Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article is in response to Kerry Pechter’s article, The Ambiguity of Tax Deferral, which appeared on December 4, 2017 and the SSRN paper it referenced. In contrast to the idea that there are different, but valid, ways to look at traditional tax-deferred 401(k) and IRA accounts, I show that there are right and wrong conceptual models. Wrong models lead to wrong decisions and do not explain outcomes. When evaluating the government’s costs for these accounts, it must be acknowledged that the benefits to savers are different from the costs to taxpayers.

The correct conceptual model

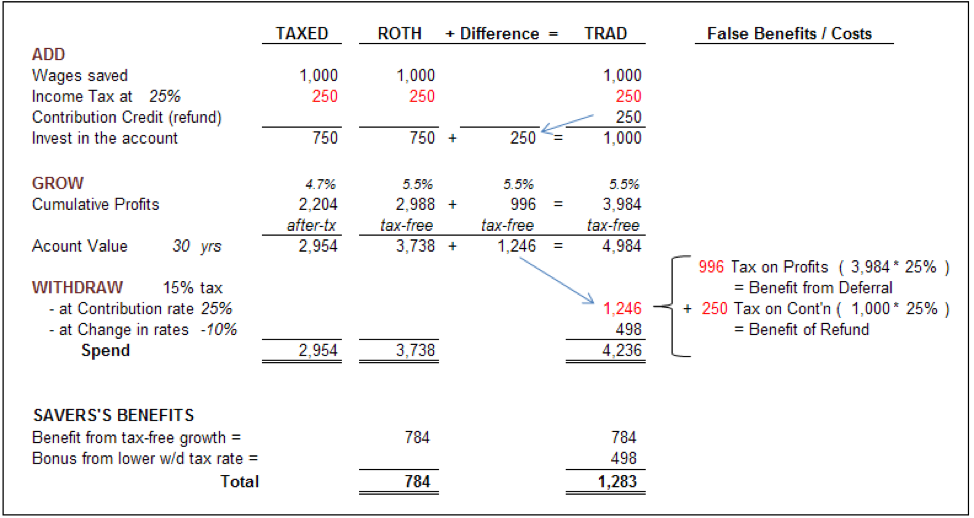

The scientific method requires that a model explain and correctly predict outcomes. Since the purpose of a tax shelter is to reduce income taxes, the model must explain and predict the value of taxes saved. A proxy for taxes saved is the excess ending wealth versus a normal taxable account. The model shown below does that. It uses one set of variables but holds true for all assumptions.

The taxed, Roth and traditional accounts are compared side-by-side, with a difference column reconciling the traditional account to the more easily understood Roth account. The difference column tracks the government’s partial funding and ownership of the account. This model holds true regardless of actual cash flows. The original $250 tax reduction at contribution is considered to be invested alongside the saver’s after-tax savings. Its resulting value fully funds the $1,246 withdrawal tax (calculated at the same rate as at contribution).

The benefit from a Roth account is its permanent sheltering of profits from tax. The traditional account gives all savers an exactly equal $784 benefit from the same factor The withdrawal tax is an allocation of principal between the account’s two funders/owners, not a tax on profits as commonly claimed.

What the common conceptual model presents as a 'tax on profits' ($996 at withdrawal) will always be exactly equal and offset what is claimed to be a ‘benefit from deferral’ (the profits earned by the unpaid $250 tax in the interim). The $250 tax reduction at contribution is not a benefit in itself because it is repaid on withdrawal. These factors always zero out in total, and never impact the account’s net benefit.

The only factor impacting the traditional account’s net benefit, on which everyone agrees, is the difference in tax rates between contribution and withdrawal. Even when the $498 bonus becomes a penalty if the withdrawal tax rate is higher (not lower), the benefit from profit-sheltering is usually far larger, leaving a net benefit relative to a taxed account.

Wrong choices are made when based on false models, e.g.:

- Those who believe the tax reduction on contribution is a benefit will likely spend the cash on extra consumption. They will think that a $1,000 contribution to a Roth account is a comparable choice to contributing $1,000 to a traditional account. When constrained by contribution limits they won’t appreciate that using a Roth account will shelter more of their profits than a traditional account.

- Those who believe that profits are taxed on withdrawal will locate profits that are normally preferentially taxed in a taxable account to avoid full taxation in traditional accounts.

- Those who fail to appreciate the compounding benefit of permanently sheltering profits from tax will asset-locate based on a ”tax efficiency” metric that measures taxes in year one only. They may withdraw funds early in retirement based on optimizing only the withdrawal tax rate.

