Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

We recently published our first book, Adaptive Asset Allocation: Dynamic Global Portfolios to Profit in Good Times – and Bad. It spent roughly six weeks as Amazon’s #1 Hot New Release in Investments, and we’re pretty psyched about that.

In our book, we spend a great deal of time extending the research and concepts we explore on our blog, GestaltU. We did this in order to distill the most salient points, and also to tie seemingly disparate topics together into a cohesive narrative. We cover topics like behavioral economics, market valuations and expected returns, factor investing, retirement income planning, and a spectrum of asset allocation strategies. The book was meant to stand as a comprehensive but accessible reference for what ought to matter to modern investors.

Today, we’re proud to share a few sample chapters with the community at Advisor Perspectives. Specifically, below you will find:

- Chapter 25, which discusses the differences between strategic, tactical and dynamic asset allocation.

- Chapter 26, which addresses the “optimization machine,” our term for the connection between philosophical beliefs about markets, and how they are expressed in portfolios.

- Chapter 27, which covers the flaws – and salvation – of mean-variance optimization.

- Chapter 34, which provides a concise taxonomy of portfolio optimization methods.

Not included in this post are Chapters 28-33, which discuss in detail the spectrum of portfolio optimization methods from buy-and-hold traditional balanced; through strategic portfolios that embrace structural diversification like the Permanent Portfolio; evolving to inverse volatility weighting, robust risk parity, and minimum variance; and finishing with our flagship strategy, Adaptive Asset Allocation.

We cover the entire spectrum from passive to active asset allocation because investors are far more likely to stay committed if their investment methodology aligns with how they believe markets work. But that’s a topic for another day.

For the moment, we hope you enjoy the sample chapters below.

Part IV: An Investment Framework for Stability, Growth, and Maximum Income

This is where the rubber hits the road, so to speak.

Given current difficult market conditions, the traditional means of portfolio management simply won’t help investors achieve their financial objectives. Static stock and bond portfolios, strategic asset allocation, and buy-and-hold might work during certain market regimes, but if they didn’t get the job done over the last 13 years, and we’re expecting 20 more years of the same, something’s got to change.

This situation calls for flexibility, responsiveness and adaptability. The Adaptive Asset Allocation (AAA) framework embraces all of these qualities, and was largely developed in response to the issues we’ve posed thus far.

As Darwin said, “It is not the strongest of the species that survives, nor the most intelligent. It is the one that is the most adaptable to change.”

Chapter 25: A Word about Asset Allocation

Before beginning, we need to deal with some issues of nomenclature. For the remainder of this book, we will use the terms ‘policy portfolio’ and ‘strategic asset allocation’ somewhat interchangeably. However, it’s important to understand what they are and how they are similar and different.

A policy portfolio is a long-term prescribed asset allocation. For example, the ubiquitous 60% equity / 40% fixed income (balanced portfolio) is a common policy portfolio for private investors and many institutions. A manager that holds the policy portfolio in appropriate weights at all times without active deviation, and rebalances back to the prescribed weights on a regular basis, practices Strategic Asset Allocation (SAA). So SAA is simply a passively rebalanced manifestation of a policy portfolio.

In contrast, a manager that actively deviates from the policy portfolio is said to practice some tactical asset allocation (TAA). Traditionally, TAA is a practice that applies even when a policy portfolio has been declared. Though the manager is free to deviate from the stated guidelines, often the manager won’t deviate too far.

Further out on the asset allocation continuum is dynamic asset allocation (DAA), which is unconstrained allocation among all of the eligible assets in the investment universe. The universe is probably specified in advance—hopefully it is robust and coherent as we will discuss below—but no policy weights are assigned to the assets. A manager who practices DAA can hold all assets, none of the assets, or anything in between at his or her discretion.

You can see that asset allocation runs along a continuum from strategic at one end, with no active portfolio bets, to dynamic at the other end, with exclusively active portfolio bets. The question is: What would motivate an investor to choose a strategic, tactical, or dynamic approach? The answer lies in what the investor thinks he knows about the way assets behave. Let’s explore that.

Chapter 26: The Optimization Machine

No matter how one invests, it’s important to identify and understand the assumptions that underpin a methodology. All investors embrace, to varying degrees, two important assumptions.

