Why Bitcoin Is Not in a Bubble

Membership required

Membership is now required to use this feature. To learn more:

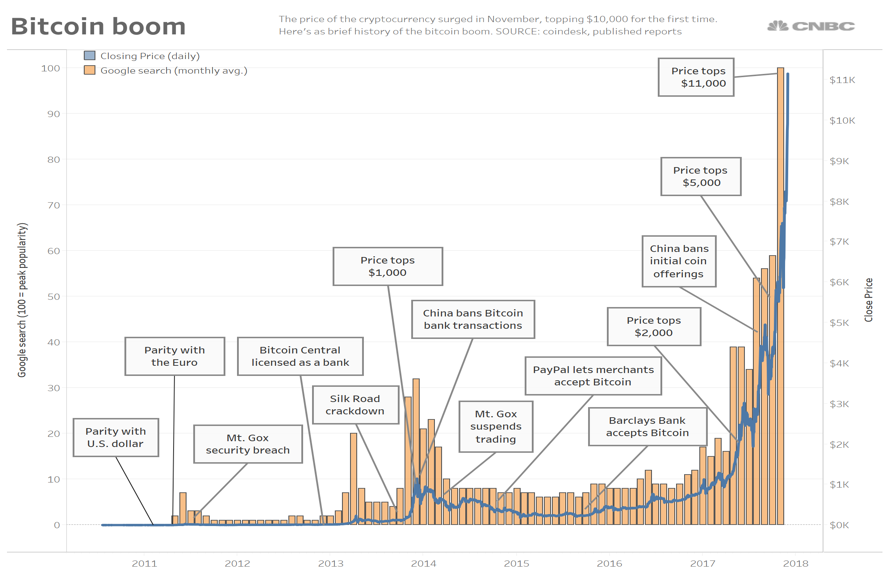

View Membership BenefitsDuring 2017 bitcoin rose from $900 to $20,000. As I write this, it was priced around $16,000. According to Warren Buffett, in Forbes in November 2017, “You can’t value bitcoin because it’s not a value-producing asset… it’s a real bubble… It doesn’t make sense...I don't believe in this whole thing at all. I think it’s going to implode." Jared Dillian of Mauldin Economics expects bitcoin to eventually be priced around $150.

It is newsworthy how many investors and analysts have recently asserted that bitcoin – and by extension, all cryptocurrencies – are in a bubble. This in a day where the Dow is up to almost 26,000 and all indexes are at all-time highs. A few analysts are saying the stock market is in a bubble.

Yet Robert J. Shiller, Vanguard Founder Jack Bogle, James Rickards, Peter Schiff, Ray Dalio, CEO of JP Morgan Jamie Dimon, Nobel Laureate Joseph Stieglitz, and others have all stated in the past year that bitcoin is a “fraud,” “it ought to be outlawed,” or it is in a bubble.

This was all before bitcoin hit its recent all time high of almost $20,000. Since then, it corrected to almost $11,000, or down about 40%, bitcoin’s largest correction since 2013. But then it rebounded into the $15,000 range, then corrected again.

If there is a bitcoin bubble is it bursting or about to burst? As I said in my September 2017 article, Are Cryptocurrencies The Best Investment Opportunity Of The Next Decade? Part Two, “None of the numerous articles that declare cryptocurrencies are a bubble (see here, or here, or here) seem to have any understanding of why or what constitutes a bubble...Amazon (2010) and Apple (around 2012) both looked high at prices of $100 and $80 and were accused of being in bubbles – but at prices of 970+ [currently, 1150+] and 150+ [170+] today one would question the past evaluation.”

Some investors – Schiff in particular – make some salient points about bitcoin and bubbles. Therefore, it is worth examining the nature of bubbles, and the arguments that cryptocurrencies are in a bubble, to determine whether the space is still worthy of investment.

Why the cry ‘bubble!’?

Analytic capabilities appear to fail when it comes to crypto. So many assert the bitcoin bubble you would think the contrary position would be gaining advocates.

