In a career spanning more than three decades, Jeffrey Gundlach had never seen the conditions the bond market faced last week. Indeed, he said the “setup for the 10-year Treasury was the worst in his career.”

Gundlach spoke to investors on July 12 to provide updates on two mutual funds, the DoubleLine Core Fixed Income Fund (DBLFX) and the DoubleLine Flexible Income Fund (DFLEX). He is the founder and chief investment officer of Los Angeles-based DoubleLine Capital, known for its fixed-income mutual funds, closed-end funds and ETFs. Copies of his slides are available to download here.

Two elements created the ominous market conditions, according to Gundlach. Yields had moved to new lows, and investor sentiment became exceedingly bullish on bond prices.

His concerns were justified. Since July 5, the yield on the 10-year Treasury has risen 16 basis points, from 1.37% to 1.53%. The previous low yield for the 10-year was 1.39% in July 2012.

The bullish sentiment in the bond market, Gundlach said, was from pundits who were calling for a 1% yield on the 10-year. But the return from that move would be too small to compensate for the risk of an adverse move in yields.

The misguided bond-market sentiment can be found in statements like, “Bond yields simply cannot go up,” and, “Nothing can make them go up.” Gundlach said that sentiment is similar to early this year, when gold was at $1,075 and may claimed it could not go up. But gold went up 30% to its current price of nearly $1,400.

“I don’t like investments where, if you are right,” he said, “you don’t make any money.”

“If you are going to speculate on something, do it where you’ll make some real money,” Gundlach said. Wheat is “down massively,” he said. It may not go up, but if it does you’ll make 10% or 15%, according to Gundlach, which is a better deal than the 10-year Treasury.

Gundlach added that to make money on the 10-year, it would need be sold to “some greater fool at its lowest all-time yield.”

Let’s look at Gundlach’s comments on the economy and the broader bond market.

Banking troubles, the economy and a possible recession

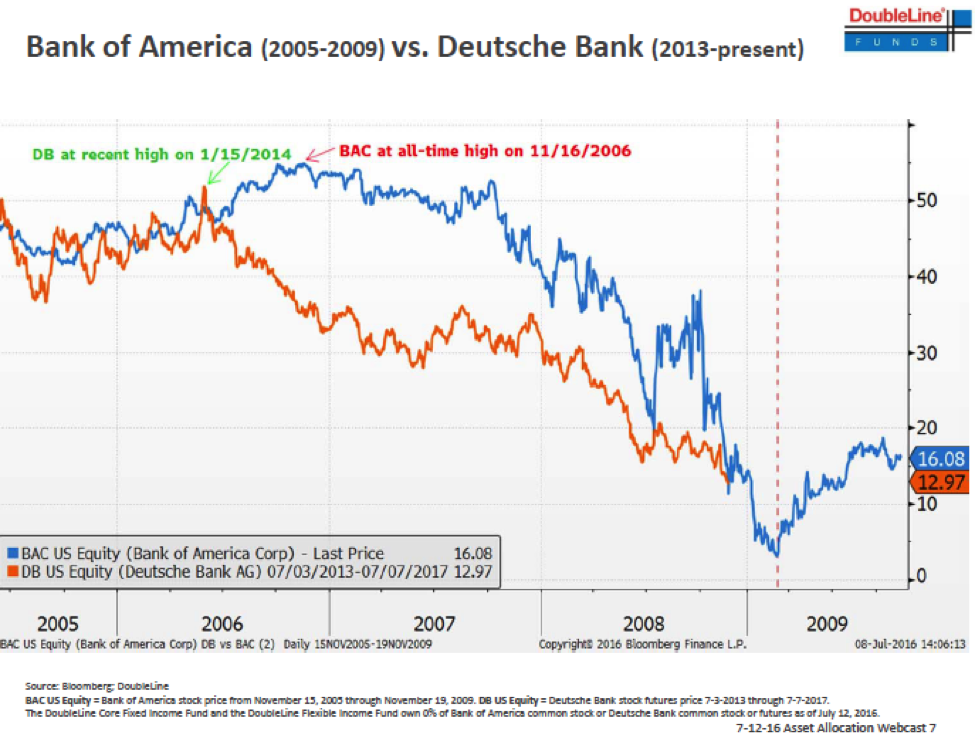

One of the reasons the set up for bonds was so negative, he said, is because of troubles in the banking system. Below is what Gundlach called the “chart of the quarter”:

It compares the price movement of Bank of America’s stock from 2005-2009 to that of Deutsche Bank since 2013. In both cases, there was a slight appreciation followed by a “total collapse,” he said.

