Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

People associate leverage with volatility and trouble. The history of finance is littered with examples: the savings and loan crisis of the late 1980s, Orange County in 1994, Long Term Capital Management in 1998 and MF Global in 2011. But personal leverage is common; anyone with a mortgage is leveraging their home. The typical 20%-down mortgage gives the buyer five times leverage to their equity.

Leverage is a productive tool, used within limits.

Enter U.S. Treasury bonds. Leverage may not immediately seem to belong with a Treasury, but for three important reasons, leveraged U.S. Treasury bonds make sense as an ordinary investment.

- The cost to borrow is the lowest in the financial markets.

- Leverage unlocks the yield curve to management.

- Leveraged U.S. Treasury bonds can compete with or better hedge against equities.

The cost to borrow is the lowest in the system

In lending markets, the better the collateral, the lower the rate. At one extreme, think of credit card rates that can go up to 30% after a missed payment. This is a loan collateralized only with the threat of a consumer’s credit score. At the other extreme are U.S. Treasury bonds, which, with no credit risk and immediate liquidity, are the best collateral and hence finance at the lowest rate in the system.

U.S. Treasury bonds finance near-to the Fed Funds rate – today 1.875%. Because this is less than what they yield, leveraging provides a positive cash flow spread. On one side, you earn the yield of the Treasury and on the other, you pay the financing rate, the subtraction between the two is the spread. While certainly helpful in a portfolio, it comes with an important caveat. Leverage will often increase yield but it is only part of the total return. The other part, price sensitivity, must always be considered in determining how much leverage to apply.

Sometimes, when the yield curve is inverted, the cost to finance is more than what Treasury bonds yield and, thus, the financing spread is negative. Yet, because an inverted yield curve typically predicts a period of upcoming lower interest rates, this is generally not a bad time to leverage.

Leverage unlocks the whole yield curve to management

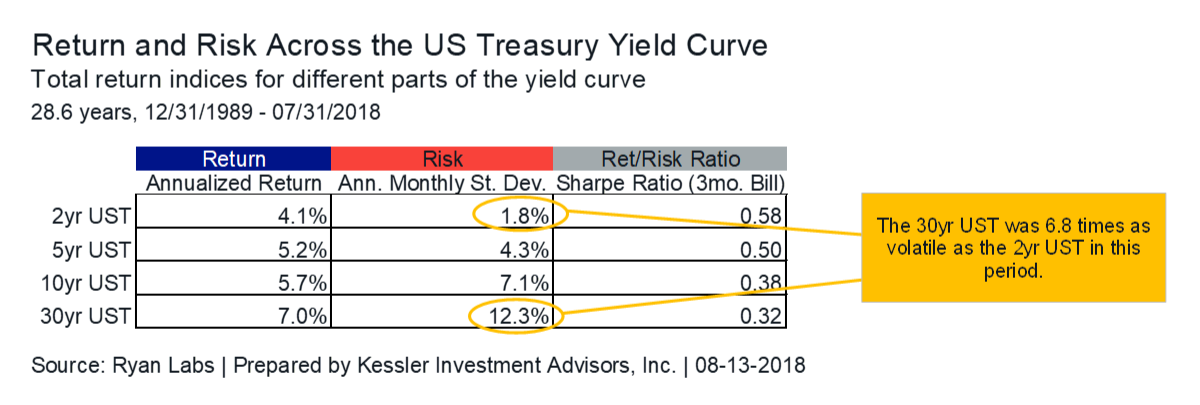

U.S. Treasury bonds offer much more than their yield; their prices appreciate when yields fall and depreciate when yields rise. Investors often buy them with an opinion of where yields are going in the short to medium term. But, inconveniently, their price sensitivity (known as duration) varies greatly depending on maturity. For instance, since 1990, 30-year U.S. Treasury performance is about seven times as volatile as 2-year U.S. Treasury performance (see table below).

Without leverage, investors wanting more opportunity from the Treasury market are stuck with longer maturities (i.e., the 30-year UST). Yet, the short-end of the curve has the best long-term risk/return statistics (see Sharpe ratios above). Leverage, with its multiplicative effect on returns and volatility, can give any part of the yield curve the same opportunity for a given move in interest rates. In bond lingo, leverage can provide duration equivalence.