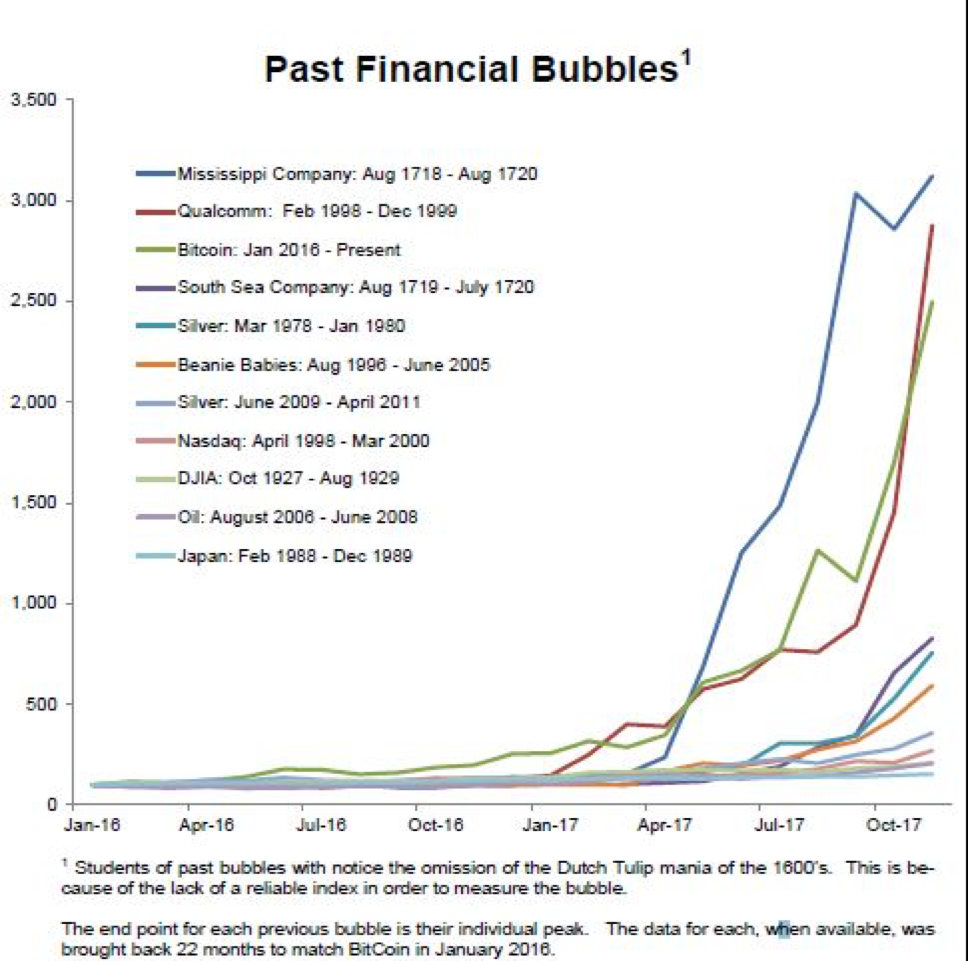

According to Birinyi Associates, bitcoin is already one of the biggest bubbles of all time, larger than the NASDAQ bubble of the 1990’s (see chart above). But again, none of these analysts or articles explain why bitcoin is a bubble; they only assert that it has bubble qualities, by which they mostly mean that it has experienced a sustained parabolic rise.

Is a parabolic rise a necessary and sufficient condition to label a phenomenon a bubble? Necessary, perhaps, sufficient no. More to the point is John Authers’ view in Bitcoin Bubble Follows Classic Pattern Of Investment Mania that the value for bitcoin cannot be shown.

The crux of the issue is that analysts see bitcoin and cry ‘bubble’ because they don’t understand either term. Is bitcoin a stock? Is it a commodity? Is it a currency? Where is the value, and how should it be determined?

What is a bubble?

“Parabolic” is usually used to indicate a steep rise, but a bubble is not exclusively defined as a steep rise in price, as some pundits seem to assume. According to Investopedia, “The term "bubble," in the financial context, generally refers to a situation where the price for an asset exceeds its fundamental value by a large margin.” If this is a basic working definition, then a bubble involves two primary elements: price and value. Other paradigms flesh this out some.

