Sage Advisory Services Ltd. Co., a Registered Investment Advisory firm, was founded in 1996 by Robert G. Smith, III and Mark C. MacQueen. Prior to forming Sage, Bob and Mark both spent many years in distinguished money management careers, working and living around the globe.

Sage Advisory Services Ltd. Co., a Registered Investment Advisory firm, was founded in 1996 by Robert G. Smith, III and Mark C. MacQueen. Prior to forming Sage, Bob and Mark both spent many years in distinguished money management careers, working and living around the globe.

Sage was established with a simple mission: to better meet the unique investment management needs of institutions and individuals through industry-leading analytical services, innovative investment solutions and an unwavering focus on risk management. Sage is headquartered in Austin, Texas, which provides a physical environment consistent with the philosophical vision for Sage – the perfect landscape for independent thinking and purpose-driven investment management. Sage is 100% employee owned and currently manages money on behalf of institutional and private clients across the United States.

Performance information about Sage’s strategies can be found here. Over the last two years, volatility has been on the rise while global equity markets have offered little return. During that time, the Sage Tactical Allocation Strategies have added value relative to the benchmark and delivered strong risk adjusted returns (Sharpe ratio). The example shown is our All Cap Equity Plus Strategy, as well as the Moderate Growth (60/40) which is our most widely used ETF strategy.

I spoke with Bob Smith on June 20.

What led you to create the Sage Advisory, and how has the business evolved since its founding?

I began my career in the early 1970s on Wall Street, first as a bond analyst and then for Loeb Rhodes and Merrill Lynch, on both the equity and the fixed-income side. I worked in the Middle East as an advisor to central bank of Saudi Arabia for about five years, and another five years in London running the fixed-income office at Merrill Lynch.

That was where I met Mark MacQueen. In 1996 we decided to start Sage Advisory, having worked together since the early 1980s. Mark and I have worked together almost 30 years.

We started the firm primarily as a fixed-income shop because everybody else was buying equities in the late 1990s. Nobody wanted to talk fixed income. We were intently motivated by the fact that liability-driven investment management was very prevalent in the insurance business, but it wasn’t very dominant in pension funds and the retail space. We started out as liability-driven investment managers.

The second thing we wanted to do for our clients was to give them things that we thought were tried and true. We were traditional product-oriented with a very traditional process and philosophy that had been time-tested. By doing macro-driven top-down fixed-income actively managed portfolios, we were able to diversify across the yield curve and other dimensions.

What led you to start investing in ETFs?

Starting in the late 1990s, we wanted to do something different in the equity space. At that point in time, ETFs were in the very early stages. It was just SPY, MDY and DIA. We were captivated by the technology. It fit very well with what we did as macro top-down strategists in the equity space, and we felt that many of our decisions could be easily rolled over to other considerations, such as whether to allocate to stocks versus bonds. We weren’t stock pickers. We weren’t industry pickers. We didn’t have a raft of analysts to do that, but we did have some very good macro-decision capabilities that were well-demonstrated.

We started out, believe it or not, using ETFs in some of our balanced accounts that we ran for our institutional clients. We expanded that application progressively as the providers of ETFs grew and the availability of ETFs became greater. We quickly realized there was an opportunity for us to apply our expertise in a more dynamic form. We were also adherents to the works of Brinson, Hood and Beebower and other notable educators and members of the investment-intelligence community that said, from an attribution standpoint, all you have to do is focus on style, cap-size and perhaps some regional orientation. Those are the three big decisions that were driving returns.

Most people were not really applying that knowledge in an aggressive fashion. They certainly applied it, but it wasn’t “the” decision. Investors quickly went on to industries, sectors and stock picking and so forth. We decided we were fine with the big asset-allocation decision and getting the style and the cap decision more right than wrong. That fit well with our fixed income orientation and how we saw the world from a macro top-down perspective. It also fit well with our notion of being really careful with client money, not paying up a lot and getting very little. We found that the expenses associated with ETF investments were quite attractive relative to the mutual fund community. We felt that ETFs were going to continue to grow because of that.

Did you see other advantages in ETFs?

We liked the transparency. We were very well-known early on in fixed income for giving our clients 100% access to everything that we invested for them via the Internet. This was back in 1996-1998. We wanted to follow through with that on the equity side.

Mutual funds and a lot of separate account managers weren’t willing to do that on a day-to-day basis. But this is important because we are stewards of our clients’ money. It’s not our money. As a result of events like the Asian contagion, transparency became important as a commodity or feature to the investment-management process. That was something that drove our process.

Rob Williams, our director of research, joined our firm and helped us to refine further our investment process with regard to ETFs, but we had to wait for providers to catch up with us. We didn’t have all the components of the style box fleshed out. We didn’t have a lot of different choices for each component. We had to wait until we felt that there were appropriate vehicles from an analysis standpoint in terms of tracking errors, trading volumes and what kinds of investors were holding the securities.