Based on theoretical models and long-term observations, practitioners of SAA implicitly expect assets to respond in specific ways to different market environments. For example, they expect government bonds to do well when the economy is doing poorly and inflation is low, and they expect stocks to respond positively to economic growth. Also, they expect stocks to be more volatile than bonds, and they expect them to move to the beat of different drummers. The specific qualities of these structural relationships may change incrementally over time, but the basic understanding of asset relationships is broadly indelible.

Alternately, investors who choose to practice tactical or dynamic asset allocation implicitly believe that they can estimate the salient features of assets through time in response to changes in the economic or financial landscape. Often, these estimates are qualitative, so that they are based on a narrative or “feeling in the gut” about what’s going on in markets at that moment. These estimates tend to be “ordinal” in nature, which just means an investor knows which assets he likes most and least, but can’t quantify the magnitude of differences.

Other times, however, estimates are quantitatively derived from historical data series or economic variables. These estimates tend to be more precise and, where a long history exists for the assets under investigation, they can be tested for accuracy using statistical methods. More importantly, statistical methods also quantify how confident one should feel about these estimates, which helps inform how much faith we should place in them when we apply them for allocation purposes. The best approaches to investing—the ones most resilient to ever-changing and risky markets—incorporate a strong fundamental understanding of the structural nature of assets in a portfolio with a realistic understanding of the limits of statistical estimation.

An investor’s absolute and relative balance of confidence in his ability to estimate the merits of an investment as they change over time, versus his faith in theoretical or structural relationships, should determine the approach to asset allocation. An investor with no edge in estimation would be better off sticking with tried and true SAA based on sound financial principles. On the other hand, where an investor feels he has an edge in estimating changes in the character of assets over time, he might choose to use this information to implement TAA or DAA.

Some investors might have very little faith in the structural nature of assets, and no confidence in their ability to estimate the nature of assets by observation over time. Such an investor, with no information whatsoever at his disposal about the relative merits of assets in his portfolio, may logically choose to implement a policy portfolio that holds all of the assets in equal weight. This is the neutral position for investors with no edge [Addendum: an equally plausible neutral position is the Global Market Portfolio]. An investor who holds a mix of assets in a portfolio that deviates in any way from equal weight (including common practices like holding a capitalization-weighted index such as the S&P 500) is, whether acknowledged or not, acting on a set of assumptions.

Traditional investors who practice Strategic Asset Allocation (SAA) are implicitly making strong assumptions about the long-term return, risk, and correlation qualities for each of the assets in the portfolio. They are also making strong assumptions about which assets to include in the portfolio, and which ones to exclude. By restricting the universe—for example, to domestic stocks and bonds, as most investors do—they become vulnerable to the opportunity cost of missing out on returns from sources not included in their portfolio. In addition, these adherents to a policy portfolio SAA approach are making the strong assumption that it is not possible to add value to the portfolio by using dynamic estimates to alter the portfolio through time in response to new information.

At the other end of the spectrum, investors who assume that the salient behaviors of assets can be estimated with some confidence over time are not compelled to choose an allocation that will work well in all environments, with commensurate opportunity costs and risks. That’s because the estimates themselves help to identify the optimal combination of assets at each rebalance period. Depending on the degree of confidence about which asset features are estimable—volatility, correlations, or returns—these investors may pursue a variety of optimization techniques to improve portfolio performance. We will explore many of these methods in the chapters that follow.

We affectionately call the integration of structural assumptions, a thoughtfully diversified investment universe, and the application of varying optimization approaches the optimization machine. The goal is to achieve robust, resilient portfolios over time, and like any machine, the quality of the output is dependent on the quality of the inputs.

Chapter 27: Garbage In, Garbage Out

Practitioners, academics, and the media have derided nearly every investment method at one time or another, but the grumbling regarding modern portfolio theory, or mean-variance optimization (MVO), has become outright disgust since the technology bubble burst in March, 2000. This is largely because the dominant application of the theory, which uses strategic asset allocation at its core, delivered poor performance and high volatility over the last 14 years, particularly during bear markets.

