Why Factors Premiums Should Persist

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

This article originally appeared on ETF.COM here.

There are two big, ongoing debates relative to index (or, more broadly, passive) investing. The first is whether active or passive (which I define as neither market timing nor individual security selection) management is the winner’s game (the one most likely to allow you to achieve your goals). The overwhelming evidence, as presented in my book, “The Incredible Shrinking Alpha,” shows that passive investing is the prudent choice.

The other debate that rages on is if a total-market approach (with John Bogle often seen as the standard-bearer) is “best,” or whether “titling” a portfolio to well-documented factors is likely to produce higher returns, and perhaps higher risk-adjusted returns.

During discussion about this second issue, perhaps the most-asked question I hear goes something like this: We know the historical evidence shows premiums for these factors, but how can you be confident that factor premiums will persist after research about them is published and everyone knows about them? After all, we are all familiar with the phrase “past performance does not guarantee future results.” I thought it worth sharing my answer.

Argument for persistence

The first thing I point out is that we live in a world of uncertainty. There is simply no way to know for certain whether a factor premium will persist in the future; that goes for all factors, including market beta.

A good example demonstrating this point is that, using data from Dimensional Fund Advisors, from 1969 through 2008, the Fama-French U.S. large-cap growth index ex-utilities returned 7.8% and underperformed long-term (20-year) Treasury bonds, which returned 9.0%. That’s a 40-year period in which investors took all the risks of stocks in this asset class (which today constitutes about 50% of the U.S. market’s total capitalization, down from about 70% at the end of 1999) but still underperformed long-term U.S. Treasuries.

Given that any strategy of investing in risky assets can fail to deliver a risk premium, no matter how long the horizon, we must make decisions in the face of uncertainty, recognizing that the best we can do is to put the odds in our favor. That raises another question: How can we best put the odds in our favor?

Potential problems with research findings

A well-documented problem with factor-based investing is that smart people, with even-smarter computers, can find factors that have worked in the past but are not real – they are the product of randomness and selection bias, referred to as data snooping or data mining. I’m reminded of the saying, “If you torture the data long enough, it will eventually confess.”

The problem of data mining compounds when researchers snoop without first having a theory to explain the result they expect, or hope, to find. Without a logical explanation for an outcome, one should not have confidence in its predictive ability.

“P-hacking” refers to the practice of reanalyzing data in many different ways until you get a desired result. For most studies, statistical significance is defined as a “p-value” less than 0.05 – the difference observed between two groups would not be seen even one in 20 times by chance. That may seem like a high hurdle to clear to prove that a difference is real. However, what if 20 comparisons are done and only the one that “looks” significant is presented?

The problem of data mining and p-hacking is so acute that economist John Cochrane famously said that financial academics and practitioners have created a “zoo of factors.”

For example, Campbell Harvey (past editor of The Journal of Finance), Yan Liu and Heqing Zhu, in their paper “…and the Cross-Section of Expected Returns,” which was published in the January 2016 issue of The Review of Financial Studies, reported that 59 new factors were discovered between 2010 and 2012 alone. Furthermore, as reported in a May 2017 Wall Street Journal article, “most of the supposed market anomalies academics have identified don’t exist, or are too small to matter.”

To address this problem, some financial economists have argued that the hurdle for statistical significance should be raised to a p-value of less than 0.01. But there is another way to solve the issue. To minimize the risk of p-hacking, and to give investors sufficient confidence in allocating a portion of their portfolios to a factor (or any alternative investment), my co-author Andrew Berkin and I established the following criteria in our book, “Your Complete Guide to Factor-Based Investing.”

For a factor to be considered for investment, it must provide additional explanatory power to the cross section of returns (it’s a unique source of risk and return not subsumed, or explained by, other well-documented factors already used in asset pricing models) and have delivered a premium (higher returns). However, those are just the necessary conditions.

Because investing isn’t a physical science where we can prove the existence of phenomenon and, thus, establish laws, all we can do is to put the odds in our favor. We can do so by applying the scientific method to hypotheses. The scientific method is a system for answering questions about the world through careful observations and rigorous experimentation. Its basic steps include formulating a question, doing background research, constructing a hypothesis, testing that hypothesis, analyzing the data and then sharing the results.

By applying the scientific method, we can address and minimize the previously discussed risks of data snooping so we can gain sufficient confidence that we are putting the odds in our favor. To do that, we need to add the following sufficient conditions to consider for a factor for investment.

What makes a factor?

