Are stocks’ glory days behind us? What about bonds? As the late Merle Haggard asked in song, “Are the good times really over for good?” A widely circulated McKinsey Global Institute (MGI) report, Diminishing Returns: Why Investors May Need to Lower Their Expectations, suggests that they are. The report makes the case that both stock and bond returns over 1985-2014 were exceptional and that investors should expect lower returns in the future.

McKinsey forecasts a real (inflation-adjusted) stock market total return, including dividends, that ranges from 4% to 5% in their low-growth scenario to 5.5% to 6.5% in their higher-growth scenario; those compare to a historical average of approximately 5.9% (since 1926). Both scenarios acknowledge the currently low growth rate of the U.S. economy – approximately 2% over the last several years, versus a historical average of 3.3% – but the second scenario has the growth rate gradually rising to its historical average.

The McKinsey report also makes forecasts for bonds. Their low-growth forecast is for a real return on 10-year U.S. Treasury bonds of zero to 1%, and their higher-growth forecast is for a real return of 1% to 2%. These numbers contrast sharply with recent bond returns, which have been high as interest rates have fallen.

MGI is correct, at least directionally, in their forecasts and for many of the right reasons. But its report fails to adequately address a few critical areas that should be of concern to advisors, as I will outline.

My biggest concern is that the report gives relatively high forecasts for equity returns but calls them low forecasts, as if the authors are sure investors are expecting even more. This is a subtle but important point; if the good news is that the bad news is wrong, someone ought to say so. After all, the report could have been titled “Oh No! Stocks Projected to Deliver Large Profits, but Less than During the Best Years in its History.” Other shortcomings include confusion as to when the best historical returns occurred and a failure to recognize that many investors rely on forecast methods that are better than merely projecting past returns into the future.

The equity returns projected by MGI are quite attractive. At real 4%, you double your purchasing power every 18 years. At real 6.5%, every 11 years. What more do you want? The great bull market of 1981-1999 may have accustomed investors to capital market conditions that were almost miraculous, but most investors understand that such an event is not repeatable. Someday in the far future we will have bull markets of comparable magnitude, but not soon and not starting from the valuation levels that currently prevail.

The main points of the rest of this article are:

- The really high returns in the equity market were earned over 1985-1999, not 1985-2014; the 2000-2014 period was far below average and below what MGI is forecasting, so they’re actually forecasting an increase in returns relative to the last 15 years. (My analysis goes through 2014 because that is what MGI’s did, even though 2015 data are now available.)

- As Eugene Fama and Kenneth French demonstrate, investors didn’t expect the high returns they got.

- The discount rates used by pension funds, cited by MGI as indicative of investor expectations for asset-class returns, are manipulated and are not an accurate guide to what investors really expect.

- Future returns on bonds will be much worse than they were historically; the report gets this right.

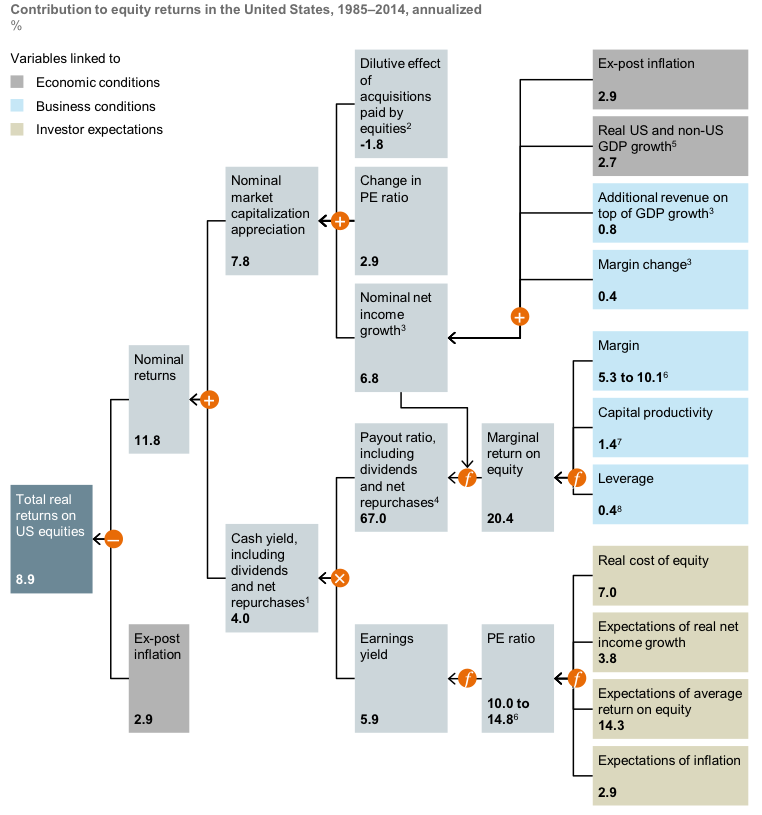

Finally, the MGI report introduces a decomposition model of stock returns. This analysis is of high quality and I reproduced MGI’s diagram of the model here for one asset class for one period (equities, 1985-2014) so you can see how MGI thinks about the return-generating process.

