DALBAR’s response to this article appears at the end of this article.

Boston-based DALBAR has published updates of its “Quantitative Analysis of Investor Behavior” study annually since 1994. The study is meant to educate investors about how the returns they earn generally lag behind the returns for market indices widely reported in the media. The study analyzes the sources of poor investor performance, finding that the bad timing behavior of buying high and selling low is the main culprit, along with fund expenses, the need for cash and a lack of cash to invest. These are all valid issues. However, my concern is that the quantitative results of the study do not properly measure the underperformance of investors. DALBAR’s method for calculating average investor returns unfairly understates these returns. There is a methodological flaw that I will explain, which is that DALBAR does not properly calculate an internal rate-of-return for an ongoing series of cash flows, which renders its results meaningless.

The DALBAR study is widely relied upon by financial services professionals. Countless advisors and investment companies cite it as an empirical demonstration of poor investor performance. I have even made such references to the study.

Yet, I have only been able to find two authors who have been critical of the study in the past. Harry Sit (The Finance Buff) was the first, and his analysis, provided in a guest post at Michael Kitces’ blog, led me onto the path of finding an even deeper problem with the study. Sit properly demonstrated the point that the market index is based on time-weighted returns (assuming the investment of a lump-sum amount at the start of the period), while investors with ongoing savings and distribution needs will experience a different money-weighted return. With ongoing contributions to investments over time, an investor will underperform the market index if returns tend to be relatively higher in the early part of the investment period when less is invested, and lower in the latter part of the investment period when more funds are invested.

That is a very important point, but it is only part of the story of what the DALBAR study is getting wrong. A key point from Sit’s article that led me on this journey was his reference to how the DALBAR study also shows results for a dollar-cost averaging investor. I’ll come back to this shortly.

The other critical piece I have found about the DALBAR study is an excerpt from the book, The Three Simple Rules of Investing: Why Everything You’ve Heard about Investing is Wrong – And What to Do Instead, by Michael Edesess, Kwok L. Tsui, Carol Fabbri, and George Peacock. That excerpt is posted here at Advisor Perspectives. The authors cited Sit’s analysis (incorrectly attributed to Kitces) about the confusion of money-weighted and time-weighted returns. They also made a new, relevant point about how if mutual fund investors (which includes many professional investors) are underperforming the market so dramatically, then who exactly is on the other side of these trades to outperform by so much? This remains as an unsolved mystery.

Let’s now dig into the problems of the DALBAR study. While the study provides analysis for rolling periods with lengths ranging from 12 months to 30 years, the 20-year investment results serve as the baseline for discussion about the study. The DALBAR study looks at investor returns for equity funds (compared to the S&P 500 as a benchmark), fixed-income funds (compared to Barclays Aggregate Bond Index) and a balanced-asset allocation fund that is not compared to a benchmark. I will base my analysis on the equity funds analysis for 20-year periods, with comparisons to the S&P 500. My analysis of S&P 500 returns is based on data from Morningstar, which leads to slightly different numbers than found in the DALBAR study reports, but this is a minor issue.

Table 1 shows the 20-year annualized returns based on monthly data for different rolling historical periods. For instance, the 2003 numbers represent the period from January 1984 to December 2003. Most recently, the row for 2016 represents January 1997 through December 2016.

Table 1

Twenty-year annualized returns for the periods ending in each listed year

|

Year End

|

S&P 500 Annualized Return (Lump-Sum, Time Weighted)

|

S&P 500 Annualized Return (Dollar-Cost Averaging, Money Weighted)

|

S&P 500 Annualized Return (DALBAR's Methodology for Dollar-Cost Averaging)

|

DALBAR's Reported Average Equity Fund Investor (Using Same DALBAR DCA Method)