SAA, as it is generally applied probably deserves its bad name, but the portfolio mathematics described by Markowitz are beyond reproach. The math is the math. Markowitz demonstrated how to build an optimal portfolio—that is, a portfolio that delivers the highest return at each level of risk—by thoughtfully integrating just three parameters:

- Expected volatility

- Expected correlation

- Expected returns

The trouble with SAA, as it is typically applied, is that investors utilize estimates based on long term average observations from history to create their optimal portfolios. As we discussed at length in Part 1, long-term averages turn out to be poor estimates of volatility, correlation and returns over the 5-, 10-, or even 20-year horizons that matter to most investors. So is it any surprise that, upon putting faulty estimates into the Optimization Machine, the output has been disappointing?

At the end of the day, it’s not the math that’s failed since the turn of the millennium; rather it’s a tragic misapplication of financial theory.

You see, the problem with averages is that they hide a great deal of important information beneath the surface. There is an old cartoon that shows an economist with his head in the oven and his feet in the freezer, while the caption in the middle reads, “On average, I feel great!” Markets are a lot like that. While the really long-term average might matter to an investor with an infinite time horizon and no cash flows, most investors don’t tick these two boxes. Rather, as we covered earlier in this book, by the time most investors have a meaningful amount to invest, their financial investment horizon is at most two or three decades. But even that overstates the reality of the situation, because most investors tend to abandon an investment after three to five years of underperformance.

In other words, most investors are unable or unwilling to commit for enough time for the long-term average to assert itself. This begs the question: If an investor can’t commit to a strategy over a timeframe that allows the averages to play out, why use long-term averages as estimates for the construction of a portfolio at all?

It is instructive to start this exercise by looking at just how far markets have strayed historically from these averages, and then discuss ways to deal with this problem.

Volatility

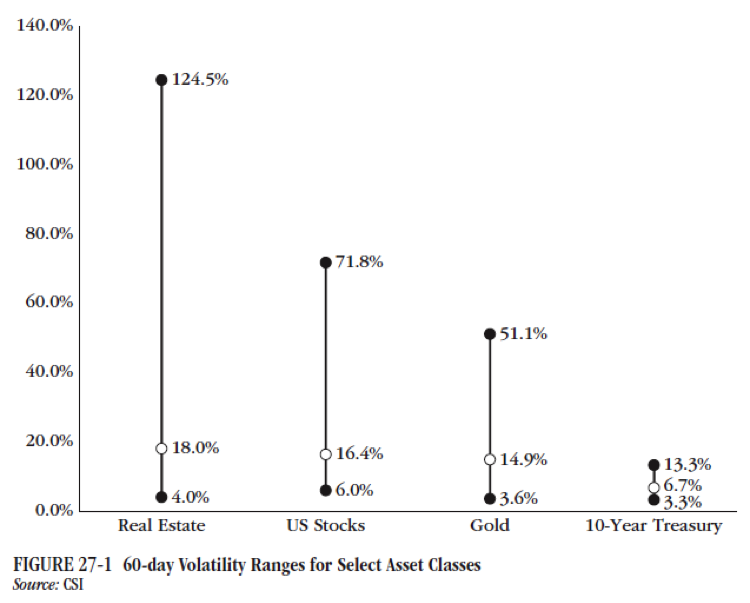

While assets generally exhibit a long-term volatility character, observed volatilities for all assets stray very far from their average state from time to time. For example, while average 60-day equity index volatility is around 16% annualized for stocks, we sometimes observe stock volatility to be well under 10% in calm, trending markets, or more than 70% in panicky bear markets. This dynamic is not unique to stocks either, as illustrated in Figure 27-1. Even Treasury volatility ranged between 3% and 13% from 1990 to 2013.

This has a dramatic impact on the risk profile of a typical balanced portfolio, and therefore on the experience of a typical balanced investor.

Correlations

Imagine a flock of birds in the sky, or a school of fish swimming together in the ocean. While each group contains individuals that can make their own decisions, as a group, they tend to move in the same direction almost simultaneously. It is visually striking to watch them move together in near perfect unison as if they were connected by invisible strings. In fact, we can describe the relationship between the birds or the fish as having a nearly perfect correlation. The degree to which the individuals in the group are connected is a function of their correlation.

