Capital Efficiency Trumps Fees in the Search for Portfolio Diversifiers

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Returns to the simplest domestic capitalization-weighted indexes have dominated virtually all active strategies over the nine years since the global financial crisis. It’s not hard to understand why many investors have opted to eschew active strategies altogether, and instead have migrated en masse to the lowest cost index products. And, for most investors, when considering traditional active long-only equity or bond mutual funds, it is prudent to place a high priority on fees. After all, most equity mutual-funds and smart-beta index products will have a correlation of 0.8 or higher to a traditional 60/40 portfolio1. As a result, they are likely to produce only small marginal benefit in terms of portfolio efficiency.

However, the equation changes when investors consider allocations to alternatives, such as market-neutral and managed futures strategies.

Alternatives are constructed to capture returns from sources that are structurally uncorrelated with equities and bonds. Therefore, they may be expected to be uncorrelated to core portfolios, and substantially improve portfolio efficiency by increasing returns, reducing volatility, or both. However, many investors in alternatives evaluate these products using the same criteria that they use to evaluate traditional funds.

This is a mistake.

The evaluation of alternatives introduces an extra dimension into the equation that investors don’t need to think about with traditional equity funds. It’s the concept of capital efficiency.

Capital efficiency measures the amount of market exposure one can achieve with an investment per unit of capital invested. This has become a central theme for many institutional investors, who understand that they may face low expected returns on capital in their core portfolios over the next few years.

Capital efficiency can be best understood as “bang for your buck.”

Consider two funds, A and B, with similar expected Sharpe ratios, fees and taxes. In other words, the funds are equally efficient. However, fund A is run at 6% volatility while fund B is run at 12%. This is possible in the world of alternatives because they often use leverage or derivatives like futures.

Given that fund B runs at 2x the volatility of fund A, fund B should be expected to produce 2x the excess return. In other words, an investor who carves out 20% of their portfolio to invest in liquid alternatives would gain 2x the marginal improvement in returns and Sharpe ratio on their portfolio by investing in fund B instead of fund A.

Three alternative funds walk Into a bar

To help illustrate the point, imagine an investor owns a traditional portfolio consisting of 60% in a U.S. equity index ETF and 40% in a bond index ETF. Acknowledging that expected returns are low for both stocks and bonds at the current time, the investor wishes to diversify with a 20% allocation to alternative investments. His objective is to raise his expected returns with minimal risk.

He evaluates his options and identifies three attractive funds:

- A market-neutral equity fund with an expected gross Sharpe ratio of 1.1, targeting 7% annualized volatility on up to 300% gross exposure, with a gross expense ratio of 2.24%, and 0 correlation with the current portfolio;

- A managed-futures mutual fund with an expected gross Sharpe ratio of 1.1 , targeting 12% annualized volatility on up to 300% gross exposure, with a gross expense ratio of 2%, and 0 correlation with the current portfolio; and

- A global tactical asset-allocation (GTAA) ETF of ETFs with an expected gross Sharpe ratio of 0.8, expected long-term average annualized volatility of 8.25% on a maximum of 100% gross exposure, with a gross expense ratio of 0.8%, and a correlation of 0.5 with the current portfolio.

Let’s dig a little deeper into how I arrived at these assumptions.

Market-neutral fund

The market neutral fund is, by definition, hedged against market beta. Thus, it’s reasonable to assume it will have a consistent correlation (beta) of zero to the market. If the fund has equal risk exposure to five uncorrelated styles (say size, value, quality, investment, and momentum) with average Sharpe ratios of 0.5, the expected Sharpe ratio of a well-crafted portfolio is about 0.5 x ![]() =1.1 2.

=1.1 2.

A quick glance at larger equity market-neutral funds shows that they tend to exhibit between 5% and 7% volatility, so I chose an estimate near the top of the range to give this option the benefit of the doubt (you’ll see why below). I used a fee estimate from a fund managed by a very large quantitative shop that is known for competitive fees in the alternative space.

Market-neutral funds typically turn-over greater than 100% of their portfolio per year, and all gains are taxable as ordinary income.

Managed-futures funds

A managed-futures fund typically allocates to a large basket of global asset classes across equities, bonds, currencies and commodities, and sometimes to more esoteric markets like carbon credits.

