The much-ridiculed plan to build a wall on the Mexican border has dominated the political discourse since Donald Trump proposed it last June. But, according to Stephanie Kelton, we already have a wall and it is very tall and nearly insurmountable. It is the national debt.

The much-ridiculed plan to build a wall on the Mexican border has dominated the political discourse since Donald Trump proposed it last June. But, according to Stephanie Kelton, we already have a wall and it is very tall and nearly insurmountable. It is the national debt.

Until about a year and a half ago, Kelton was the head of the economics department at the University of Missouri at Kansas City. She took a leave of absence to serve as the chief economist for the Senate Budget Committee, representing the Democrats. Bernie Sanders is the ranking Democrat on that committee, and Kelton has more recently served as his economic advisor for his presidential campaign.

Kelton spoke on April 12 at the 25th Annual Hyman P. Minsky Conference on the State of the U.S. and World Economies at Bard College in New York. Copies of her slides are available here.

“There is a lot of talk about building a wall in the U.S,” Kelton said. “I can assure you we have already built it.”

The belief that the growing national deficit will constrain growth and burden future generations acts as a wall that is a barrier to doing “almost anything sensible,” according to Kelton. It stands in the way of nearly everything policymakers would otherwise do as good economic policy, she said.

Kelton has spoken at several conference for financial advisors (see here, for example). In this talk, she provided the additional context from her work in Washington about how policymaking ignores the economic theories that she – and many others – have articulated.

The gatekeeper of the wall

The congressional budget office (CBO) is the institutional gatekeeper of the wall. That agency, she said, is meant to assure that the federal government behaves in a fiscally responsible manner, by “scoring” legislation and running short- and long-term budget forecasts.

In her work with the Senate budget committee, she met regularly with the CBO to discuss its budget forecasts. During her first several months, she said the Republican majority called five or six hearings to deal with the debt crisis.

What is the CBO telling us? “Budget deficits drive up interest rates and that results in the crowding out of investment,” according to Kelton. That statement is taken as an unassailable fact, she said.

The prevailing doctrine, according to Kelton, is that federal borrowing is not a source of net saving to the non-government sector, but a use of savings. Therefore, more borrowing results in less investment, slower growth and lower productivity. That leaves the government with less revenue and higher deficits – and a higher probability of a fiscal crisis.

Those beliefs, she said, are “well entrenched in D.C., not questioned and universally accepted.”

“It is often said that nobody in Washington can agree on anything,” Kelton said, “except this.”

Indeed, Kelton played a series of recordings of politicians, including many of whom were or are candidates for the 2016 presidential election, making statements such as “we can no longer take money from the Bank of China and from our grandchildren” or the “crushing burden of debt.”

On this issue, the rhetoric from Democrats is indistinguishable from that of Republicans.

But what if those arguments are false?

That rhetoric extends to entitlements; Social Security, Medicare and interest payments on the debt are said to be the blame for the supposedly out-of-control federal deficit, Kelton said.

One party claims it is a revenue problem, and therefore the government should raise taxes. The other side argues it is a spending problem, and budget cuts are necessary. Kelton said that Mike Enzi (R-WY), the chairman of the Senate budget committee, is an accountant and has claimed that, by definition, a deficit means that you’ve overspent, and therefore the solution “is to cut.”

But what if those arguments are false? What if deficits don’t drive up interest rates? What if we are not beholden to China as our lender?

In her work in Washington, Kelton sought to persuade policymakers that that the answers to those questions are not what is dictated by conventional wisdom. She said that economists can do more to educate those at the CBO and elsewhere and to show that the assumptions most policymakers make are fundamentally flawed.

Indeed, Kelton said that we need the government to take a deficit position almost all the time. But virtually nobody in Washington would consider that position to be reasonable.

She said that some deficit hawks would “tar and feather” her for that belief; many want a constitutional amendment to the contrary and a gold standard to make it harder to run deficit

Kelton noted that Hyman Minsky argued that government deficits are a source of profits for the private sector. Markets need confidence, according to Minsky, and lose it when profits fail to meet expectations. She cited research from Fidelity showing that the massive deficits that were run in the wake of the Great Recession "led to a quick recovery" in corporate profits. A government that aims to "get its fiscal house in order" with, say, massive spending cuts and tax increases, could easily bring about a sharp decline in profits that crushes confidence going forward, according to Kelton.

Kelton distinguished her position from that of most Keynesians, who want deficits only when the economy is weak, and a surplus when it is strong, so the budget is balanced over the course of the full business cycle.