The support by the ETF providers was vitally important in terms of the research content and the insight into the construction and maintenance of those ETFs. We don’t buy things just because we think that they are slick and they are interesting. We buy them because they are tried and true and they will be consistent in their ability to give the exposure over and over again that clients were wanting at that point in time.

I understand that you are well known and respected in the institutional and insurance markets. How have you evolved your approach with ETFs for the financial advisor market?

The first thing that is really important for us is that we want to build strategies that would be considered core building blocks. Advisors get pelted all the time with all kind of choices and struggle trying to fit them in and identify what each of these respective choices are regardless of their performance. Very quickly, we said we want to go to the core building blocks of capital market line, provide asset allocation and not be on the fringes.

We don’t want to be fast and furious. We want to be core and somewhat constrained; that doesn’t mean that we don’t generate return, but constrained within our risk set. We wanted to make sure that from a risk perspective, which is where advisors are trying to zero in on their value-add, we are well-defined in a constrained way. We use the basic building blocks and our clients cannot and should not expect us to be 100% invested one day and 0% invested the next day.

We want to have as few moving parts as we possibly can and not have overly complicated portfolios, but have more simplified, straightforward and very clear asset allocations within the portfolios. That makes it much easier for an advisor to describe the investment process, the philosophy we have, where we are invested, what bets we have on and whether those bets are meaningful.

For example, we won’t put anything into our portfolios, at least on the equity side, unless we’ve got a conviction to put 5% or more into that particular category. We compete with many advisors and tacticians that will put 1%, 2% or 3% into a position. By the time you end up adding up the portfolio, you’ve got 40 different positions but it’s hard to identify the theme and the focus of the portfolio.

We have between five and seven holdings in a portfolio. They’ll be thematically going after the same thing as the guy who is running 40 positions, but we are going to do it with a lot more conviction, a lot more concentration, a lot more clarity and a lot less cost and turnover.

By doing that we feel that we are helping the advisor. He can identify us. He knows exactly what to expect from us. He knows how to fit us in within the universe of alternatives he may be considering.

I’d like to ask about your tactical ETF strategies. Can you describe how the portfolios are constructed, which ETFs you use and how you do the allocation among those ETFs?

Within the asset allocation strategy, we are tactical in two ways. The first level of tactical management is at the broad asset-class level, where we will be tactical by moving plus or minus 20% from the equity and fixed income target allocations. For example, our moderate-growth strategy target allocation is 60% equities, 40% fixed income. That strategy can go down to 40% or up to 80% in equities. We believe that the 40% range of motion gives us enough flexibility to protect and be opportunistic without really changing the essential purpose of that strategy.

The second level of tactical management is what we can do within the equity and the fixed-income allocations. We don’t carry any static or neutral allocations in any of the asset classes. We have the ability to exit market segments and sectors entirely. We can make meaningful tactical shifts between asset classes and market segments even within those reasonably constrained and defined allocations.

Most advisors utilize our tactical approach as a diversifier to traditional investment approach and as a risk offset to their equity portfolios. They tend to look at us as a manager who operates with a well identified risk budget or risk profile. We think that’s appropriate.

Among our strategies, we have 100% equity all-cap, core-plus fixed income and blends in between. But all of them are tactically constrained, which means that the strategy operates with a well-defined risk budget.

I understand that your construction process is driven by your views on the macro landscape. What are some of the factors that are key to your decisions on both the equity and fixed income side? I looked at your most recent market commentary, the video that was issued at the end of May, and one of the views that was expressed was that risk markets had stabilized partially in response to the expectation of continued dovish policies from the Fed. What do you see as the primary risks that could disrupt that stability?

We are cautious in an environment where we have had an extended run-up in risk-asset valuations with a relatively mediocre economic backdrop. What do I mean by mediocre? The inability to break out from roughly a 2% to 2.5% trajectory in GDP, relatively low levels of inflation, very choppy employment markets and a very scattered or choppy general economic environment in terms of month-to-month reports from the consumer sector and the business sector.

We acknowledge that there’s also been a high degree of leverage that has been put into the game. Government balance sheets all over the world have become exceedingly more leveraged in terms of debt-to-GDP. There’s also a changing landscape in the corporate arena because corporate credit risk has become much more pronounced than it was a few years ago. Debt-leverage metrics, debt-service coverage ratios, earnings growth trends and top-line revenue growth trends have all either softened greatly or are in decline. In general, corporate credit metrics are going in the wrong direction. There has been a notable change in the degree of leverage on many corporate balance sheets.