In addition to meeting the two necessary conditions, the factor must also meet all of the following criteria:

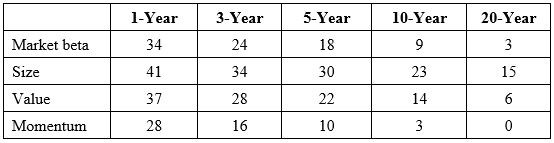

Persistent: It holds across long periods of time and different economic regimes, minimizing the risk that the finding is just a lucky outcome specific to one short period of time. As an example, the following table uses data from Ken French’s website to show the persistence (the odds of a negative premium, expressed as a percentage) of the factors used in the Carhart four-factor asset pricing model. The period is 1927 through 2017.

While no one questions the likelihood (but not the certainty) that the market-beta factor will produce a premium in the future, the value and momentum premiums have similar persistence records (with momentum’s being stronger). Despite the similarity in persistence, I’m asked all the time why I believe it’s likely that the value premium will persist. Furthermore, the size premium’s persistence would look similarly strong if we measured it as we do the other factors.

The size factor, as defined by Eugene Fama and Kenneth French, is constructed by sorting all stocks by market capitalization (as determined by market capitalization of NYSE stocks) into deciles and then taking the weighted average annual return of deciles 6-10 (small-cap stocks) minus the weighted average annual return of deciles 1-5 (large-cap stocks).

In other words, it is the bottom 50% of stocks ranked by size minus the top 50%. Contrast the size factor with Fama and French’s value factor, which is constructed by sorting stocks on book-to-market ratios, then taking the weighted average annual return from deciles 1-3 (value stocks) minus the weighted average annual return from deciles 8-10 (growth stocks). It is the top 30% of stocks ranked by the valuation metric minus the bottom 30%.

Pervasive: It holds across countries, regions, sectors and, where applicable, asset classes.

Robust: It holds for various definitions (for example, a value premium is present whether it is measured by price-to-book, earnings, cash flow or sales); it’s not dependent on one formation that might have been a result of data snooping.

Investable: It holds up not just on paper but also after considering actual implementation issues, such as trading costs.

Intuitive: There are logical, risk-based or behavioral-based explanations for the premium and why it should continue to exist. Investors should prefer risk-based explanations, as they cannot be arbitraged away (although post-publication cash flows can shrink the premium). However, that does not mean we should totally discard behavioral-based explanations, because well-documented limits to arbitrage can prevent sophisticated investors from correcting overvaluations.

Undervaluation is much easier to correct, as an investor can simply buy the undervalued asset, driving its price up. On other hand, to correct an overvaluation, the investor must be able to short the security and bear the risks of unlimited losses and the need to post sufficient collateral on a daily basis.

The presence of evidence across each of these criteria can provide investors the required confidence that a premium is likely to exist in the future – and they are the same reasons that we have confidence – but not certainty – that a market beta premium is likely in the future.

The good news is that, among all the factors in Cochrane’s “zoo,” investors only need to focus on eight that meet our criteria: market beta, size, value, momentum, profitability, quality, term and carry.

What about all those other factors? Some have not passed the test of time, fading away after their discovery, perhaps because of data mining or random outcomes. Or, perhaps the factors worked only for a special period, regime or narrow band of securities. And many factors have explanatory power that is already well-captured by others – they are variations on a common theme (e.g., the many definitions of value).

Summary

Skepticism is healthy, until you are so skeptical you dismiss anything that doesn't agree with your preconceived views. What you should be skeptical about is whether findings are the result of data mining or p-hacking and, thus, are false discoveries. That is why one should not rely only on a single study, even if it shows statistically significant results.

Instead, you should require all the other things I have mentioned before having sufficient confidence to invest. I have observed that their ideology causes some skeptics to do what some call “throwing the baby out with the bathwater” – assuming all findings are bad because some are.

We do have sufficient evidence to be confident once all the requirements I’ve laid out have been met. Others may come to different conclusions looking at the same information. Or, they may have different degrees of confidence. When you reject about 99% of identified factors because they don't meet all the criteria I mentioned, I think that is testament to being sufficiently skeptical about the findings, while also being open enough to consider others and not be blinded by ideology.

In my case, for example, I have more confidence in risk-based explanations than in behavioral ones. However, I choose not to ignore behavioral explanations where limits to arbitrage prevent full correction of mispricings.

Finally, if you are considering, or already engaged in, factor-based investing, I offer these words of caution from the conclusion of “Your Complete Guide to Factor-Based Investing”: “First, as we have discussed, all factors – including the ones we have recommended – have experienced long periods of underperformance. So, before investing, be sure that you believe strongly in the rationale behind the factor and the reasons why you trust it will persist in the long run. Without this strong belief, it is unlikely that you will be able to maintain discipline during the inevitable long periods of underperformance. And discipline is one of the keys to being a successful investor. Because there is no way to know which factors will deliver premiums in the future, we recommend that you build a portfolio broadly diversified across them. Remember, it has been said that diversification is the only free lunch in investing. Thus, we suggest you eat as much of it as you can!”

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All