A study by Hurst, Ooi and Pedersen (2017)3 found that a diversified trend-following strategy produced excess returns of 11% annualized, net of estimated trading costs, on volatility of 9.7% over 126 years from 1880-2016, for a Sharpe ratio of 11%/9.7%=1.1.

In its worst decade (1910-1919) the strategy produced net returns of 4.1%, while it produced over 20% annualized returns in its best decade (1970-1979).

Many managed-futures strategies combine trend signals with carry signals, and this combination has improved the results to trend strategies in historical testing4. When managed-futures funds are properly constructed, 60% of gains on trading would typically be taxed as long-term capital gains, while 40% would be taxed as regular income.

Global Tactical Asset-Allocation (GTAA) ETF

The website Allocate Smartly has taken the time to replicate over 40 GTAA strategies using a common data set over similar time horizons.

I examined data from the site and found that the average strategy produced 8.6% annualized returns net of estimated trading costs with 8.25% annualized volatility. Excess returns were 6.6% annualized after subtracting a 2% risk-free rate. The average of pairwise correlations for all strategies with a U.S. 60/40 portfolio was 0.5, and the strategies produced an average Sharpe ratio of 0.8.

A survey of GTAA ETFs listed on U.S. exchanges indicated a range of fees between about 0.8% and 1.7%, so I chose a fee estimate near the bottom of the range. In many cases, trading within ETFs does not produce taxable gains until the fund is sold, at which time an investor pays capital gains on the difference between sale and purchase prices.

A horserace between funds

How might the investor analyze the relative benefits of these funds to a portfolio over a 10-year horizon, given his objective to add a 20% allocation to these funds? For my analysis, I assume the core 60/40 allocation is held indefinitely (ignoring tax implications of periodic rebalancing), but the alternative fund is sold after 10 years.

Let’s assume the 60/40 portfolio has an expected net after-tax annualized return of 4% with average 12% annualized volatility. For the purpose of our analysis, it’s simpler to deal with excess returns, net of the expected risk-free rate5. If we assume a 2% expected risk-free rate over the next 10 years, the 60/40 portfolio is expected to produce 2% excess annualized returns, with an expected Sharpe ratio of (4%-2%)/12%=0.17 . I assume zero fees on the core portfolio to reflect the costless options available to investors at Schwab, Fidelity, and other dealers, and the near-zero fees on many core ETFs.

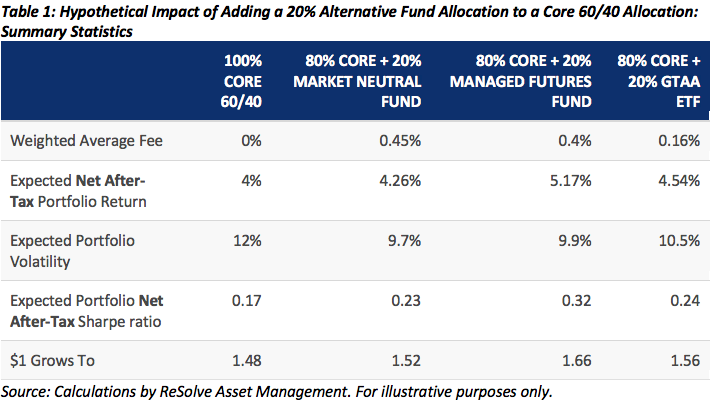

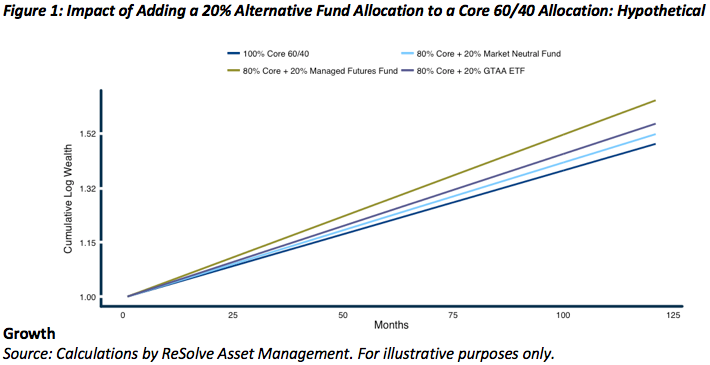

I assume a tax rate of 39.6% on ordinary income and 23.8% on long-term capital gains6. Table 1 summarizes the impact of adding a 20% allocation to each of our three hypothetical funds to the 60/40 portfolio, while Figure 1 illustrates the potential difference in ending portfolio value.