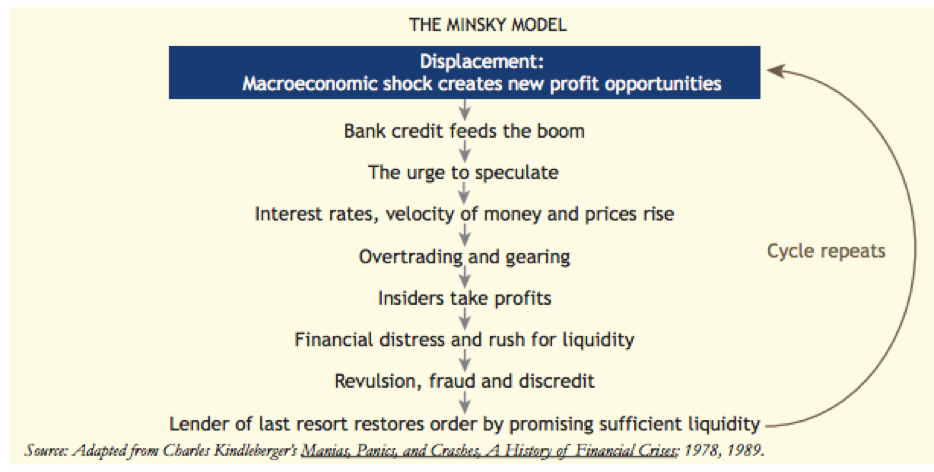

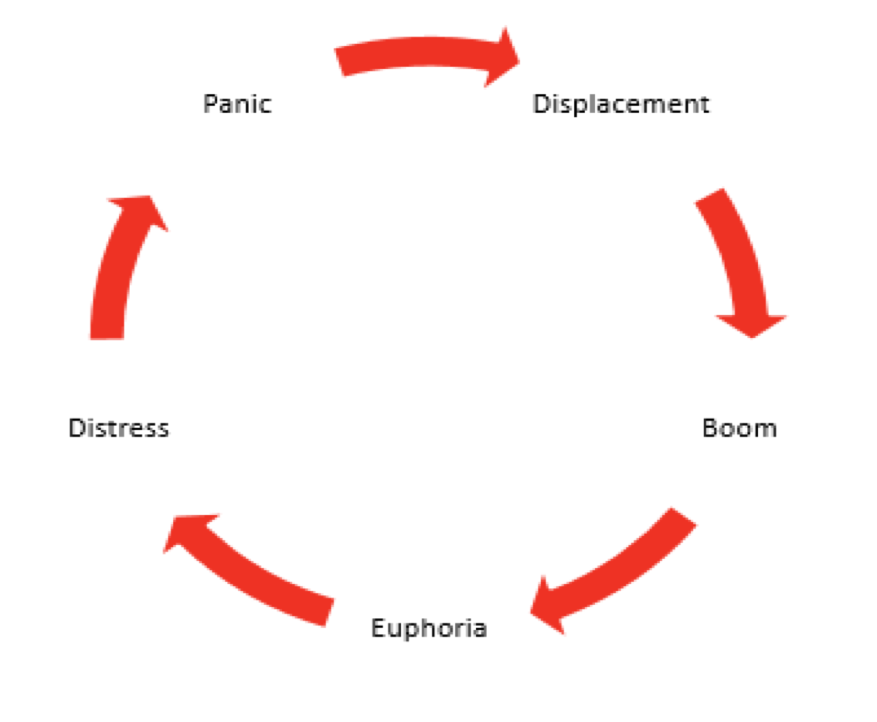

Economic historian Charles Kinderberger applied Hyman P. Minsky’s model of credit cycles to financial crisis in his 1978 book Manias, Panics, and Crashes. The Minsky Model identified nine stages of a credit cycle (see chart), which Kinderberger refined to five stages (see red circular chart below) and compared to most stock market or single stock bubbles: Displacement, Boom, Euphoria, Crisis or Profit-Taking, and Revulsion or Panic. Today, this has been called the Kinderberger-Minksy model of a bubble.