Correlation is quantified via a statistic called the correlation coefficient, which varies between –1 (moves in opposite directions) and +1 (moves in the same direction). A coefficient of 0 indicates no relationship.

A common misconception is that two securities with a perfect negative correlation will cancel each other out, leaving a portfolio return of zero, but this is not the case. Correlation describes the degree to which two securities deviate in the same direction from their respective average returns. In this way, two securities can be perfectly negatively correlated (coefficient of –1) but also move in the same general direction over time.

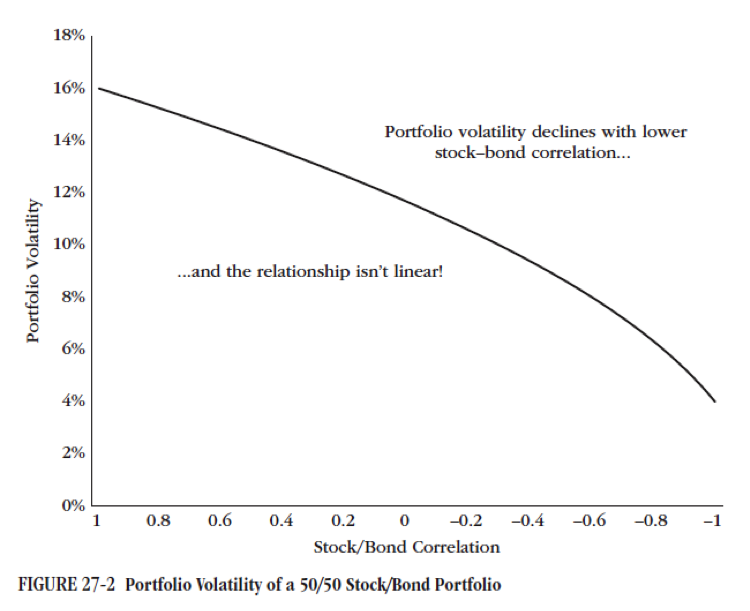

Stocks and bonds provide an intuitive example of this phenomenon. Both stocks and government bonds exhibit positive long-term average returns, but they are negatively correlated over the long term. In this way, while the average volatility over long periods of time (not the 60-day period from above) of stocks is 20% and the average volatility of long-term government bonds is 12%, the long-term realized volatility of a 50/50 stock and government bond portfolio is 10.6% rather than 16%, which is the average of the two securities.

In fact, the mathematical relationship between volatility and correlation was the breakthrough that landed Harry Markowitz his Noble Prize in Economics. From his work, it can be demonstrated that portfolio volatility always declines as correlation trends from +1 to –1.