I present a detailed breakdown of the analysis that led to the values in Table 1 in an Appendix below.

From Table 1 it’s clear that a 20% allocation to the alternative mutual funds adds up to 0.45% in weighted average portfolio fees, compared with just 0.16% in fees from the addition of the GTAA ETF. However, despite these higher fees and less advantageous tax status, a hypothetical 20% position in the managed-futures fund increases expected wealth creation after 10 years by 1.37 times what would be expected from the core 60/40 portfolio on its own. This compares to improvements of just 1.08 times and 1.17 times the wealth creation that would be expected when capital is allocated to the market neutral fund and GTAA ETF, respectively.

The key point is that the improvement in capital efficiency from managed futures overwhelms all other considerations.

In addition, due to the low correlation between the managed-futures fund and the core portfolio, the improvement in hypothetical returns is achieved with just slightly higher portfolio volatility than what we’d expect from an investment in the market-neutral fund, and lower volatility than an investment in the more highly correlated GTAA ETF.

As a result, an investment in the hypothetical managed-futures fund could boost portfolio Sharpe ratio by 1.88x, representing a much larger boost than what one could achieve from the other funds.

Takeaways

The evaluation of alternatives introduces an extra dimension into the equation that investors don’t need to think about with traditional equity funds. Capital efficiency measures the amount of market exposure one is able to achieve per unit of capital invested. In other words, it quantifies “bang per buck” of an investment.

All things equal, it is often more advantageous to a portfolio’s performance, from an after-fee, after-tax perspective, to allocate capital within the alternative sleeve to strategies with low correlation and high target volatility, especially if the strategy trades futures. This is true even if these funds have higher fees and less favorable tax treatment. Focusing exclusively on fees and taxes is unnecessarily short-sighted.

The advantages of allocating to capital-efficient alternatives may be magnified through thoughtful “asset location.” In other words, investors with retirement accounts have the opportunity to hold less tax-efficient investments in IRAs or 401ks in order to defer or perhaps even eliminate the tax drag.

Build your own report!

The article above illustrates how capital efficiency, taxes and fees impact portfolio choices given reasonable assumptions.

However, you may have different views on these variables.

That’s why I prepared a simple online application so that you can generate a bespoke report based on your own assumptions.

Just set your variables and generate your report - Go to the app now!

Adam Butler, CFA, CAIA, is Co-Founder and Chief Investment Officer of ReSolve Asset Management. ReSolve manages funds and accounts in Canada, the United States, and internationally.

Appendix: Detailed fund by fund analysis

First, it’s critical to standardize the expected return across funds, after fees and taxes.

Market neutral fund

The market-neutral fund is expected to produce gross excess returns of 1.1x7%=7.7%. Now let’s subtract fund fees of 2.24% for net returns of 5.46%. The fund returns are considered 100% ordinary income for tax purposes, so if we assume a tax rate of 39.6%, expected net after-tax return would be 5.46%x(1-39.6%)=3.3%. As a result, the new portfolio would be expected to produce an excess return of 80%x2%+20%x3.3%=2.26% with annualized volatility of 9.7% 7, so that the expected net after-tax portfolio Sharpe ratio would be ![]() . All gains are crystallized each year.

. All gains are crystallized each year.

Managed futures fund

The managed futures mutual fund is expected to produce gross excess returns of 1.1x12%=13.2% less fund fees of 2% for net returns of 11.2%. Since the fund trades futures, gains should be taxed at 60% long-term capital gains and 40% ordinary income. If we assume long-term gains are taxed at 23.8% and ordinary income is taxed at 39.6%, we can estimate a combined tax rate on gains of approximately 60%x23.8%=40%x39.6%=30.12%, so expected net after-tax return would be 11.2%x(1-30.12%)=7.83%. As a result, the new portfolio would be expected to produce an excess return of 80%x2%+20%x7.83%=3.17% with annualized volatility of 9.9% 8, so that the expected net after-tax portfolio Sharpe ratio would be ![]() =0.32. Again, all gains are crystallized each year.