Deutsche Bank’s stock closed at $14.10 on the day Gundlach spoke. He predicted that when its price goes to single digits you will see calls for bailouts, and pointed out that this is already happening in Italy and Germany.

The next response to those bank problems will be “bond unfriendly” – deflationary – and will take everyone by surprise, he said. Those responses could include bailouts, “helicopter money” or a large fiscal stimulus, according to Gundlach.

Ironically, Gundlach said that the U.K. – the country that is leaving the EU – has actually been the strongest of the big European equity markets. That is based on the FTSE 100, which is an index of large firms. Those companies have been aided by the collapse of the pound, Gundlach said, and that currency weakness has started to reverse.

As a result of the “Brexit” vote, Gundlach said the probability of a Fed hike is down to zero for 2016, including the July, September and December meetings. There is a probability of one-third of a rate hike for the February 2017 meeting.

The Fed has “completely capitulated” in its plan to raise rates, Gundlach said.

Market indicators are signaling neither inflation nor a recession. Gundlach said the CPI is moving “sideways” at about 1% and the real-time “PriceStat” indicator has been flat.

The Kansas City labor-market indicator is showing no signs of recession, he said. Data from the Atlanta Fed shows that GDP is growing at approximately 2%, Gundlach said, “So we are not in a recession.” The Conference Board Leading Indicator is still above zero and its trend is not good, but according to Gundlach, it is not giving a recessionary signal.

Gundlach follows two unemployment-related metrics that are indicators of a pending recession. The first is when the monthly unemployment rate exceeds its 12-month moving average. That metric has deteriorated recently, he said, and it will cross over in August or September. But he said the second, when the quarterly unemployment rate exceeds its three-year moving average, has been an “uncanny predictive ability of recessions.” It is not forecasting of a recession through 2017.

The commodity price decline late last year has been reversed, he said, due mostly to strength in silver and gold, which is masking some of the other commodity performance. “It is not in a bull market,” he said.

Earnings on the S&P 500 have followed the path of recent years: he said predictions have been “successively and monumentally downgraded.” This year they are headed to zero, he said. Nominal GDP growth is lower than wage and rent growth, which puts deflationary pressure on consumer goods and inhibits economic growth.

Jobs growth has been concentrated in the age-55-and-over crowd, Gundlach said, “many of whom don’t want to work.” Zero interest rates are forcing people to work longer and are reducing spending, according to Gundlach. People need to save more to afford retirement.

Across the bond market

Gundlach offered his assessments of various sectors of the bond market, based on DoubleLine’s proprietary methodologies that indicate valuations relative to the Treasury market:

- Mortgage-back securities are now the cheapest bond sector. GNMAs are 1.5 standard deviations cheap. Commercial mortgage-backed securities (CMBS) are not cheap.

- High-yield bonds are “sort-of okay” from a valuation perspective compared to long-term Treasury bonds. They have done terribly and are very dangerous because of their illiquidity. Defaults on junk bonds are on the rise. The percentage of bonds that are distressed is going down, but in the past that has happened despite bear markets in junk bonds. Recovery rates and EBITDA in the junk bond sector are down, especially on energy companies.

- Crude oil seems trapped between $45 and $50/barrel and is more likely to breakout on the downside because inventories are at record highs and production is increasing.

- Bank loans are a little bit overvalued versus one- to three-year Treasury bonds.

- Municipal bonds were overvalued at year-end and are now at average valuation.

- TIPS are slightly expensive and are “grinding sideways” versus nominal Treasury bonds.

- Emerging-market debt is at average valuation, which is bolstered by the fact that the dollar has not been rallying recently. Do not expect a stronger dollar unless there are economic problems.

Gundlach’s overall theme on the bond market was decidedly negative. He said this is not a good time to enter the bond market, particularly long-dated bonds.

“Be cautious about duration in the bond market,” he said.

“I would not be surprised if the 10-year went to 1.7%,” he said. “That is the base case we are looking at.”

But he added that investors should not bet on very high rates, which won’t be an issue until a few years from now.

Read more articles by Robert Huebscher