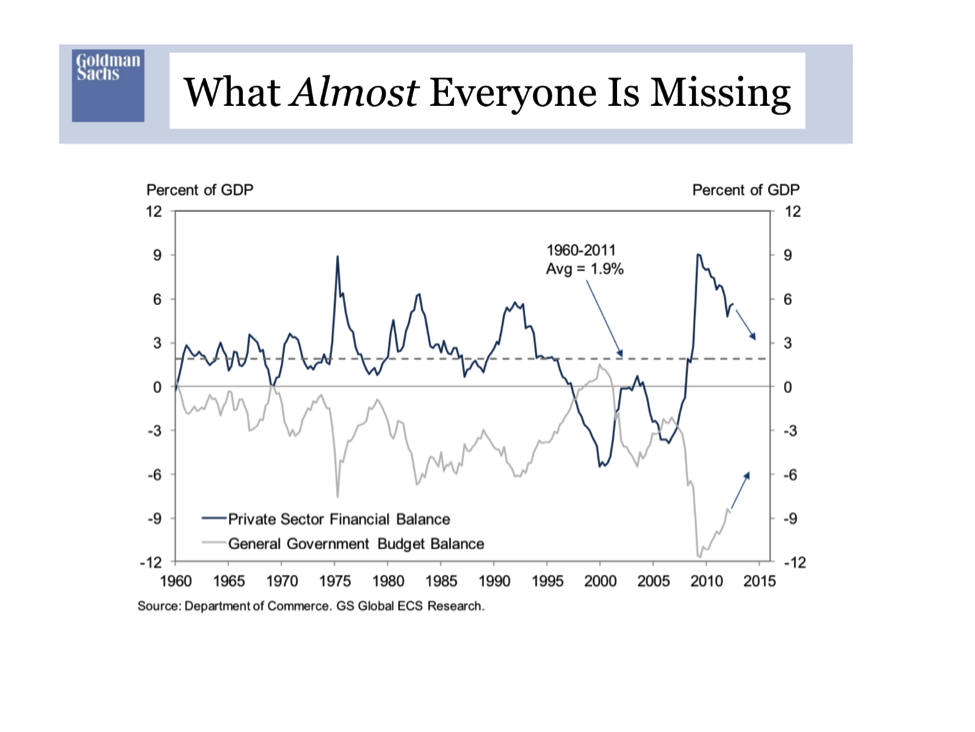

The most important chart in the world

“We are fundamentally misunderstanding basic accounting when we look only at the government side of the accounting ledger,” she said. Government deficits are, by definition, surpluses in the non-government sector, which includes the private and foreign sectors. That is an accounting identity.

The identity is illustrated by what she called “the most important chart in the world:”

This chart, which was originally created by Goldman Sachs, shows that as the government deficit grows, so does the private sector financial surplus.

Kelton was critical of the Simpson-Bowles recommendations, which were a product of the deficit reduction commission established by President Obama. It called for deficit reductions of $4.1 trillion over 10 years through a combination of tax increases and spending cuts.

Everybody was “gung ho” for it, she said. But if, instead, those recommendations were presented as a $4.1 reduction in private-sector financial balances, Kelton believes it would have had little support.

For those who are longing for the “good old days” of the Clinton budget surpluses of the late 1990s and early 2000s, Kelton offered a warning. The dot-com bubble and the emerging housing bubble (via wealth effect) fueled the leverage that caused household spending to significantly outstrip earnings (so households were spending more than their income, i.e., running deficits). All of that spending (accomplished by borrowing to finance the spending in excess of income) took the economy to full employment. Tax revenues (from capital gains and income) shot up, and spending to support the unemployed fell sharply. The economy was running full throttle and that is what balanced the budget and even pushed the budget into surplus, according to Kelton.

Kelton said that deficits can be too small and too big, but almost no one ponders the possibility that they can be too small. Everyone worries that they are too big, she said.

Is there a solution?

Kelton was not optimistic that policymakers will come around to her way of thinking.

The proper fiscal policy is to refrain from spending cuts or tax increases when faced with the prospects of slowing economic growth. “What feels right is wrong,” she said.

When your car skids, you naturally turn in the opposite direction, she said. But the driver’s manual tells you to turn into the skid to gain balance. “Go with the correction,” she said. “When you see the deficit increasing, the impulse is to reduce it by raising taxes and cutting spending.” But that has led to severe policy mistakes in Europe, for example.

Canada seems to have gotten this message, according to Kelton. It elected Justin Trudeau based on his promise not to balance the budget or to bring deficits down.

“Right now, in D.C. none of this is possible,” she said.

One idea, she said, would be make the dual mandate – price stability and full employment – the responsibility of Congress instead of the Fed. A policy guide like the Taylor Rule could be used to a guide to when to increase government spending or cut taxes, based on when GDP growth is needed.

Instead, Kelton said there is good reason to believe that the era of government shutdowns and debt-ceiling crises is not over. “This puts more pressure on the Fed,” she said. “It is pretty difficult to see where more aggressive fiscal policy will come from.”

She quoted Minsky, “We need to recapture our can do spirit and eliminate from the seats of power those of little faith and of little vision.”

Ironically, the presidential candidate who came closest to reaffirming Kelton’s principles was Donald Trump. In an interview on May 4, he proclaimed, “Don't forget, I'm the king of debt. I love debt."

Read more articles by Robert Huebscher

The much-ridiculed plan to build a wall on the Mexican border has dominated the political discourse since Donald Trump proposed it last June. But, according to Stephanie Kelton, we already have a wall and it is very tall and nearly insurmountable. It is the national debt.

The much-ridiculed plan to build a wall on the Mexican border has dominated the political discourse since Donald Trump proposed it last June. But, according to Stephanie Kelton, we already have a wall and it is very tall and nearly insurmountable. It is the national debt.