Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article originally appeared on ETF.COM here.

Because of the risk of data mining, an important criterion for considering an investment strategy (such as a factor) is to not only see that a factor adds explanatory power to the cross section of returns while delivering a premium, but that the premium is persistent across time and economic regimes and is pervasive around the globe. By examining the performance of factors outside of the U.S., we create out-of-sample tests.

Looking beyond the U.S.

Matthias Hanauer and Jochim Lauterbach contribute to the literature on asset-pricing models with their August 2018 study “The Cross-Section of Emerging Market Stock Returns.” Using monthly stock returns for a total of 28 emerging market countries and a sample period of 21 years (July 1995 through June 2016), they investigated the predictive power for an extensive set of factors, not only covering the categories of value, profitability and investment, but controlling for market beta, size and momentum.

To avoid their results being driven by micro stocks, they were excluded. (Although micro stocks represent only 3% of the total market capitalization of their emerging market universe, they account for 43% of the number of stocks.)

Following is a summary of their main findings:

- Value, profitability and investment are priced in emerging markets as well as developed markets.

- The anomalous returns associated with cash flow-to-price, gross profitability, composite equity issuance and momentum are pervasive, as they show up in equal- and value-weighted sorts as well as in cross-sectional regressions. However, ROE, ROA and size factors show no clear relationship.

- In contrast to the prediction of the CAPM, there is not a positive relationship between market beta (risk) and return.

- Their derived return forecast also works in a long-only big stock portfolio, and takes reasonable transaction costs into account.

The above results were consistent with those of Yigit Atilgan, K. Ozgur Demirtas and A. Doruk Gunaydin, authors of the August 2018 study “The Cross-Section of Equity Returns in Emerging Markets,” which covered 27 emerging market countries over the period 1988 to 2014.

Before closing, we can examine whether factors are actually implementable. We can do this with a live test with more than 20 years of live fund data. This is important, because often anomalies that appear on paper disappear after accounting for all the costs of implementation.

Implementation

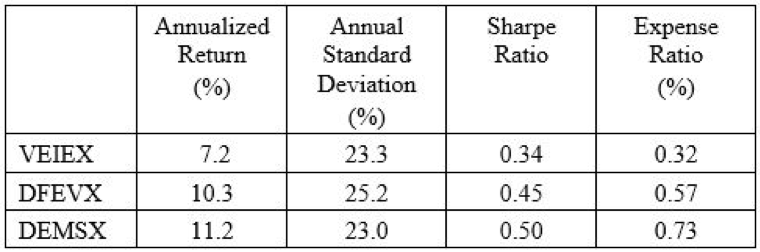

To test whether factor premiums can be captured in emerging markets, where trading costs are larger than they are in the U.S. and other developed markets, we can examine the returns of the DFA Emerging Markets Small Cap Portfolio (DEMSX) and the DFA Emerging Markets Value Portfolio (DFEVX) and compare them to those of the Vanguard Emerging Markets Stock Index Fund (VEIEX). Data is from Portfolio Visualizer and covers the period April 1998 (the first month when all three funds were live) through July 2018.

Not only did the two Dimensional funds deliver higher returns, they provided higher risk-adjusted returns. And they did so despite having higher expense ratios. (Of course, investors must also be willing to accept the different risks of factor-based funds, including the tracking error that can occur.)

This demonstrates that those focusing solely on expense ratios are often missing the bigger picture. One should consider not just the expense ratio but the expense per unit of exposure to factor premiums. In other words, these three funds are not commodities. They provide different exposures to factors with premiums. And it’s the value-added that should matter, not the expense. (Full disclosure: My firm, Buckingham Strategic Wealth, recommends Dimensional funds in constructing client portfolios.)

Summary

The out-of-sample tests provide support for the common factors found in asset pricing models. They also provide support for cash-flow-based measures of profitability providing superior explanatory power over ones that do not account for accruals. These findings provide investors with increased confidence that the factor premiums will persist.

Disclosure: The funds discussed in this article have been selected for informational purposes to illustrate the data and are not provided as a specific recommendation to purchase a particular security. Past performance is historical and does not guarantee future results.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

Read more articles by Larry Swedroe