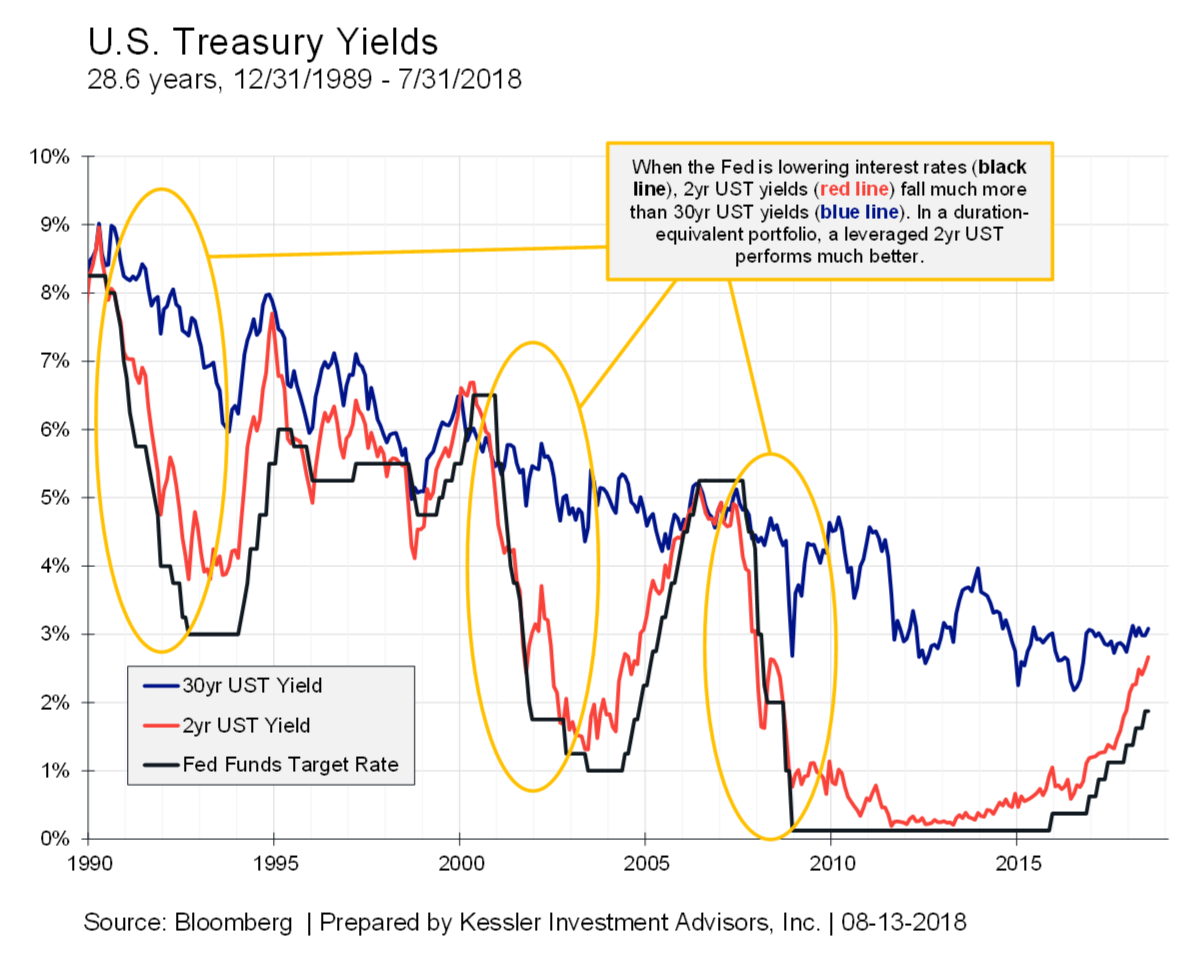

This becomes especially important during periods when the Federal Reserve is lowering interest rates. As you can see in the chart below, in the last three big phases of Fed easing, the 2-year yield falls much more than the 30-year UST. In these periods, it would’ve been more advantageous to own a duration equivalent 2-year U.S. Treasury position than the 30-year U.S. Treasury.

Leveraged U.S. Treasury bonds can compete with or better hedge against equities

While leverage can be used amongst U.S. Treasury bonds to make them more equal, it can also be used to raise their volatility closer to that of other asset classes. This is the risk-parity concept, popularized by Bridgewater Associates in the 1990’s. From Wikipedia,

The risk parity approach asserts that when asset allocations are adjusted (leveraged or deleveraged) to the same risk level, the risk parity portfolio can achieve a higher Sharpe ratio and can be more resistant to market downturns than the traditional portfolio.

