The top conversations on APViewpoint last week were started by thought leaders Larry Swedroe, Dan Solin and Michael Edesess, and included comments from thought leader and New York Times columnist Carl Richards. They generated thoughtful discussions on: a common and costly mistake investors and their advisors make; how female advisors should dress to win clients; and why DALBAR is “dead wrong” on investor versus fund performance.

Larry Swedroe’s A Common and Costly Mistake Investors and Their Advisors Make received three comments about his recent article on why investors should not use historical stock and bond returns as the best estimator of their future returns. APViewpoint members discussed the value of considering how historical returns of an investment were earned, and suggested that it can be insightful to examine whether returns were driven by earnings growth or rising valuations. While some maintained that it can be useful to examine long-term stock and bond returns when constructing a retirement portfolio for clients at the beginning of the accumulation phase, others argued that “it's current valuations that predict future market returns, not past returns.” They suggested that advisors look at valuations when examining factors (e.g., value, small-cap), and explained that academic studies have shown that “if spreads narrow between factors, then future returns should be lower.”

Dan Solin’s How Female Advisors Should Dress to Win Clients provoked eight comments from female advisors pushing back against his suggestion – taken from several professional fashion consultants – that they should wear stockings or panty hose and confine their wardrobe to well-tailored skirted suits. APViewpoint members widely agreed that the fashion recommendations presented by Solin don’t align with the common attire of female financial advisors, and that his advice is outdated. Members argued that if they dress too formally they may not seem as approachable, and that wearing more informal clothes such as pants is more practical and provides comfort that helps them feel more confident. They concluded that “as long as you are professional, dress for your setting and your brand, you are fine… being [yourself] and authentic - while professional is the key.”

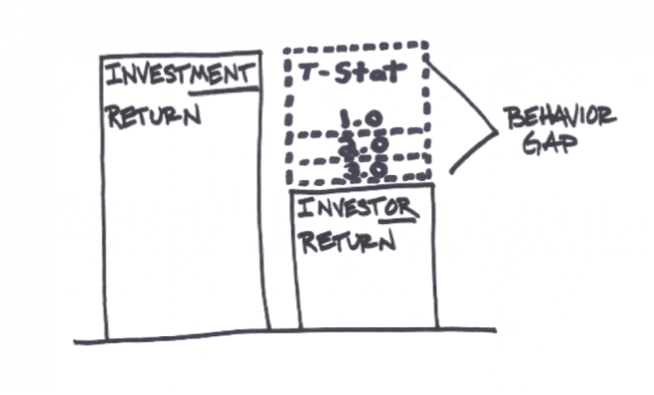

Michael Edesess’ article on The Fallacy behind Investor versus Fund Returns (and why DALBAR is dead wrong) has received 68 comments as it continued into its third week of activity. This week, Carl Richards commented on the conversation about the degree to  which emotionallydriven buyhigh/selllow behavior is taking place in markets. Members continued to debate best practices for measuring the effect of investor behavior on the gap between investment and investor returns. Some argued that, despite the lack of a transparent methodology, the general findings from the DALBAR reports can help advisors fulfill one of their most important goals: helping clients avoid “the big mistake” during market swings. Similarly, they added, simple illustrations like those of Carl Richards can be equally instructive for advisors given that they are “intuitive, truthful, and of great utility (since it makes no claim to precision or quantitative evidence, but strikingly summarize our experience and knowledge-to-date.)” However, others maintained that it would be more insightful to present findings about the effect of behavior on investment returns in an empirical finance framework that uses “t-stats" to specify statistical significance.

which emotionallydriven buyhigh/selllow behavior is taking place in markets. Members continued to debate best practices for measuring the effect of investor behavior on the gap between investment and investor returns. Some argued that, despite the lack of a transparent methodology, the general findings from the DALBAR reports can help advisors fulfill one of their most important goals: helping clients avoid “the big mistake” during market swings. Similarly, they added, simple illustrations like those of Carl Richards can be equally instructive for advisors given that they are “intuitive, truthful, and of great utility (since it makes no claim to precision or quantitative evidence, but strikingly summarize our experience and knowledge-to-date.)” However, others maintained that it would be more insightful to present findings about the effect of behavior on investment returns in an empirical finance framework that uses “t-stats" to specify statistical significance.

APViewpoint will be hosting its next CE eligible webinar, Risk Parity: The Antidote for Unbalanced Portfolios, on Thursday, August 11, at 4:15 PM ET. In this presentation, ReSolve Asset Management CEO Adam Butler will explain why a broadly diversified and properly balanced risk parity portfolio can thrive across a wide variety of market environments. You can register for the upcoming webinar here.

Marianne Brunet is a financial markets analyst with Advisor Perspectives.