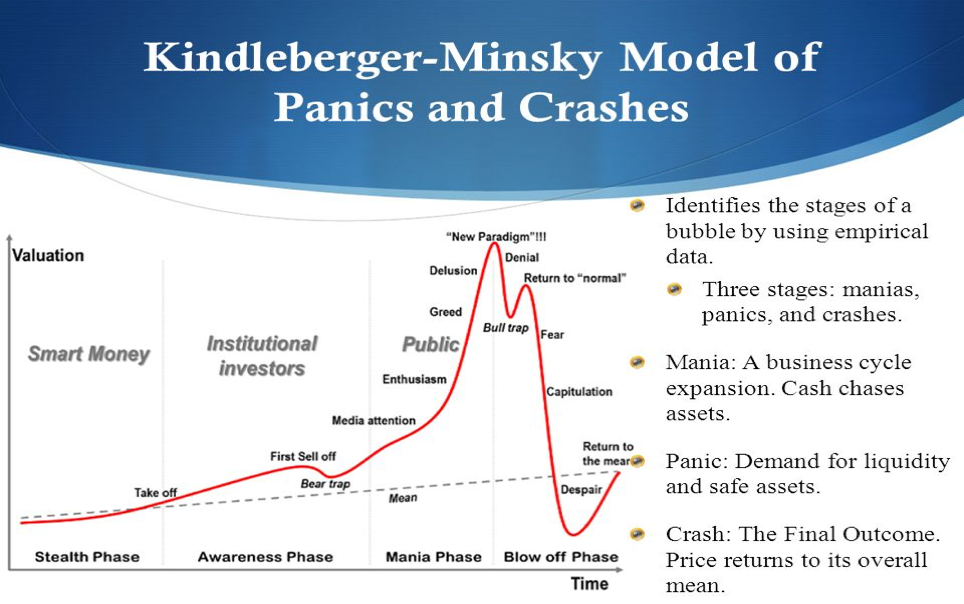

Dr. Jean-Paul Rodrigue, a professor at Hofstra University, proposed a four-stage modification in 2008 that is used by many financial analysts and revises Kinderberger’s stages of a bubble to Stealth, Awareness, Mania, and Blow-Off (blue-red chart below).

One of the more recent classic examinations of the characteristics of a bubble was done by GMO’s Jeremy Grantham. Grantham, who believes that neither U.S. stocks nor bonds will beat inflation over the next seven years, defined a bubble as a two-standard deviation move from a market’s long-term average (in price/earnings). Note that by this definition, Grantham is focusing on price and earnings, which relates to value.

In one of Grantham’s earliest GMO Quarterly letters on bubbles he said, “The necessary conditions for a bubble to form are quite simple and number only two. First, the fundamental economic conditions must look at least excellent – and near perfect is better. Second, liquidity must be generous in quantity and price: it must be easy and cheap to leverage.“ We might call these Grantham’s ex-price/value bubble criteria.

Analysis of value and price: Is bitcoin in a bubble?

The sine qua non for bubbles might be fundamental value relative to excessive price, but how does one measure the fundamental value of bitcoin or other cryptocurrencies? As a recent Coindesk article on Ripple opines, “there’s no foolproof way to value Cryptocurrencies.” It has not been determined how important blockchains will be to the global economy or how direct the value correlation is to cryptocurrencies.

Even if we could apply a reasonable facsimile of Grantham’s two-standard deviation criterion to bitcoin, and by extension, all cryptocurrencies, it is not the same. Bitcoin is not a stock. There is no product or service and it does not generate an income stream.

Bitcoin is the face of blockchains and digital currencies. It might be called part stock, part emerging currency, and part commodity. As a kind of stock, Cryptocurrencies have become - to retail investors - the de-facto face of the blockchain they represent, even though at times, a direct correlation cannot be shown. They are more like fiat currency, because they are the digital face of the fiscal and economic potential of blockchains and digital ledger technology (DLT) in the same way a fiat currency is the face of the economic potential of a nation. The present and future value of bitcoin are impossible to accurately estimate.

The rising value of bitcoin is the result of the present valuing of a future stream of potential benefits. If in the future it exceeds these benefits the price may go much higher. If it disappoints, the price may crash. This is why price/value comparisons of bitcoin based on Grantham’s paradigm, like the one recently noted in The Guardian, just don’t work. As the Commodity Futures Trading Commission (CFTC) notes, this is still a risky speculative investment – and speculative investments are prone to bubbles. However, this does not mean that bitcoin is currently a bubble.