The glory days were 1982-1999, not 1985-2014

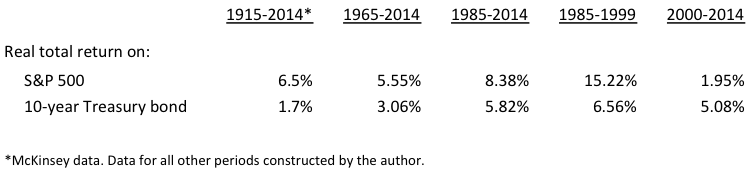

First, let’s look at the data. Here are compound annual real returns over various periods:

Exhibit 1

Compound annual real returns on principal U.S. asset classes

The stock market is what most people care about when they think of markets being good or bad. So it’s clear from Exhibit 1 that the glory days of the stock market ended in 1999; returns over 2000-2014 have been well below expectations (both investors’ own expectations for that period and MGI’s expectations for the future). It’s fatuous for MGI to talk about the last 30 years as if that were a single economic environment. And both they and I expect equity returns to rise, not fall, relative to the miserly standard set by the 2000-2014 period.

Bonds are a different matter. The bond bull market continued into the 21st century, and future bond returns will be lower because the starting yields are as low as you can get. Despite the Alice-in-Wonderland existence of negative interest rates in Europe and Japan, I do not expect them here, and that’s what it would take to produce significant further capital gains in the bond market. So the future for bond investors looks disappointing.[1]

Why were equity returns over 1982-1999 so high?

In the late 1990s, the late Ray DeVoe, the author of the brokerage firm Legg Mason’s wise and witty market commentary, made the case that future returns would be lower than recent past returns because of the overwhelming volume of good news that had already become incorporated into stock prices over the prior two decades. This news included the end of high inflation, a radical decline in interest rates, the end of the Cold War and collapse of the Soviet Union, the weakening of OPEC, deregulation, globalization, free trade, booming corporate profits and the emergence of the personal computer and the Internet. (DeVoe’s list was even longer; I’ve left out a good half of it.)

Starting in 1982, the market understandably reacted with a massive upward lurch, which was mostly over by 1999. Anyone who expected a repeat of this flood of good news over the subsequent 15 or 20 years would have had to be slightly daft. Yet the once-widespread method of projecting historical stock returns forward into the future led, in the late 1990s, to ever-increasing estimates of the expected stock return as markets continued to rise. By the turn of the millennium, the historical method produced an equity return forecast of 12%, something that could only happen – given the market’s already high level – under the most extraordinary circumstances.

Not only did those circumstances fail to materialize, but this young century has been a rougher ride than just about anyone expected. We have had two wars, a depression (not a Great Depression but a real one nonetheless) and a significant slowdown in emerging markets. The markets, already burdened with a high starting valuation, delivered some of the weakest returns in their history over 2000-2014, as Exhibit 1 shows.

Going forward, MGI expects real equity returns that are much higher than those realized over 2000-2014 (or 2000-2015; their analysis stops in 2014), and I expect this too. Their forecast is 4% to 6.5% per year in real terms. Thus the report’s title and the overall impression given by a superficial reading of the report are misleading. Their bond forecast – like mine – is for much lower returns in the future than over 2000-2014, which was an exceptionally good period for the bond market because of the decline of interest rates to unprecedented low levels.

Decomposing equity market returns

To understand past returns and make forecasts, MGI used a model that augments the conventional dividend-discount model (DDM) with macroeconomic information. This is a very helpful way to frame an equity (or bond) market forecast, and we reproduce their visual depiction of the model in Exhibit 2.

Exhibit 2

Drivers of equity returns[2]

This decomposition, or breaking up of return into its component parts, is useful for making forecasts. You replace each historical number with the number you think will prevail over your forecast horizon. The format makes it easy to debate the relevant inputs and to assess the accuracy with which each input is estimated. For example, the current dividend yield is quite accurately measured, while the rate of future change in the P/E ratio is anybody’s guess.