In this environment we want to be extremely careful. Since we look at the world from a macro top-down, a fundamental and a technical perspective, we would say that fundamentals right now are not supportive of a continued advance in risk-asset valuations. Technically we are not in the greatest position for another advance in terms of valuations. In this environment, the macro, fundamental and technical factors lining up in a way that is flashing yellow lights. It’s time for people to begin to consider rolling back certain types of risks in their portfolios.

Which risks would you roll back?

On the fixed-income side, it’s rational to start realizing rolling in on the yield curve and taking some of the long-duration risk out of the portfolio, not so much because interest rate policies will tighten and short-term interest rates will go from here to the moon and beyond. But rather, think of fixed income as rent on your money. The income you’re earning is rent. If you are getting no more rent for being in a 20-year than you would over a 10-year note, why be out in a 20-year note and taking on all that principal volatility? Come in on the curve a little bit in this flattening environment.

We also have noticed a huge compression in quality spreads across fixed income including high yield. It’s time for people to reduce the beta in some of those areas. You don’t have to rush at it, but it’s time to start to scale back because of the soft state of the economy and because the continuation of QE is doubtful. We’ve come to the end of the line on QE and other policy actions that would drive rates lower.

From a diversification standpoint, on the equity side we thought that there was going to be a lot of volatility this year, and that was the one commodity that you would be able to buy a lot of. We decided to utilize some smart beta and to reduce the volatility coming out of 2015. Throughout most of this year our portfolios have been tilted towards low volatility, and that has served us very well both in the U.S. and internationally.

On the fixed-income side, during the first quarter we began to exit some of the non-core higher risk sectors of the markets and felt comfortable with establishing a more traditional core portfolio. In this effort we started to move toward higher credit quality and more government credit in our portfolios to liquidity and reduce the price volatility that came from the non-core components. Most of the game was played out during the first three or four months of this year. Once we got through the burst after February 11, when rates bottomed, and went into March and April, we saw that high yield, preferred stocks and convertibles and had more risk than they did before on a relative basis. It was worthwhile to start to scale out of those positions gradually.

You’ve answered a lot of my questions about how you are positioning your fixed-income allocations. I just want to ask more about the equity side. You mentioned earlier that you’ve become more defensive in your thinking. How has does that manifest itself in your equity positioning?

We are trying to protect the downside and mitigate against volatility, and there has been significant amounts of short-run volatility. Our investment outlook is always driven by our investment committee, which meets every couple of weeks at a minimum. We look one to two quarters forward in our forecasts and try to make what we would feel are meaningful tactical adjustments in our portfolios.

This year, we’ve made some very modest adjustments, and have not felt strongly about making big adjustments away from the notion of expecting more volatility than return. What has this led to? Right now in our global equity allocation model, allocations are about 80% low-vol in the U.S. portion and we have a large-cap bias and no allocation to mid or small caps. We have alternated between USMV and SPLV to exercise our view.

We have been underweight emerging markets throughout most of the year. We run against a 10% allocation in our performance index, but we’ve maintained a sizable underweight to this sector with a 5% allocation and we only put that on as we got into the end of the first quarter of this year. Our international allocation had a slight overweight of about 45% of our portfolio and of that we’ve had about 15% in EFA, 10% in VDK (the Vanguard European stock ETF). EAFV, the low-volatility alternative, has represented about 20% of our overall portfolio. So half of our international position has been low-vol. The other half has been full beta with a European orientation.

