Why Referrals are Down – and What to Do About It

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In my article, Why Top Performing Advisors are Exiting the Business, I outlined the fundamental changes taking place in every aspect of how financial advisors operate. Perhaps nowhere is the change we’re seeing greater than in how successful advisors are attracting new clients – and in particular the collapse in the role that referrals play in bringing new clients on board.

Historically, referrals were the primary way that advisors attracted new clients. And those referrals came relatively easily, as a reward for doing a good job for clients. But times have changed. When I talk to advisors today, I hear a different story, as many talk about referrals “drying up.” And industry data backs this up.

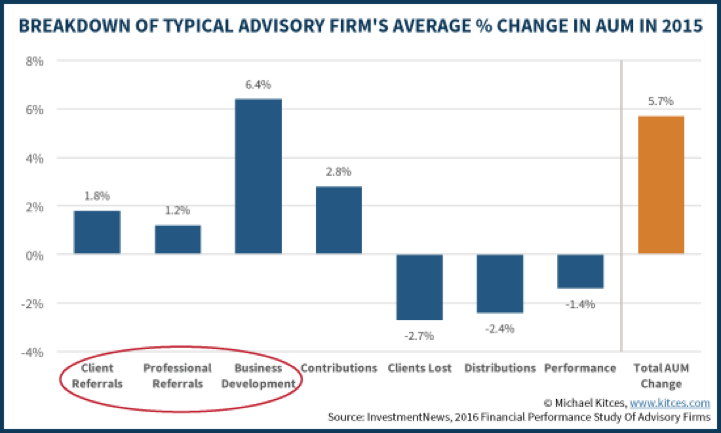

In his article, The Death of Referral Marketing for Financial Advisors, Michael Kitces wrote about a FPA research study on the source of AUM growth. The key chart is below, showing that in 2015 client referrals represented less than 2% of AUM and when it came to increasing assets were significantly less important than the combined assets from a variety of other business development techniques.

This raises three fundamental questions for advisors:

- What’s led to the slump in referrals – and is this change temporary or permanent?

- What are the implications for the approach that you should take in your approach to referrals?

- What does this mean in terms of the broader strategy on attracting clients?

Today, I’ll tackle the first two questions on referrals – and deal with the issue of your broader strategy on attracting clients in the New Year.

Why referrals are down

There are several reasons that referrals have dropped from historic levels.

- The risk of referring friends

Some clients are still scarred by the near-death experience of 2008. In one roundtable with investors that I hosted recently, several said that while they liked and trusted their advisors, they would be cautious about referring friends. The reason came down to the responsibility that would come with making those introductions and the risk of jeopardizing friendships should we see another sharp drop in markets. Added to this is that some clients who referred friends and family to advisors in the past reported that they felt pressured to meet; even if that was a different advisor, that memory may still make some clients cautious.

- Lack of differentiation between advisors

Even if clients are happy with the job you do and your relationship, that isn’t always enough to lead to an enthusiastic referral. One reason for that is that many advisors are perceived to operate very similarly, using words to describe how they operate that are indistinguishable from other advisors. This is no different than recommending your accountant or lawyer to a friend. Even if you’re happy with your accountant, if you feel that the job he or she does for you is fundamentally no different than what other accountants would perform, you’re less likely to provide an enthusiastic referral.

- Fewer investors are actively looking to move

Finally, there is the reality that most investors with significant assets are either working with an advisor today or have worked with one in the past before deciding to manage their money on their own. As a result, there are fewer investors who are actively looking to move. We also have to add the impact of buoyant markets. I recently talked to an advisor who said that given strong markets since 2009, prospects are reluctant to change what they’re doing– but that when we hit an inevitable correction, a flood of investors will be looking to move. Of course, that depends on the nature of the correction – a sharp pullback may cause investors to pull out of the market entirely, similar to what we saw from some clients in 2008.

Given the reality of these obstacles to referrals, there are three keys to increasing referrals:

1. Reduce clients’ perceived risk of providing referrals

2. Recognize the role of “referral DNA” among your clients

3. Adopt the right mindset on referral conversations

Reduce clients’ perceived risk of making referrals

Most advisors instinctively recognize the importance of reducing the risk for clients in making referrals. That’s one reason that some self-styled referral experts urge advisors to get clients to talk about the value that you provide.

There are two problems with asking clients to describe the value that you provide. The first is that, quite frankly, it’s a bit weird and risks having clients see you like someone selling used cars rather than as a professional. Honestly, can you see a successful accountant or lawyer saying to a client: “Before we go further, can you tell me all the ways that I’ve created value in our relationship?”