Per Grantham’s ex-price/value criteria, the fundamental conditions of the economy are improving, but certainly not excellent. There is credit (margin) but exchanges are still difficult to navigate for the uninitiated. There is also still a lot of cash on the sidelines and both the stock market and the cryptocurrency markets continue to climb a ‘wall of worry.’

Analyst and trader Willy Woo may or may not be overstating when he says in Bitcoin Investing, “It’s not in a bubble. We're on the path of digitizing the world. We are seeing the final phase of the Post-Industrial Revolution which started in the 1960s-1990s with the invention of the microprocessor through to the expansion of the Internet.” Time will tell.

Analysis of the Kinderberger-Minsky model: Is bitcoin in a bubble?

If we compare cryptocurrencies to Kinderberger’s adaptation of Minksy’s cycle, where are they? Starting in reverse order, definitely not in panic (five stage model), or blow-off (four stage). So far at least, Bitcoin’s price has always rebounded.

As for the profit-taking (distress/crisis) phase: There have been times when the bitcoin price has been cut in half following steep rises, but rather than indicative of massive profit taking (in fact, by most reports those who have bitcoin hold onto it like it was gold in a depression), it appears to be reaction or panic to market news. For example, the dive in the market after China announced closure of its exchanges. Profit taking occurs in the small corrections after a run-up, like the recent correction to $15,703 after a run up from $10,815 to $17,630 in one week. The more recent run-up to close to $20,000 followed by a 40% correction to around $11,000 may have been caused by news of South Korean regulation and year-end profit taking. But these are smaller corrections than some of those in the past.

Are we in euphoria? Neither my uncle nor cousin or grocery clerk or any waiter are bragging about becoming millionaires on Cryptocurrencies yet and most people that I talk with don’t know what they are, much less anything about blockchains or DLT. Anecdotally, the average person in the United States, Korea, or the Philippines might or might not have heard of bitcoin – but they certainly don’t even begin to understand it. According to Investopedia, in the euphoric stage of the dot.com bubble, “at the height...in March, 2000, the combined value of all technology stocks on the Nasdaq was higher than the GDP of most nations.” We’re not even close to anything like this with cryptocurrencies.

In this way Woo, in Bitcoin Investing: A 10,000 Year View, is incorrect that bitcoin is in the early stages of the mania phase. Smart money is just beginning as is the awareness of the average retail investor, and the obstacles to retail investors are in the early stages of being overcome. According to a CNBC interview with Brian Kelly, portfolio manager of the BKCM Digital Asset Fund, “If you look at the internet in 1995, that's where you are in digital currencies.”

Are we in the boom phase? Without question bitcoin and cryptocurrencies have gained increased media attention since around 2012 to 2013, but institutional money is just weighing whether or not to invest. What is true is that bitcoin and cryptocurrencies – as well as the technology that undergirds them – is gaining increased attention and becoming more widely known. Yet, even many of those who are inclined to invest don’t have the basic understanding of how to invest. Exchanges are still responding slowly and most seem overwhelmed. Coinbase has been reported to have over 250,000 new sign-ups every week, a factor driving the popularity of its three (now four, including bitcoin cash added in December) trafficked currencies bitcoin, llitecoin, and ethereum.

The small amount of investment relative to global assets says that this is a ‘boom’ in its very early stages. Cryptocurrencies are still just a little over $500 billion of total managed assets compared to over $80 trillion world wide – expected to rise to over $100 trillion by 2020. Total client assets, managed and un-managed, are expected to rise to close to $300 trillion. Cryptocurrencies are not even 1% of this total yet. Blockchains and DLT are still being tested and have not come close to being fully integrated in industry.

This is why some displacement may still be ahead. Bitcoin, and other Cryptocurrencies, have not yet clearly displaced anything. At least not in the same way as low interest mortgages replaced higher interest mortgages in the early 2000’s or dot coms replaced more sane investments in the stock market run up of the 1990’s. Real technological displacements may still be to come. According to one source, ‘social capital’ is just beginning to develop and it’s not clear whether it will take hold around cryptocurrencies or not. Bitcoin could still crash – but not because it is in a bubble.