|

|

2003

|

12.69%

|

11.35%

|

6.53%

|

3.51%

|

|

2004

|

13.03%

|

11.08%

|

6.36%

|

3.70%

|

|

2005

|

11.94%

|

10.53%

|

6.01%

|

3.90%

|

|

2006

|

11.73%

|

10.61%

|

6.06%

|

4.30%

|

|

2007

|

11.85%

|

10.30%

|

5.87%

|

4.48%

|

|

2008

|

8.37%

|

5.04%

|

2.71%

|

1.87%

|

|

2009

|

8.10%

|

6.15%

|

3.34%

|

3.17%

|

|

2010

|

8.79%

|

6.02%

|

3.27%

|

3.83%

|

|

2011

|

7.76%

|

5.76%

|

3.12%

|

3.49%

|

|

2012

|

8.17%

|

6.20%

|

3.37%

|

4.25%

|

|

2013

|

9.08%

|

7.64%

|

4.22%

|

5.02%

|

|

2014

|

9.86%

|

8.03%

|

4.46%

|

5.19%

|

|

2015

|

8.27%

|

7.39%

|

4.08%

|

4.67%

|

|

2016

|

7.58%

|

7.34%

|

4.05%

|

- coming soon -

|

Source: S&P 500 calculations are by the author using data from Morningstar. DALBAR's Average Equity Fund Investor returns are found in "Quantitative Analysis of Investor Behavior, 2016" DALBAR, Inc. www.dalbar.com

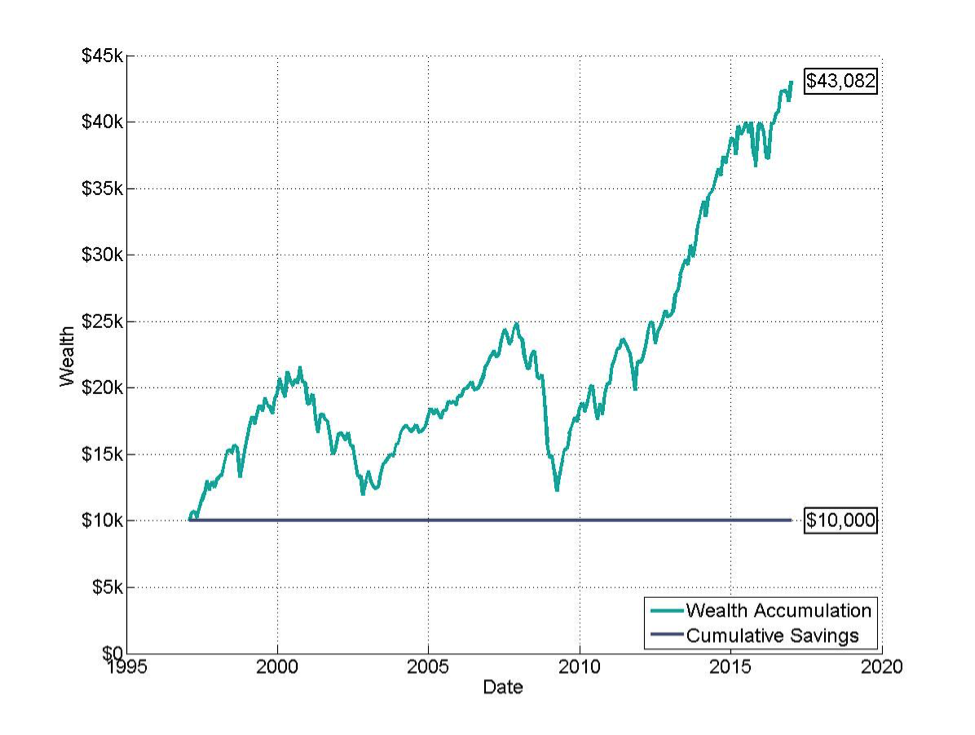

The second column reflects annualized time-weighted returns for the S&P 500. We invest $10,000 at the start of the 20-year period and use the historical monthly S&P 500 returns to determine how much wealth is accumulated at the end of 20 years. This wealth accumulation is used to calculate an annualized annual return over the 20-year period. This is the basic time-weighted return for the S&P 500. Figure 1 provides an example for how this calculation works by using the 20-year period ending in December 2016. A lump-sum contribution of $10,000 made in January 1997 will have grown to $43,082 using the indexed S&P 500 returns.