=0.32. Again, all gains are crystallized each year.

Global Tactical Asset Allocation ETF

Finally, the GTAA ETF is expected to produce gross excess returns of 0.8x8.25%=6.6% . Now let’s subtract fund fees of 0.8% for net returns of 5.8%. Because of the unique tax treatment of trading inside certain ETFs, we will assume the fund crystallizes zero capital gains each year.

However, while taxes on the market neutral and managed futures funds are crystallized in full each year, the ETF structure simply defers capital gains until the ETF is sold. Assuming the ETF is sold at the termination of our 10-year holding horizon, the investor would expect to pay 23.8% long-term gains tax on the compounded gains at termination. If we assume a net growth rate of 5.8% after fees, the fund should turn $1 into $1.76 after 10-years. The investor would pay 23.8% on the gain of $0.76, which reduces the net gain to $0.76x(1-23.8%)=$0.58. Thus, the net expected annualized return actually works out to (1+0.58)(1/10)-1=4.7%.

Therefore, the new portfolio would be expected to produce an excess return of 80%x2%+20%x4.7%=2.54% with annualized volatility of 10.5% 9, so that the expected net after-tax portfolio Sharpe ratio would be ![]() =0.24.

=0.24.

Disclaimer

Confidential and proprietary information. The contents hereof may not be reproduced or disseminated without the express written permission of ReSolve Asset Management Inc. (“ReSolve”). ReSolve is registered as an investment fund manager in Ontario and Newfoundland and Labrador, and as a portfolio manager and exempt market dealer in Ontario, Alberta, British Columbia and Newfoundland and Labrador. Additionally, ReSolve is an SEC registered investment adviser. ReSolve is also registered with the Commodity Futures Trading Commission as a commodity trading advisor and a Commodity Pool Operator. This registration is administered through the National Futures Association (“NFA”). Certain of ReSolve’s employees are registered with the NFA as Principals and/or Associated Persons of ReSolve if necessary or appropriate to perform their responsibilities.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The information contained herein are of an illustrative nature and for informational purposes only and does not constitute financial, investment, tax or legal advice. These materials reflect the opinion of ReSolve on the date of production and are subject to change at any time without notice due to various factors, including changing market conditions or tax laws. Where date is presented that is prepared by third parties, such information will be cited, and these sources have deemed to be reliable. Any links to third party websites are offered only for use at your own discretion. ReSolve is a separate and unaffiliated from any third parties listed herein and is not responsible for their products, services, policies or content of their website. All investments are subject to varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy or precut referenced directly or indirectly in this website will be profitable, perform equally to any corresponding indicated historical performance level(s), or be suitable for your portfolio. Past performance is not an indicator of future results.

1 Author’s estimates based on a small survey of U.S. equity mutual funds and smart-beta ETFs.

2 The volatility of a portfolio with N assets and average pairwise correlations of ![]() . Note that for any

. Note that for any ![]() portfolio volatility will be lower than the average volatility of the constituent assets, while portfolio expected return is constant, resulting in a higher Sharpe ratio.

portfolio volatility will be lower than the average volatility of the constituent assets, while portfolio expected return is constant, resulting in a higher Sharpe ratio.

3 See https://dx.doi.org/10.2139/ssrn.2993026 Exhibit 1.

4 For example the paper “Time-Series Momentum, Carry and Hedging Premium” by Molyboga, Qian, and He (2017) suggests that adding carry to trend improves the Sharpe ratio by 0.17. See https://dx.doi.org/10.2139/ssrn.3075650 .

5 Note that we use annualized returns rather than average returns when translating between Sharpe ratios, returns and volatilities. There are some issues with this, but it was important to compare expected compound growth, which requires annualized returns. The use of arithmetic means rather than annualized (geometric) means should not have any material impact on the economic interpretation of the results.

6 Assumes the highest federal tax bracket for ordinary income (~39.6%), with commensurate federal tax rate on capital gains and dividends and including Medicare Contribution Tax of 3.8% (total of ~23.8%). Source

7.![]()

8.![]()

9.![]()

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All