I note one objection to their method: The use of the real cost of equity as an input is circular because the output – the expected real return on the stock market – is also the real cost of equity. But that is not a major concern because the other, non-circular inputs have greater influence over the answer.

Were the high realized returns of the late 20th century expected?

Without explicitly saying so, the McKinsey report adopts the point of view that the historical returns that investors got are the returns they expected. This view – that investors conform their expectations to what can be earned in the market so that one can use realized returns as a guide to expectations – is closely linked to my former employer Ibbotson Associates, which made and, under the flag of Morningstar, still makes forecasts that depend on this assumption.[3] (To their credit, Ibbotson/Morningstar also makes what they call supply-side forecasts, which do not use this assumption and rely on a DDM much like that used by McKinsey.)

The original Ibbotson method still exerts a strong influence over the brokerage and financial advisory community, where historical returns are widely used as the basis for forecasts. The exact method used by Ibbotson is based on the capital asset pricing model and adds a constant equity risk premium, drawn from history over as long a period as the data allow, to the current cash or bond interest rate. The compound annual equity risk premium over cash, measured over 1926-2014, is 6.6%. The Ibbotson method adds this number to the cash yield, currently 0.3%, to arrive at a stock market total return forecast of 6.9%.[4]

But suppose the high equity returns of the late 20th century were not expected. Suppose that investors expected significantly lower returns, but consistently received positive surprises as the various news items mentioned by DeVoe arrived. If that is the case, it’s not appropriate to use past returns as proxies for investor expectations. Instead, one should try to figure out what returns investors expected at the time, and project those forward when making forecasts. Otherwise they would be incorporating persistently positive surprises into the forecast, a mistake that would bias the forecast upward.

It sounds prohibitively difficult to go back through history and discern what equity returns investors were expecting. However, the Nobel Prize-winning economist Eugene Fama and his perennial co-author Kenneth French have done exactly that.[5] They constructed a DDM and an earnings discount model each year through history (1872-2000), representing the returns that a rational investor would expect given dividend and earnings information and growth forecasts that were available at the time. They then averaged the year-by-year results. Fama and French write:

[T]he dividend growth model and the realized average return produce similar real equity premium estimates for 1872 to 1950, 4.17 percent and 4.40 percent. For the half-century from 1951 to 2000, however, the equity premium estimates from the dividend and earnings growth models, 2.55 percent and 4.32 percent, are far below the estimate from the average return, 7.43 percent. We argue that the dividend and earnings growth estimates of the equity premium for 1951 to 2000 are closer to the true expected value.

In other words, the 1951-2000 period was exceptional. Investors expected a modest return but got a high return. Before that, they got more or less what they expected, but over 1951-2000 they got repeated positive surprises. This did not take place just over the last 30 years, as the McKinsey report suggests, but (1) over a much longer historical period and (2) not in this current century. Since 2000 returns have been less than investors expected.

The McKinsey forecasts, then, are not low forecasts; they are right in line with what investors expected all along. They are also in line with what investors got, except in the unusual 1951-2000 period when returns raced ahead of expectations.

Will investors be happy with a 4% to 6.5% real equity return?

Are the McKinsey forecasts of a real return of 4% to 6.5% in the stock market more or less than what investors are currently expecting?

Let’s look at three methods to estimate what investors on average are expecting: The first is to ask them. The second is to assume that they expect historical returns to be repeated (but historical over what period?). The third is to use a dividend- or earnings-discount model and, like Fama and French, assume that the results of one of those models are a good proxy for investor expectations.

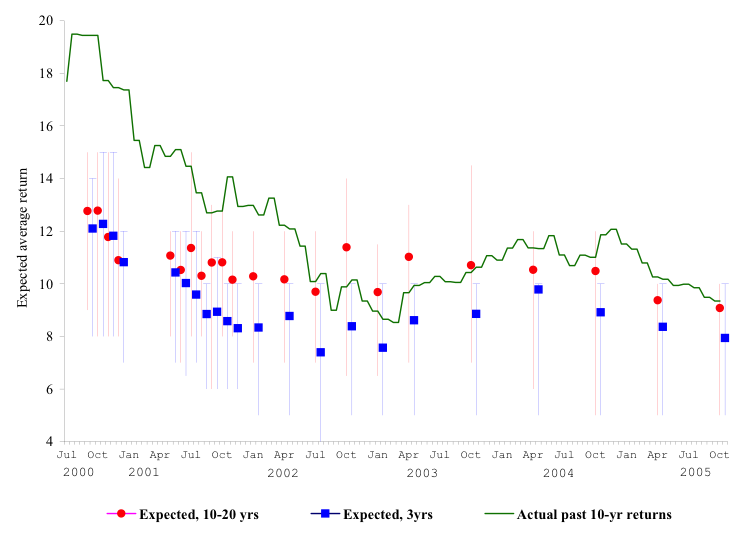

- Ask them. The data are old, but the source – the Federal Reserve – is unimpeachable. A survey of investors reveals that expectations of long-run returns tend to run somewhat below recent experience, but (this is important) with exceptions when recent returns are low. Exhibit 3 shows the survey results from the 2000-2005 period. Since the last 10 years’ nominal annual S&P 500 return is 6.4%, lower than any past return in Exhibit 3, a reasonable guess is that investors expect a future (10 to 20 year) return somewhat above that level.