The monthly return over this period is calculated as:

(43082/10000)^(1/240)-1 = 0.61041%

and the annualized return is (1+0.0061041)^12-1 = 7.58%, matching Table 1.

Figure 1

Growth of a $10,000 S&P 500 investment made in January 1997,

through the End of 2016

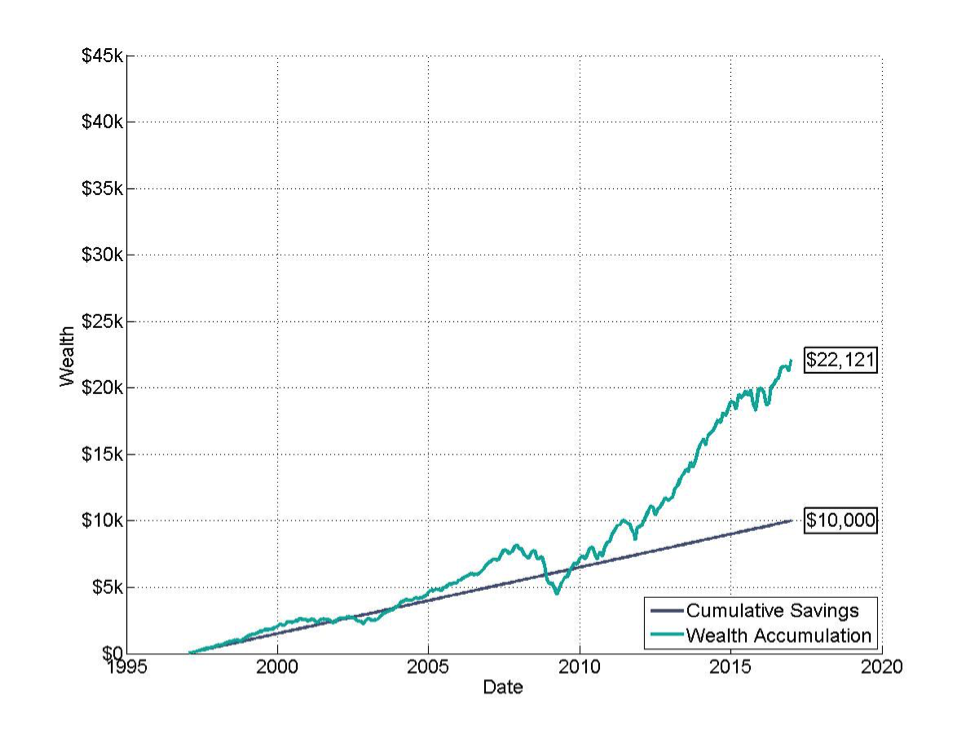

Returning to Table 1, the third column reflects the annualized return over 20 years for an investor who dollar-cost averages in the same $10,000 total investment in 240 monthly increments of $41.67. In this case, ongoing small contributions are added to the investments over time, rather than making the full investment at the beginning. I will use the period ending in 2016 as an example to illustrate this. This case is illustrated in Figure 2, where we can see that the wealth accumulation at the end of 20 years is $22,121. It is naturally less, because contributions were made more gradually over time and experienced less opportunity to grow as the market rose. On average, the contributions were invested for a much shorter period. Based on the wealth accumulation at the end, the annualized investment return for this scenario requires calculating an internal rate-of-return for the ongoing cash flows that accurately reflects when the investments were made.

