if a client wants to be socially responsible, the firm defines (in a prescribed mathematical framework) which products meet that criterion.

WealthBalancer produces an asset allocation based the client’s risk profile, such as in the example above, and another based on the client’s risk tolerance. It is the advisor’s role to work with the client to reconcile the two and determine a reasonable asset allocation that will achieve the client’s financial goals.

WealthBalancer does not make the traditional differentiation between the accumulation and de-accumulation phases of retirement planning. Clients can have as many cash flow streams or events as necessary, and those get unified through the balance sheet.

Subsuming robos and financial planning applications

DiBartolomeo said that WealthBalancer will subsume most financial planning and robo products because of its far-reaching output. But it is meant to operate at the asset-class level. It contains nothing about individual securities, funds or ETFs.

WealthBalancer contains an “analyst module,” where a firm enters its capital market assumptions, suite of products and its questionnaires. There is an “advisor module” that imports and sets up clients, updates portfolios and provides client-facing reports. DiBartolomeo said that the typical client can be set up in about 10 minutes.

The analyst piece runs as a traditional desktop application, but the advisor piece runs on phones, iPads, Androids or the web.

DiBartolomeo said that WealthBalancer has been through a long process of beta testing with RIAs and family offices and was then showed to existing Northfield clients, including many large trust companies that manage ultra-high net worth assets. The feedback has been extremely positive, he said.

One person who has reviewed WealthBalancer is Bernd Scherer, a managing director at Deutsche Asset Management and the person in charge of its robo-related initiatives. Scherer said that Northfield’s offering “provides current best thinking in private portfolio choice and value added far beyond a narrow focus on cost savings.”

In a paper in the most recent edition of the Journal of Investment Management, Harry Markowitz and Ken Blay proposed a method for investing over time with a mix of taxable and tax exempt accounts. They concluded by saying that it would be nice if something like what they proposed existed.

“Well,” diBartolomeo said, “we already have done that.”

Read more articles by Robert Huebscher