Exhibit 3

Expected returns vs. past returns: Survey data

Source: Federal Reserve Bank of Chicago, using University of Michigan Survey of Consumer Finances data.[6]

- Use the historical return as the measure of expectations. This method is too dependent on the choice of a time period. Over the last 10 years, the S&P 500 return has been only 6.4% nominal, or 4.6% real; over 1985-2014, the period that the McKinsey report says investors focus on, 8.4% real; over the longest period for which data are usually available, 1926 to the present, 5.9% real. Investor’s expectations based on past performance can be triangulated using these three numbers: about 6%, again in real (inflation-adjusted) terms.

- Use a dividend- or earnings-discount model. My favorite model is, of course, one with my name on it – the Grinold, Kroner and Siegel model that was developed at Barclays Global Investors about a decade ago.[7] It starts out as a standard DDM but has modifications for changes in the number of shares outstanding and for mean reversion from unusual valuation levels; in addition, the growth term is the growth rate of earnings, not dividends. Plugging in recent values for the inputs, we get about a 6% nominal or 4% real total return, including dividends, on the S&P 500.

These three sets of estimates are nicely clustered around 6%, in nominal terms; if one believes inflation will run at 1.5% to 2%, then a real return of 4% to 4.5%. There is no “crazy talk” like the 12%-15% returns that some investors expected, forever, around the turn of the millennium, nor is there an expectation of a long recession or depression. Modest expectations seem to be built into the market, incorporated in the somewhat rich current valuation of equities. (When prices are high, future returns are typically lower, and vice versa.)

McKinsey’s forecasts of 4% real, in the low-growth scenario, to 6.5% real, in the high-growth scenario, then, are on the high side relative to what investors are already expecting. There is nothing out of the ordinary about the McKinsey forecasts, and there is no justification for alarm.

These observations confirm my predisposition to believe that large consulting firms usually repackage conventional wisdom rather than challenging it.

The information non-content of pension discount rates

The McKinsey report expresses concern that public pension funds, purportedly among the most sophisticated investors, are at risk from low future returns because, as it states, “most pension funds are still assuming relatively high future returns of about 7.5% to 7.7% in nominal terms.”

McKinsey is correct to worry about the solvency of public pension plans, but not because they overestimate the returns available from equities. Most pension officers are well aware that their portfolios, about 70% of which are allocated to equities and the rest to low-returning bonds, are unlikely to earn 7.5% in nominal terms if invested in ordinary indexes. They use high return assumptions because their actuaries and consultants advise them that such assumptions will keep current contribution requirements low (because the net present value of future liabilities is lower when discounted at the high return assumption). They then try to earn higher-than-market rates through “alpha strategies” and alternative investments (hedge funds, private equity, venture capital, etc.).

This kick-the-can-down-the-road approach is consistent with rules set by the Government Accounting Standards Board (GASB) and has allowed public pension plan funding to deteriorate to unacceptable levels in many states and localities. Corporate defined benefit pensions, in contrast, use the much more sensible Financial Accounting Standards Board (FASB) rules, which call for a return assumption equal to the yield on Aa-rated corporate bonds.

Thus, there is no information in pension return assumptions suggesting that sophisticated pension officers really expect to earn around 7.5% on equities, much less on diversified portfolios that only partially consist of equities.

Future returns on bonds

If equities do not look so bad from the current vantage point, bonds are a different story. Monetary policies around the world have pushed interest rates to all-time lows, currently about 1.9% on U.S. Treasury bonds with a 10-year maturity. In some countries, shorter-term interest rates are negative.

When one subtracts a reasonable inflation forecast from a yield this low, the real expected return on Treasury bonds is effectively zero. That is, an investment in a Treasury bond portfolio can be expected to just keep even with inflation. TIPS (Treasury inflation-protected securities) do a tiny bit better, with the 10-year TIPS yield at 0.3%.