- Those who believe there is a benefit from deferral of taxes may delay withdrawals in retirement based on the belief that they are maximizing the benefit from deferral.

- Those who fail to understand that the withdrawal taxes are an allocation of principal between the account’s two owners will use the full account value in asset-allocation calculations, resulting in a too-small weighting for the assets in the traditional account.

These examples of wrong advice, resulting from wrong conceptual models, are found throughout the advice industry.

The government’s cost

In my research paper, Government’s Cost for Retirement Accounts, published on September 27, 2017, I switched the point of view to that of the government, and broke down the net cost for taxpayers. I showed that for traditional accounts there are three factors that add together. The government is modeled as borrowing to replace any income tax not collected.

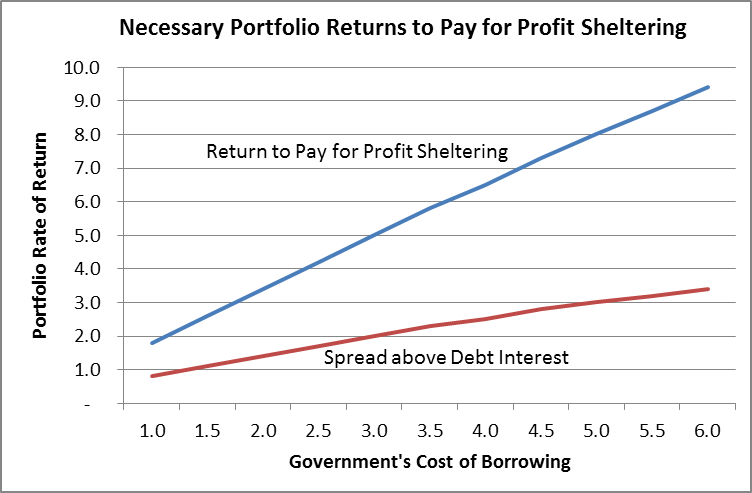

- The cost to government for tax-sheltered profits is less than the benefit to a saver for that same factor. This is because the saver’s benefit compounds over time at the rate of return earned by his portfolio, while the government’s cost compounds at the much smaller interest rate of its debt.

- Taxing withdrawals at rates lower (or higher) than at contribution costs the government the same as the bonus (or penalty) for savers.

- The third factor for the government is a benefit from leveraged investing. The government borrows $250 to fund the income tax not collected at contribution. That debt compounds over time at the low interest rate on government debt (say 3%) ending at $607. But inside the traditional account, the saver is investing the $250, on the government’s behalf, at the higher 5.5% portfolio return to collect the $1,246 withdrawal tax. The government is essentially investing with leverage, borrowing at low rates, investing to earn high returns, and pocketing the $639 difference.

In the process of borrowing to invest in risky assets, the government faces costs to administer its debt and the saver may pay advisory fees that are buried in her (and the government’s) 5.5% portfolio returns. But are those fees a justification for calling traditional accounts inefficient? Are they a reason to impose regulation of fees? Should the accounts be denigrated by calling them a government subsidy to the private asset management industry? Is there justification for concluding that back-loaded taxation (traditional accounts) are more expensive for the government (than Roth accounts)?

No. Even with advisory fees reducing the saver’s portfolio return, the government benefits from the leveraged investing inside traditional accounts under most reasonable assumptions. Certainly at today’s low interest rates the necessary spread to earn a leveraged return large enough to completely offset the cost of tax-free profits is very small. Advisory fees will reduce returns and the benefit from leverage, but not destroy it.

Conclusion

The only conceptual model that explains and correctly predicts the resulting benefits from traditional retirement accounts is the model that sees the government funding and owning a portion of the account. The withdrawal taxes are an allocation of principal between the two owners.

The reality that most savers misunderstand the traditional account and think the whole account is ”their money” is a poor reflection on the financial advice industry and media. Savers have been taught wrongly. The government itself promotes the false ideas that profits are taxed on withdrawal and that the tax reduction on contribution is a benefit. It gives no hint that the main benefit is from permanently sheltering profits from tax, always exactly equal to the same benefit from a Roth account.

The cost to government for traditional accounts is the sum of three factors. If their benefit from leverage is greater than the cost of withdrawals at lower tax rates, then they cost less than Roth accounts, and vice versa. Any advisory fees for managing the government’s share of the investment portfolio are a small price to pay for a larger benefit from leveraging.

Chris Reed is not affiliated with any investment firm. He maintains the web site www.retailinvestor.org.

Read more articles by Chris Reed