Figure 2

Growth of a $10,000 S&P 500 investment made as 240 monthly increments of $41.67,

Starting in January 1997 and running through the December 2016

Using Excel, I calculated the monthly investment return for these systematic dollar-cost averaged investments using the RATE function:

=RATE(240,41.67,0,-22121,1) = 0.59224%

I then annualized this as (1+0.0059224)^12-1 = 7.34%, as shown in Table 1. This is the proper way to calculate the money-weighted return for this dollar-cost averaging investment approach. During the time period shown in the table, these money-weighted returns lagged behind the time-weighted returns. This is the point highlighted by Harry Sit. It is a natural implication of the ordering of investment returns over time, and it does not reflect poor behavior on the part of the investor.

Returning to Table 1, the fourth column shows the returns for the same dollar-cost averaging investor using the flawed methodology of the DALBAR study, which is also the same flawed methodology it uses for calculating its average investor returns. We can see that the annualized returns in this column all lag behind the returns found in the previous columns. Returning to the example for the period ending in December 2016, an investor who contributed $41.67 in each of 240 months will have provided a total contribution of $10,000 that is worth $22,121 at the end of the time period. We saw this already.

The DALBAR methodology ignores dollar-cost averaging component of these systematic investments and instead assumes that the entire $10,000 was invested at the beginning of 1997. This is because it uses the same methodology for calculating a time-weighted return, rather than using a proper money-weighted return.

Using DALBAR’s approach, the monthly return over this period is calculated as:

(22121/10000)^(1/240)-1 = 0.33136%

and the annualized return is (1+0.0033136)^12-1 = 4.05%, as shown in Table 1.

I hope it is clear why this calculation is wrong. If the $10,000 was invested at the beginning, it grew to $43,082. But because the investment was gradually made over time with ongoing new contributions, it could only grow to $22,121. Because the money is not invested for as long, on average, the accumulated wealth should be lower. But it doesn't mean that an investor underperformed by making bad decisions. The investor did not have the resources to be invested yet. This dollar-cost averaging case is a better benchmark to determine real-world investor performance and whether investors mistime the market. DALBAR creates an unfair penalty by assuming these funds were all invested at the beginning of the time period.

This is very important because it is the same way it calculates the return for the average equity-fund investor. It incorrectly calculates too low a return for reasons completely unrelated to investor behavior.

Investors may underperform, but the DALBAR study and its calculations cannot determine this.

Returning to Table 1, I can’t replicate the specific DALBAR calculations for average equity-fund investor performance, because I do not have access to the inflows and outflows of funds to know what the wealth accumulation would be at the end of each 20-year period. The fifth column reports the numbers from the DALBAR study. The section on “Systematic Investing” from its 2016 report revealed that this is the methodology used. It describes findings for the 20-year period ending in 2015 (the 2017 study providing returns through 2016 has not been released yet).

In its 2016 report, the S&P 500 earned 8.19%, the average equity-fund investor earned 4.67% (final wealth is $24,894), and the systematic dollar-cost averaging investor earned 3.99% (final wealth is $21,184). This flummoxed the DALBAR authors, forcing them to use contorted logic to explain why the systematic investor actually underperformed the average equity fund investor. The authors point out that the average investor was able to get more into the market in the late 1990s, which set them up for the win as the S&P 500 surged at that time.

This explanation reveals DALBAR’s understanding that having more invested early is advantageous, making it all the more troubling that it continues to make the calculations in the manner done. We are able to learn from this section about its incorrect method to calculate these money-weighted returns. It does the wrong time-weighted calculations for average investor returns as well. Because these investors gradually enter the markets, they naturally lag behind a lump-sum investment into the S&P 500 for reasons completely unrelated to poor investor behavior. Calculating internal rates of return would correct for this. The dollar-cost averaging investor should be DALBAR’s benchmark for comparison, not the lump-sum investor.