Investing at a zero real return is better than earning no nominal yield at all, as investors in money market funds and other cash instruments did until recently. But that is about the best one can say about it. Bond yields, which are equal to the expected return, are so low that the current environment has been characterized as one of “financial repression.” In a recent Advisor Perspectives article, Tom Coleman and I express concern that financial repression is depriving the economy of one of its most important sources of potential growth, which is income from savings. As long as policymakers consider zero and negative interest rate policies to be stimulative rather than repressive, I worry that low growth will continue.

A future environment that favors equities

Investors who expect a miracle from the markets – who think that 3% or 5% savings rates will get them close to their goals or that 10% savings rates will assure them a luxurious future – will be disappointed. Those conditions never existed. One would have had to have perfect foresight – and a lot of money early in life – to buy at the bottom in 1982 and then never sell until the top in 2000 or 2007 or 2015, availing oneself of the full glory of the largest bull market in history.

But investors who save diligently, buy and hold diversified portfolios of stocks and bonds and focus on their very long-term goals will do fine. A bias toward equities is justified, given the exceedingly low expected returns on bonds. Even with growth as low as we’ve experienced over the disappointing period since the end of the global financial crisis, the equity risk premium implied by McKinsey’s forecasts is 4%, enough to justify an above-average allocation to equities. With higher growth rates, the equity risk premium implied by McKinsey’s forecasts is even higher: 4.5%.

To quote the redoubtable financial journalist Kate Welling, “be not afraid.”

Larry Siegel is the Gary P. Brinson Director of Research for the CFA Research Foundation and an independent consultant. Prior to that, he was director of research in the investment division of the Ford Foundation. He is a member of the editorial boards of The Journal of Portfolio Management and The Journal of Investing and serves on the board of directors and program committee of the Q Group. He is the winner of the 2016 Graham and Dodd Top Award, shared with Barton Waring.

[1] Although not catastrophic, if my December 10, 2013 Advisor Perspectives article, http://www.advisorperspectives.com/newsletters13/pdfs/A_Framework_for_Understanding_Bond_Portfolio_Performance.pdf, is even remotely right. On average, long-term investors should expect to get back roughly their starting yield, which is just under 2% for the 10-year bond and just under 3% for the 30-year. If inflation stays low, those are unexciting but positive real yields. (See also Leibowitz, Martin L., Anthony Bova, and Stanley Kogelman, 2014, “Long-Term Bond Returns under Duration Targeting,” Financial Analysts Journal [January/February].)

The risk, of course, is that today’s inflation will accelerate – but, over a long enough time horizon, reinvestment of coupons and maturing bonds at higher interest rates will compensate the investor for inflation if markets price bonds to have a sufficiently large inflation-risk premium. The catastrophic real returns of the great bond bear market of 1941-1981 were due the absence of such a premium (the premium was actually negative much of the time).

[2] Source: McKinsey Global Institute, Diminishing Returns: Why Investors May Need To Lower Their Expectations (May 2016), Exhibit 3 on page 6. The letter “” denotes “function.” Notes: 1. Calculated as the product of payout ratio and earnings yield.

2. Acquisitions paid for by shares rather than cash.

3. Includes cross terms. 4. Calculated as 1 – (nominal net income growth ÷ marginal return on equity). 5. Based on weighted average U.S. + non-U.S. GDP growth. 6. Refers to 3-year average at start of period and 3-year average at end of period.

7. Average capital productivity over the past 30 years. 8. 30-year average of total debt divided by the sum of total debt and the book value of equity.

[3] I was Ibbotson Associates’ first employee and worked there from 1979 to 1994. Ibbotson Associates was acquired by Morningstar in 2004.

[4] This forecast is for U.S. large caps (the S&P 500) and is the forecast compound annual return (geometric mean), not the arithmetic mean. The formal Ibbotson forecast method uses only arithmetic means, so what I’ve described is a slight oversimplification. A variation of this method, which Ibbotson has come to prefer in recent years, uses the historical return of stocks over long-term Treasury bonds, instead of cash, and then adds the current yield on the bond.

[5] Fama, Eugene F., and Kenneth R. French. 2002. “The Equity Premium.” Journal of Finance, Vol. 57, no. 2 (April).

[7] Grinold, Richard C., Kenneth F. Kroner, and Laurence B. Siegel. 2011. “A Supply Model of the Equity Premium.” In Hammond, P. Brett, Martin L. Leibowitz, and Laurence B. Siegel, editors, Rethinking the Equity Risk Premium, CFA Institute Research Foundation, Charlottesville, VA., https://www.cfainstitute.org/learning/products/publications/rf/Pages/rf.v2011.n4.6.aspx

Read more articles by Laurence B. Siegel