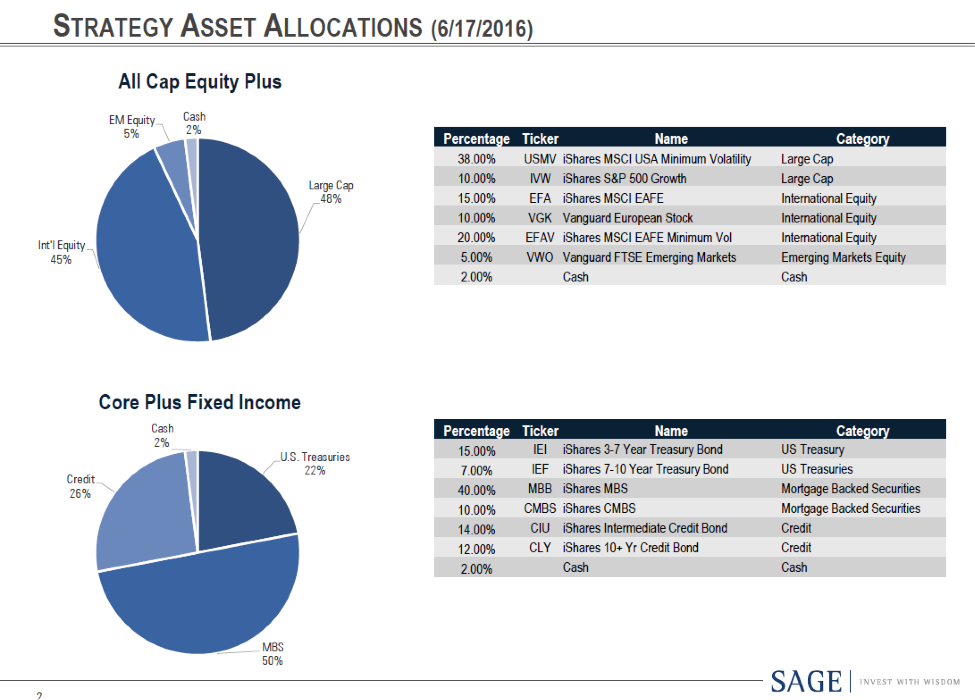

Sage’s allocations can be seen here:

How has the potential for a “Brexit” affected your portfolios?

Over the last several weeks, because of Brexit, it’s been unimaginable and a roller coaster. It is one of those “hold on to your hats” moments.

That kind of whipsaw action, with the volatility we’ve seen, will murder a client’s portfolio. We want to give our clients a smoother ride through the middle of all this volatility and at the end of it, be able to come out and say, “Look, we didn’t have tremendous upside, but we also didn’t suffer tremendous downside. The market offered us almost equal amounts of that in recent months but we have been able to generate consistent performance in our portfolios. We were able to get through some of the travails that people are biting their nails over like Brexit.”

We felt that this approach has been appropriate and it continues to be appropriate going forward. Perhaps on the other side of the Brexit vote we’ll have a bit more clarity and then we will get back to fundamentals being more important. The markets have been driven more by words than deeds. It is the policy initiatives on the part of the central banks that have driven markets, not fundamentals. Things like Brexit and exogenous events are monumental in the eyes of many but have brought more volatility than the actual fundamentals of the underlying economic performance of those markets in those economies.

We had our last investment committee meeting on June 16th. We only made one adjustment to our fixed-income allocation, which was to reduce our mortgage-backed exposure by about 5% and put another 5% into the CMBS portfolio and we left everything else as it was. Last week it was a trail of tears. Today there is nothing but total elation. In the middle of all that there is one word the pops into your mind: volatility. With the volatility that we’ve seen over the last five days, nobody can get it 100% correct: going to cash, coming back out, going back in the cash and so forth. That’s why we are perfect for these environments. We will capture that inner 80% move in the markets and hopefully miss the outer 20% of the upside and, more importantly, the downside moves to allow our clients to sleep a little better at night.

How are advisors using your strategies?

As people sit down and they look at us, they see we are pretty straightforward. Our portfolios are clear in terms of their complexity. They know what they’re getting and they know our thinking. We position the strategy not as a promise to avoid the “big one” or to be the magic silver bullet against risk. We are offering diversification in a traditional setting.

Advisors look at our ETF portfolios and ask why they aren’t more complex. Why are there just five or six positions in the equity portfolio? Why don’t you have 30 positions? We believe fervently that the fewer moving parts there are the less that can go wrong in a portfolio. We like the simplicity. We like the clarity of purpose, the clarity of strategy and the clarity of the strategy decisions.

We like the lower cost. We take a best of-breed approach to ETF selection across the entire market spectrum. We are not wedded to iShares, State Street or Vanguard. We’ll use them all. We do that not just because of cost, but for reasons related to the purpose, design and orientation of the product. Advisors know that we are doing a lot of research on the ETFs we employ within our strategies.

When you look at fixed income and you look at the ETF world, there are literally hundreds upon hundreds of ETFs. However, very few of them can handle the kind of size that we may have to put to work on any given moment because of our more concentrated and determined risk allocation. Most of our strategies are driven from an institutional perspective but offer retail delivery.

Having been around our ETFs since 1998, we have a pretty good reputation for knowing what’s marginal and what is definitely right in the crease. Advisors understand that we’ve done our homework. Many of the ETF providers ask us to look at new ETF portfolios offerings to evaluate and describe what we think our concerns might be. In the end we generally like to stick with the tried and true.

Read more articles by Robert Huebscher

Sage Advisory Services Ltd. Co., a Registered Investment Advisory firm, was founded in 1996 by Robert G. Smith, III and Mark C. MacQueen. Prior to forming Sage, Bob and Mark both spent many years in distinguished money management careers, working and living around the globe.

Sage Advisory Services Ltd. Co., a Registered Investment Advisory firm, was founded in 1996 by Robert G. Smith, III and Mark C. MacQueen. Prior to forming Sage, Bob and Mark both spent many years in distinguished money management careers, working and living around the globe.