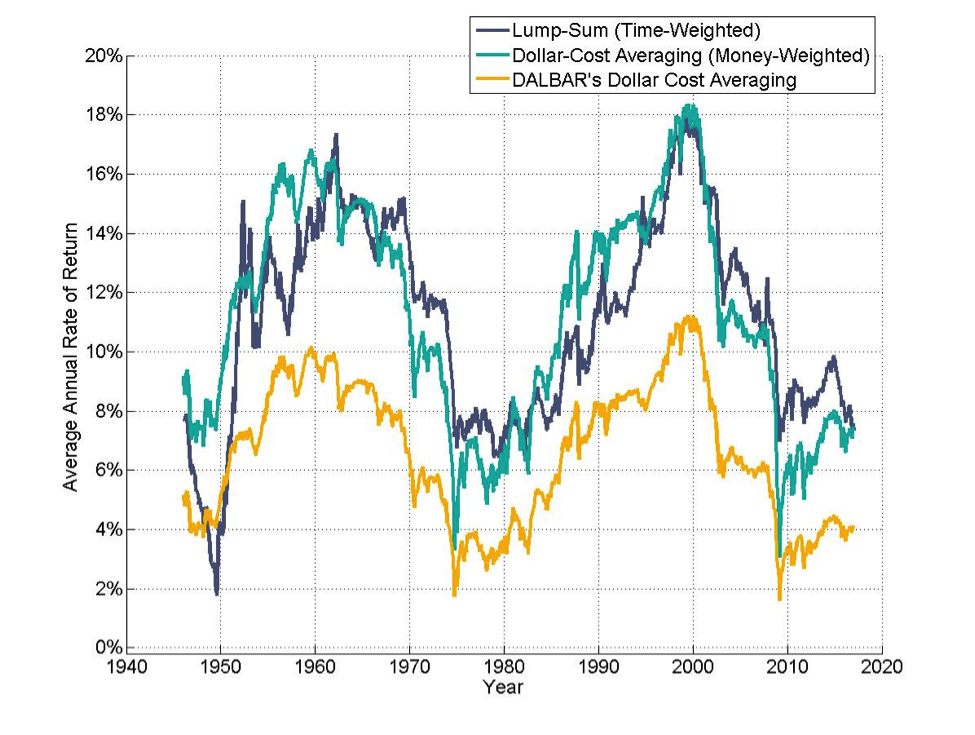

I conclude with Figure 3, which shows the rolling annualized returns for 20-year periods ending between December 1945 and December 2016. The lump-sum (time-weighted) returns reflect the annualized returns for the S&P 500 for these different periods. The dollar-cost averaging (money weighted) returns reflect the correct way to calculate the internal rate-of-return for ongoing systematic investments. This allows us to see Harry Sit’s point that sometimes money-weighted returns are ahead and sometimes they are behind. Though they have lagged behind time-weighted returns in the current century, there were various points in the past that these returns were ahead. It depends on the ordering of good and bad returns during each rolling historical period.

Finally, the yellow line reflects DALBAR’s incorrect way of calculating the returns from systematic investing. These returns lag behind dramatically for much of the historical period. But this reflects bad calculations and is completely unrelated to bad investor behavior. In terms of the average equity-fund investor return calculated by DALBAR, I do not have the data to recreate these, but Table 1 shows that sometimes these will be ahead of the yellow line and sometimes they will fall behind the yellow line. Because of the biased calculation, they will almost always look worse than the correctly calculated outcomes.

Figure 3

Rolling annualized returns over 20 years

for a lump-sum investment, dollar-cost averaging, and DALBAR’s incorrect way to calculate returns for dollar-cost averaging

The bottom line

Investors may behave badly. But the DALBAR study does not demonstrate this empirically. Its calculations are wrong and the financial services profession should stop using it as a way to market the value of financial advice.

Not all is lost, though, as there are other more sound ways to show the value of good financial advice and the harm from making bad investment decisions. Morningstar’s Gamma measure and Vanguard’s Advisor Alpha are two great ways to do this.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management and the Chief Planning Scientist for inStream Solutions. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Advisor Perspectives sent an earlier draft of this article to DALBAR for its comment. DALBAR’s response, from its CEO, Louis Harvey, is below, after which Wade Pfau revised the first paragraph and the concluding two paragraphs. The revised version was sent to DALBAR and Harvey added a postscript to his response below.