But there’s a second, more fundamental issue: For clients to talk about the distinct and unique value that you provide, you first have to provide distinct and unique value. In my article, Your #1 Imperative: Differentiate or Die, I talked about the imperative to narrowly focus the clients you work with and the problems that you solve for them. By transitioning your business to become the safe choice for the clients you serve, you reduce the risk for clients to provide referrals to other members of your target community.

Remember, clients don’t make referrals to help their advisors, they make them to help their friends. Among the many approaches that advisors have used to become the safe choice for target clients:

- Some advisors target people approaching retirement who work for large employers in their community, based on an in-depth understanding the ins and outs of the company’s benefit and retirement plan. One advisor got so good at this that the HR department at her town’s major employer hired her to run half-day workshops for employees.

- Some advisors have built expertise working with charities to deliver talks on charitable giving to their key supporters. In this case, charities hire the advisors to put these sessions on – although in some cases the attendees are so impressed by the advisors that they approach them about working together.

- Many successful advisors have focused in on a subset of business owners in their community who have common needs. One advisor focuses on owners of automobile dealerships; among other tools, to address a key risk for these auto dealers he developed a proprietary portfolio that underweights consumer cyclicals and auto stocks. Another advisor concentrates on owners of mid-sized businesses and hosts twice-annual breakfast sessions, to which he brings outside speakers on hot button topics such as best practices for hiring online, how to increase employee retention and ways to reduce the risk of employee litigation.

These are just a few examples – some advisors have developed a specialty working with women getting divorced and others have carved out a niche working with business owners who are selling their companies. As a general rule, the more important the life event for clients, the more likely they are to seek out a specialist.

One misconception that prevents advisors for embarking on a focused strategy is the fallacy that this means abandoning your existing clients. In truth, almost every advisor who has shifted to a focused approach has done so incrementally, continuing to serve existing clients while simultaneously reorienting their practice to pursue a focused client group.

To get started, carve out two half-days a week to do the fact-finding on potential groups and then to start building the expertise required to serve the group you choose. My article, How Specialist Advisors Earn Twice as Much, discussed the mechanics of picking the right group and ensuring you have the expertise and capability to serve them.

Once you’re in a position to address your target group’s unique needs and hot buttons, shift all your marketing efforts to concentrate on the group you’ve selected. Another of my articles, Becoming the Safe Choice for Your Target Clients, discussed the steps to build credibility and generate clients within a defined-target group.

Finally, within the bounds of client confidentiality, keep clients who make referrals in the loop on what has happened as a result. One advisor implements a 90-day welcome process for all new clients during which he dramatically ramps up the level of contact. At the end of that, he meets with new clients to get their feedback and asks them to complete a short five-question survey on their satisfaction to date. The feedback is inevitably positive. For clients who have been referred, he asks for their permission to share it with the clients who introduced them, keeping referrals top of mind and reducing the risk of future referrals.

Target the right clients

When you read advice on referrals, there’s lots about the advisor’s role in making referrals happen. What is seldom mentioned is the role that the client’s mindset plays in making referrals happen. But my article, New Research: The Unexpected Variable that Leads to Referrals, described a 2012 research study that shed important light on how different clients respond to the same conversation.

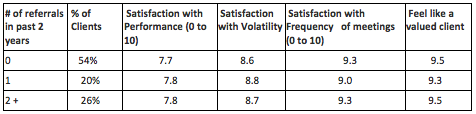

This research study gathered in-depth information from 500 clients. When asked how many times they’d introduced their advisor to friends or family in the past two years, for just over half the answer was none, while one in five the answer was once and a quarter had made two or more introductions.

The first thought was that the advisor may have played a role, but when probed as to whether their advisor had brought this up, 19% of those who hadn’t made introductions said that their advisor had mentioned this versus 22% among those who’d provided multiple introductions.

The next thesis was that clients who provided referrals were more satisfied with their advisor’s performance, but again there were no meaningful differences among clients who’d made multiple referrals versus those who hadn’t. You can see the results of that analysis below:

So if asking for referrals and satisfied clients aren’t connected with more referrals, what is? Fortunately, we had asked one other question that ultimately provided the answer. We asked the clients who completed the surveys whether they’d made referrals to other professionals over the past two years, such as accountants, lawyers, bankers, doctors and dentists. Here’s what we found:

There are at least two implications to this research.

First you need to give referrals greater importance in identifying your most valuable clients. Clearly, referrals are your most important form of non-financial compensation from a relationship. When you segment clients in terms of the communication they’ll receive, ensure that you give high-referral DNA clients who provide referrals the recognition that they deserve. My article, Three Steps to Dramatically Happier Clients, outlined some new thinking on how to treat your best clients differently.