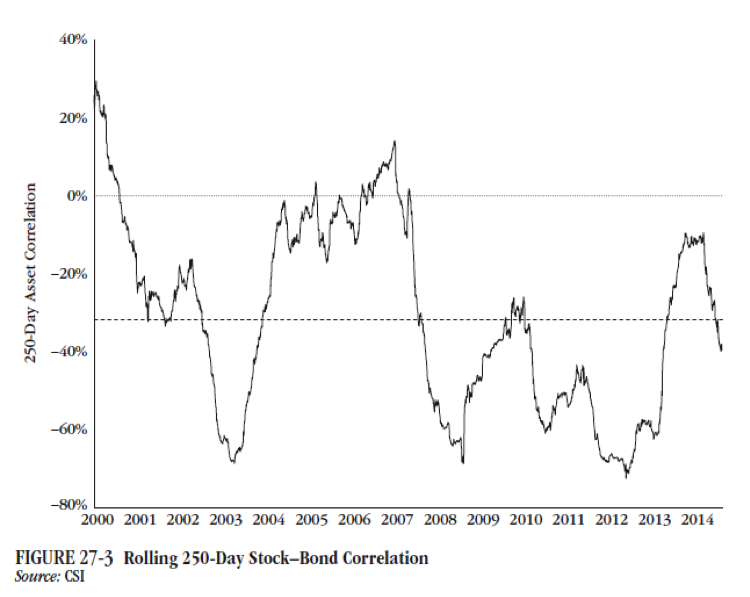

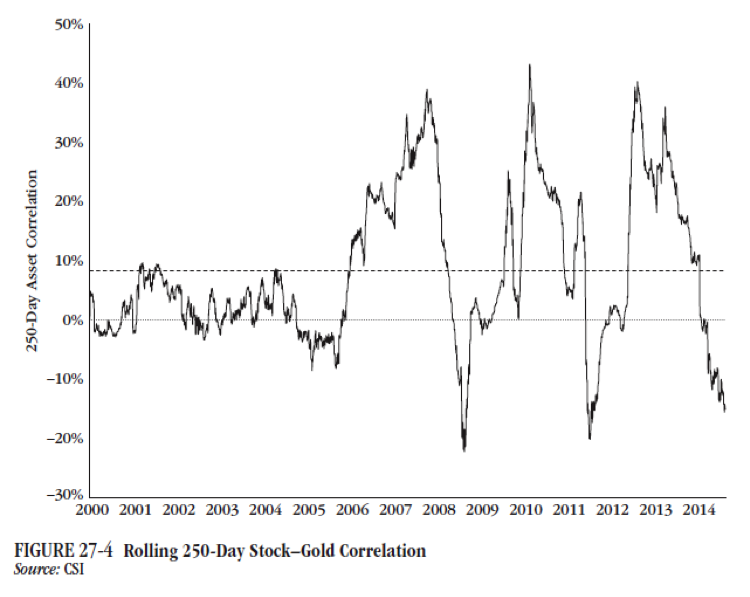

In practice, most Advisors make long-term assumptions about correlations between assets. But actual correlations between assets can vary widely over time. While the long-term correlation between U.S. stocks and Treasuries, and U.S. stocks and gold, are low or even negative over the long term, the actual realized correlation between these assets oscillates between strong and weak over time.

From Figures 27-3 and 27-4, notice that the long-term average 250-day rolling correlation between stocks and bonds over the 13-year period shown is –0.32, and the correlation between stocks and gold is +0.09.

However, the stock/bond correlation varies between –0.72 and +0.29 over the period, and the stock/gold correlation varies between –0.22 and +0.43. You could fly a jumbo jet through those ranges.

The current correlation has an enormous impact on portfolio volatility. In fact, if we revisit the relationship between correlation and portfolio volatility from Figure 26-2, the volatility of a 50/50 stock/bond portfolio increases by 100% as correlation increases from –0.8 to +0.2, holding all else constant.

Returns

We spilled quite a bit of ink in Part 1 describing the wide range of returns that markets have historically exhibited over horizons that matter to most investors. Recall that over the 20-year period from 1980 through 2000 equities delivered annualized total returns of almost 18% per year. At the other end of the spectrum, over the 20-year period following the 1929 stock market peak— through the Great Depression and WWII—U.S. stocks earned average total returns of just 1.9% per year.

It’s interesting to note that a balanced portfolio has also exhibited quite a wide range of returns over the past century or so. A balanced portfolio has delivered as little as 3.1% per year for 20 years, and as little as 4.4% per year over 30 years! Another way to think about what this means for investors is to quantify the likelihood of negative returns.

Many Advisors and investors would be surprised to learn that, examining all the 10-year periods since 1900, a balanced portfolio has presented investors with negative nominal returns over 15% of time!

This amount of variability in returns means the difference between living on food stamps after 10 years of retirement and leaving a multimillion-dollar legacy for heirs. In other words, the use of long-term average return estimates is analogous to a game of Russian roulette, where luck alone decides your fate.

The Flaw of Averages

For the record, it only takes a single faulty parameter estimate to drive portfolio optimization off the rails. In the case where even a single parameter estimate is materially off, the best possible outcome is a suboptimal portfolio. The worst-case scenario can, as experience informs us, be catastrophic. Imagine how a portfolio might behave if not one, but all three, of these estimates are off.

It is our contention that long-term average asset behavior is important to a point, especially to the process of choosing a robust and coherent investment universe. However, the importance of these estimates should not be overplayed, and they definitely should be minimized as inputs to a thoughtful portfolio optimization process.

At the end of the day, garbage long-term average estimates in, garbage portfolio results out.