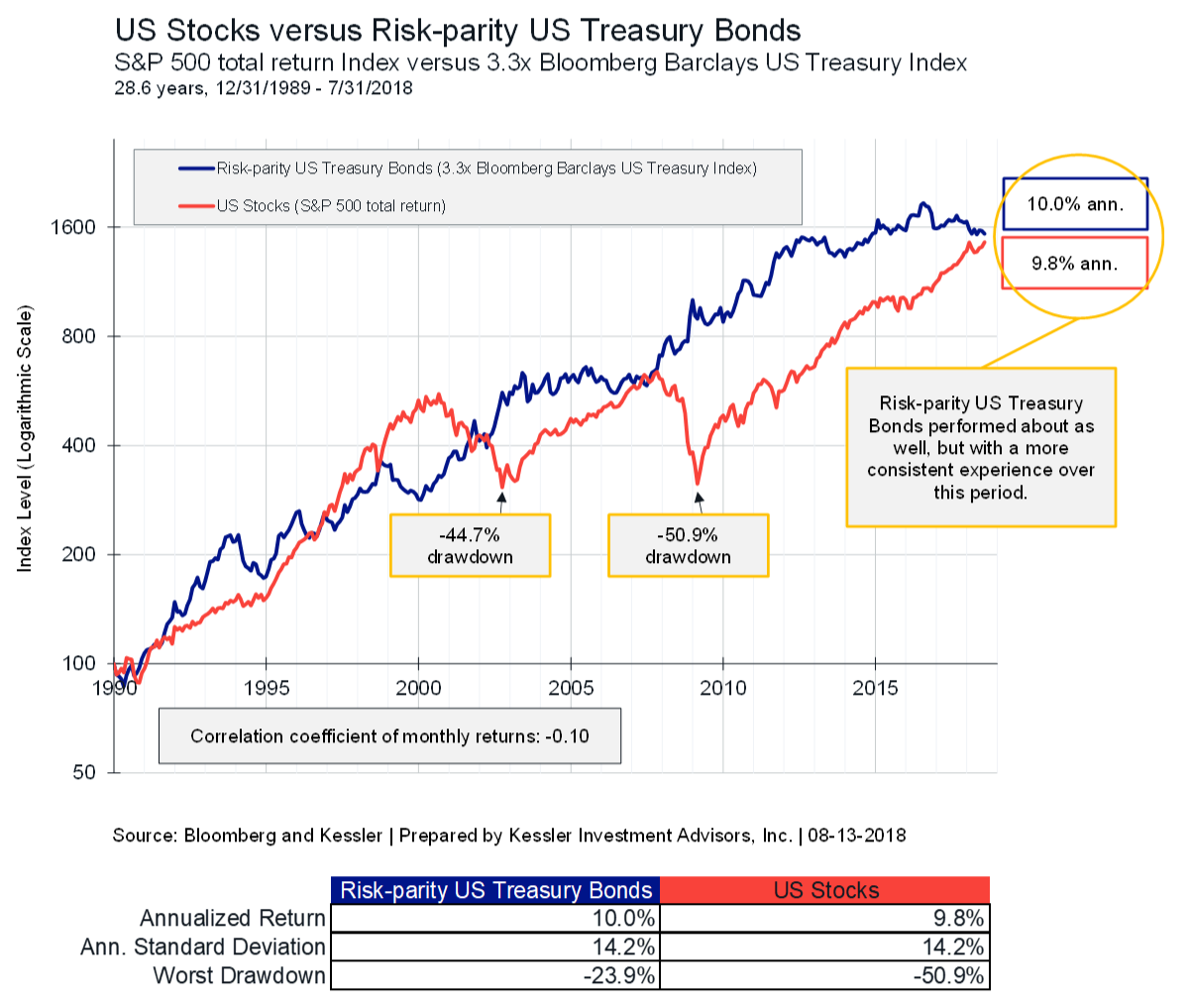

Empirically, the equity market (S&P 500) has been about 3.3-times as volatile as the Treasury market since 1990. Using a simple model of leveraging U.S. Treasury bonds 3.3-times shows a similar return to the equity market but with much smaller drawdowns.

This index is a mathematical transformation of the Bloomberg Barclays U.S. Treasury index performed by Kessler. 3.3 times leverage was chosen as the nearest leverage level (to the tenth) that had the same annualized monthly standard deviation as the S&P 500 over this period. Each monthly index return is multiplied by the leverage amount, 3.3, which then has a financing cost subtracted. The financing cost is calculated as the average daily Fed funds effective rate for each month plus a spread of 0.25% (to be conservative), then divided by 360, and finally multiplied by the actual number of days in the month. This unleveraged financing cost is then multiplied by the leverage amount minus one; or 2.3. An excel worksheet with all calculations is available upon request.

Great, but how do you do it?

For large or corporate accounts, leverage is done through the U.S. Treasury repurchase agreement market (repo for short). But, the most important components are available through the Treasury futures market. Stay tuned for the next part of this two part series: “How to leverage U.S. Treasury bonds using the futures market.”

Eric Hickman is president of Kessler Investment Advisors, an advisory firm located in Denver, Colorado specializing in U.S. Treasury bonds.

Disclaimer: Trading futures involves the risk of loss. Please consider carefully whether futures are appropriate to your financial situation. Only risk capital should be used when trading futures. Investors could lose more than their initial investment. Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Read more articles by Eric Hickman