Second, make referral recognition a priority. I recall talking to a client who’d referred a family member but was annoyed that she hadn’t gotten so much as a thank you from her advisor.

Most advisors acknowledge referrals, but the advisors with the most success at referrals go beyond this. These advisors put special effort into having a clear process to recognize and thank clients who recommend their friends. Some advisors send a bottle of wine or gift basket with a thank you note or make a donation to their favorite charity. One advisor takes those who made an introduction and the clients who they referred out to a nice dinner. Other advisors organize intimate dinners and other special events to thank all the clients who’ve made introductions. But whatever approach to thanking clients who provide referrals works for you, ensure that you have a clear consistent strategy in place.

Adopt the right mindset on referral conversations

Conventional wisdom is that to maximize referrals, advisors need to talk about this subject with clients. Most advisors long ago moved past the pressure-based approaches of the 1970s and 1980s (with stock lines like Who among the people you know should I talk to, who I can help in the same way I’ve helped you?) That being said, there is a cottage industry of referral coaches who expound the view that to maximize referrals, you need to have clear conversations about your value and about the benefits that clients have experienced in working with you.

But a 2008 research study sponsored by Vanguard called into question the impact of talking to clients about referrals. That study polled clients who had provided referrals and asked about the catalyst for the referrals. The surprising finding: Only 6% of referrals were triggered by a conversation with an advisor.

Conversations that you initiate around referrals are much less important than a reading of our industry’s “referral literature” would have us believe. Yes, it does make sense to periodically remind clients that you’re open for business and would be happy to talk to their friends. And given that an FPA research study showed that three quarters of new clients didn’t previously have an advisor, it might make particular sense to let clients know that should someone they know be managing money on their own, you’d be happy to talk to them.

But once you’ve raised this a couple of times, don’t make these conversations a source of anxiety for you or your clients. In particular, use your existing client communication as a low-stress way to raise your awareness among people in your clients’ networks.

Want to Shake Up Your Next Conference?

“A Bridge to the Future”

"Dan's talk created a sense of urgency to act and gave our advisors a roadmap to bridge the gap and move forward."

Frank Laferriere, SVP and COO, Portland Investment Counsel

Dan Richards delivers talks that challenge the status quo and inspire action. But he does more than issue a call to change … he provides new thinking and fresh strategies to help advisors navigate the future.

Click here for short highlights from a recent presentation

"Well thought out and insightful"

“A well thought out and insightful presentation to our Chairman’s Club qualifiers ….great response to your single-minded focus on what it takes to bring new clients on board.”

Lorne Harper, EVP and National Sales Director, HSBC Securities

To energize your next conference, click for more information on Dan’s speaking topics and to hear from past clients … or contact Dan at [email protected]

“Top Marks”

“You got the top marks of any speaker at our Presidents Club conference … great job”

Scott Yeoman, Training Manager, RBC Dain Rausche

One advisor had good success by sending clients an email each Friday afternoon titled “Your Weekend Reading and Viewing.” He sent links to one article and one video he’d found helpful or had enjoyed. The articles tended to be more serious and focused on financial issues, the videos more lighthearted or thought provoking.

He got especially good feedback on some of the upbeat videos that he shared. After a while, this weekly email became a vehicle for clients to introduce him to their friends in a way that was comfortable for both his clients and their friends. By sharing this email, his clients were implicitly recommending him to their network – and over time this advisor began getting calls from prospects who’d been getting his emails. Indirectly, what started out as a vehicle to stay top-of-mind with clients had become a way to get low-key introductions to his clients’ networks.

This is part of a series of articles on the imperative changes for advisors to thrive in the period ahead.

Why Top Performing Advisors are Exiting the Business makes the overall case for fundamental change

Your #1 Imperative: Differentiate or Die talks about the need to focus your client base.

Three Steps to Dramatically Happier Clients: Lessons from the Airline Industry argues for a fundamentally different mindset in how you treat your very best clients.

Vanguard’s Lesson on Great Client Communications outlines how some of today’s most successful investment firms are making videoconferencing technology a central part of their client communication strategy.

The Central Question for your Business poses the most important question for any business and one that is critical for advisors today.

Why Clients Ignore Your E-Newsletters sets out six ways to ensure that clients read your e-newsletters.

Dan Richards conducts programs to help advisors gain and retain clients, and is an award winning faculty member in the MBA program at the University of Toronto. To see more of his written commentaries, go to www.danrichards.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All