This is what the Optimization Machine is about: understanding how to best integrate what we know about how assets should behave, how they’ve actually behaved over their entire price history, and how they’re behaving right now - in real time. Depending on the quality of our parameter estimates, several investment strategies could be optimal. And as we fashion ourselves objective researchers, there seems no better place to start than to assume that not a single parameter is estimable.

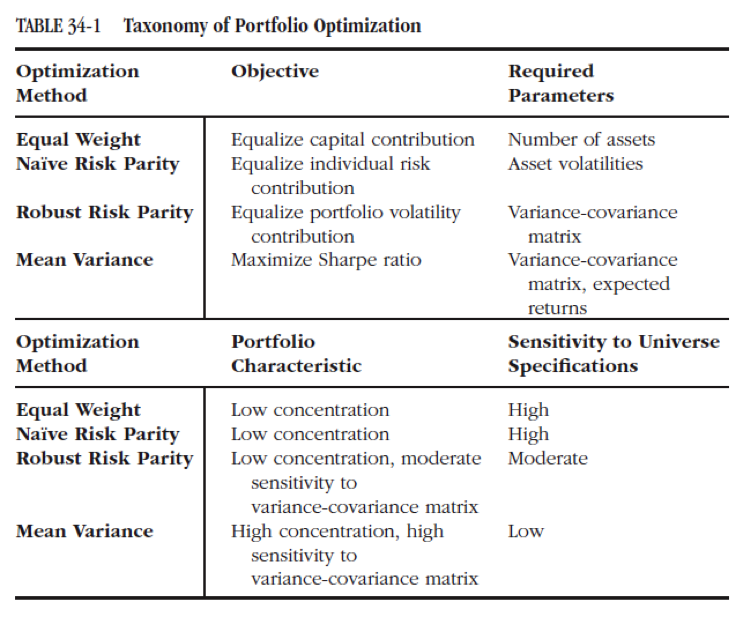

Chapter 34: Summary of the Optimization Machine

Table 34-1 summarizes the Optimization Machine, building from equal weight all the way through to mean variance optimization.

Note that equal weight portfolios require no estimates for any portfolio parameters, as each asset is weighted in proportion to 1/number of assets in the portfolio. This portfolio is therefore not vulnerable to poor estimation of risk or return parameters; however, it makes strong assumptions about the quality of the investment universe. If the universe is well diversified, such as the traditional stock/bond/gold/cash universe of the Permanent Portfolio, then this allocation mechanism can perform quite well. Alternatively, if the universe lacks robustness or is incoherent, an equal-weight portfolio is probably not the best solution.

At the other end of the spectrum, mean-variance type optimizations require very few assumptions about the quality of the universe because the optimizations make use of the covariance matrix to enforce optimal levels of diversification. However, these techniques are highly dependent on the accuracy and stability of parameter estimates.

Thus, you can see that there is a trade-off; naïve optimizations require very well-specified universes and confidence in how assets will behave. Conversely, robust optimizations, where an investor is confident about parameter estimates, require no assumptions about how assets should behave because we are observing their behavior in real-time. Thus, they are able to overcome poorly specified universes.

Our research suggests that it is possible to merge a fundamental understanding of structural diversification with reliable estimates of portfolio parameters—volatility, correlation, and returns—to build optimal portfolios that adapt to ever-changing markets. We openly admit that confidence in parameter estimates varies, but over any meaningful period of time, their inclusion in our portfolio design methodology is absolutely warranted because they improve the risk-adjusted performance of a portfolio above what could be accomplished without these techniques.

Astute readers will note that in Table 34-1 there is an optimization method we haven’t yet addressed: mean variance. In the world of adaptive portfolios, mean variance optimization offers substantial flexibility and impressively short response times to evolving economic and market conditions. Read on and we’ll show you exactly what we mean.

The above excerpt is from the book Adaptive Asset Allocation: Dynamic Global Portfolios to Profit in Good Times – And Bad by Adam Butler, Michael Philbrick, and Rodrigo Gordillo of ReSolve Asset Management. Investors interested in learning more about Adaptive Asset Allocation can download a free whitepaper here. For more information about ReSolve please visit InvestResolve.com or our research blog at GestaltU.com.

Read more articles by Adam Butler