Bitcoin – though different than Amazon – has defied most value and bubble chart analysis over its history. Kurt Eichenwald’s 2013 article for Vanity Fair, The Logic Problems That Will Eventually Pop The Bitcoin Bubble is a treasure trove of quotes you would not want to be credited with now that bitcoin has endured, taken off, and recovered multiple times. He makes some superficial points, namely that, at the time at least, it didn’t act like a currency (nor does it now, really) and that though it is not a Ponzi Scheme it can be better compared to the tulip and bulb craze of the early 1600’s in Holland.

The problem with his currency comparison is that in five short years the bitcoin ‘currency’ has surpassed most currencies in the world in value – without even having a nation behind it. How can you compare a nascent, digital currency without a nation’s governmental and economic structure behind it to the characteristics of a developed stable currency?

Bitcoin should also not be compared to tulips, because tulips are just...tulips. Bitcoin is backed by the revolutionary technology of blockchain and DLT and so far, at least, validated as a potential future currency and global payment facilitator by an increasing social network that includes central banks, governments, corporations and individuals, not to mention the CBOE and potential ETF’s that are likely to be approved in 2018. The Tulip craze spanned four months. Bitcoin’s ‘bubble’ has lasted at least two plus years and counting. Bottom line? Eichenwald’s ‘logic problems’ are that his article traffics in false analogies.

So, where are we? It seems likely that because the disrupting phase of blockchains and DLT cannot be shown to be over – and may likely be just beginning – that the entire phase of bitcoin from its 2009-10 inception to the present may be a long disruptive-early boom stage. That is, bitcoin and Cryptocurrencies may only be in the mid-boom stage of their development with plenty of upside to go. The mania-euphoric stage has not even begun.

According to The Guardian on December 2, 2017, the cryptocurrency market has been dominated by crypto nerds and retail investors – serious investors are just coming on board. If true, this is typical of the early Boom (5 stage cycle) or Awareness (4 stage cycle) phase of the cycle. As Mohammed El-Erian says for Bloomberg just this week, recent data from the U.S. Commodity Futures Trading Commission shows that bitcoin has a “notably segmented investor base.” According to the CFTC data, those long on bitcoin are dominated by individual retail investors. Professional investors dominate the shorts. Institutional investors have, so far, stayed on the sidelines. The key to bitcoin’s sustainability will be their entrance into the mix. Regardless of the model applied, bitcoin looks to have much more room to run.

Why bitcoin is not in a bubble

There are many reasons bitcoin may fall from where it is today. There are also many reasons it may continue up. Bitcoin may or may not fulfill its potential as the ‘face’ of digital currency, the blockchain, and DLT. It may or may not end up being the top cryptocurrency. It may or may not fulfill its potential value. This is the nature of a speculative investment and is different from saying that it is in a bubble.

According to Chris Kline in Forbes, Five Reasons Bitcoin Will Be Your Best High Growth Investment In 2018, bitcoin will continue to grow as a result of approved ETFs, institutional investors entering the space, and greater accessibility through exchanges like Coinbase, among other factors.

According to Marie Wieck, Manager of the IBM Blockchain, “IBM believes that one day, just as the internet became the business standard of communication, blockchain will be how all of us share and verify data.”

Cryptocurrencies like bitcoin are presently the best retail face of the blockchain. The most pertinent question relative to bitcoin is still, “Do you believe in the future value of the blockchain and DLT?”

Could bitcoin become a bubble? Yes. Will all cryptocurrencies survive? No. Is it possible that many, including bitcoin, could crash and burn? Yes. Should investors put their life savings into the space? No. Will bitcoin continue to experience significant corrections after run-ups? Likely. Should an investor or speculator diversify and have a plan for taking profits, ideally at the tops after run-ups? Yes. Will the cryptocurrency space continue to be volatile and risky for the foreseeable future? Likely.

Though all of the preceding is true, cryptocurrencies are here to stay and there is yet profit to be made. Is bitcoin in a bubble? Not even close.

Seaborn Hall, AIF, has a degree in management from Georgia Tech, a Master’s degree and has studied at the doctoral level. Formerly he was a Regional Director at a national top-50 RIA; he currently manages a family investment company, writes, and publishes the Common Sense Interpretation Websites. He holds positions in ARKK, some companies in ARKK’s portfolio, plus IBM and Nvidia. He has Coinbase and Kraken accounts and positions in bitcoin, ethereum, and litecoin. This report should not be viewed as investment advice or a recommendation, but is for informational purposes only.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All