March 1, 2017

Robert Huebscher

CEO

Advisor Perspectives

Box 380

Lexington, MA 02420

Re. Feedback on article we plan to publish

Dear Mr. Huebscher

Thank you for sharing the article, “Is It Time to Toss the DALBAR Study in the Trash?” for our comment. As you might imagine, our view of the work is that it contains factually incorrect statements and assumptions that lead to grossly incorrect conclusions. One need only to read the first paragraph to recognize that the article’s entire premise is false.

Several quotes from the first paragraph are presented below to illustrate these errors.

“The study is meant to serve as a marketing tool for financial advisors…”

- The assertion that the study is meant to serve as a tool for financial advisors is patently false. The study was developed to quantify the widely held view by investors that the returns they received were different from what was publicly reported. It has served to educate investors, advisors, financial institutions, academics, courts of law and various branches of the government of the magnitude of this difference. See http://www.dalbar.com/QAIB/Index.

“…to convince clients and prospects that they will earn significantly higher investment returns through professional management of their portfolios.”

- There is no basis for assigning this purpose. At no point has this study stated or implied that the difference in returns had anything to do with professional management. The study has given voice to practices that can serve to reduce portfolio underperformance. These practices are presented as methods investors can deploy and do not suggest the use of professional management. Practices include education, asset allocation, risk tolerance assessment, capital preservation strategies and altering of instinctive behaviors.

“The study blames poor investor performance mainly on bad timing behavior of buying high and selling low, with other culprits including fund expenses, the need for cash, and a lack of cash to invest. However, their study absolutely fails to demonstrate this!”

- The study does illustrate the recurring practice of “buying high and selling low” by reporting the juxtaposition of monthly market movements and cash flows into and out of investments. This data makes it obvious that inflows (buying) occur most often after a market rise and outflows (selling) occur most often after a downturn.

- Questioning that fund expenses lowers investor returns or that this is a DALBAR invention is ludicrous on its face.

- The other two, the need for cash, and a lack of cash to invest, are equally ridiculous challenges. Does the author seriously expect DALBAR to prove that investors don’t earn market returns when they are out of the market?

“Investors may underperform market indices. But whether this happens is not something that the DALBAR study is able to test.”

- This is simply unparalleled arrogance. The author is in no position to know what DALBAR can or cannot do.

“There is a basic methodological flaw that I will explain, which is that they do not seem to know how to properly calculate an internal rate of return, which leaves there results as completely meaningless.”

- The assumption that an internal rate of return calculation is the means and the only means to determining the performance difference is itself flawed. For the education of the author, certain measurements of fund performance use IRR but the study in question calculates the effect of activity and IRR is neither necessary nor relevant. The article would be well served if the author read the methodology that is actually used in the study (Return = Change in assets, net of inflows - outflows).

- The conclusion that the results of such a calculation is meaningless is for the reader to decide.

Thank you for the opportunity to respond to this work.

Louis S Harvey

President and CEO

PS

March 2, 2017

Thank you for the rewrite of the first paragraph of the article in response to my comments above.

While these changes address a number of the issues raised about the first paragraph, the more fundamental failure to understand the study’s methodology remains. This failure permeates the entire article.

It is utter impudence for your author to take the position that the only valid methodology is that which he espouses. While I don’t have the time or inclination to argue each assertion made, it is clear that the article is written from the perspective of the investment while QAIB takes an investor perspective.

Our formula determines what investors recognize as returns, not what the investments produce. This difference put in its simplest terms can be reduced to opportunity cost, and the resulting regrets. Opportunity costs do not exist from the perspective of the investment but it is a very real part of the investor’s world. This is the reason for using the term, “Investor Return” to describe the results.

If your author is convinced about the methods he considers valid, he should conduct his own study and let the public decide.

Read more articles by Wade D. Pfau