On Pig Farming, Cobwebs and Howard Marks

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits I can guarantee a few things about Howard Marks’ new book, Mastering the Market Cycle. You will enjoy the thoughtful writing in clear language, and you will learn one great, and I believe correct, idea about the operation of markets.

I can guarantee a few things about Howard Marks’ new book, Mastering the Market Cycle. You will enjoy the thoughtful writing in clear language, and you will learn one great, and I believe correct, idea about the operation of markets.

But you will not master the market cycle. Nobody can.

What you can do, as part of a broader program of self-education in economics, finance, and investing, is to understand better why market prices seem to run in cycles, and market psychology swings between euphoria and despair with more or less predictable regularity. This book should be a part of that self-education strategy.

Ultimately, however, Mastering the Market Cycle is disappointing because it relies on repetition, rather than intellectual exploration, to teach one big idea: Market cycles are best understood as extremes of risk perception, not of price. When everybody thinks there is no risk in the market and that all will work out well, sell. When almost everybody thinks the market is almost infinitely risky and that nothing will work out well, buy.

That’s it. The idea is repeated as a general principle and specifically for high-yield debt (the asset class in which Marks, the founder of Oaktree Capital, made his first and best-known fortune), distressed debt, equities, and real estate. Sell when others are indifferent to risk; buy when there’s blood in the streets, said Nathan Mayer Rothschild (1777-1836). So says Howard Marks as well.

How long does it take to raise a pig?

Since my views on Mastering the Market Cycle can be expressed in relatively little space, I’m using the greater space allowed me in these pages to explore ideas about why business and market cycles exist at all. The current fashion is to blame human behavior, which we'll all admit is imperfect. Marks writes, “The tendency of people to go to excess will never end. And thus, since those excesses eventually have to correct, neither will the occurrence of cycles.” In this vein, behavioral economics and behavioral finance are today’s hot topics, using irrationality to explain what the economist’s traditional assumption of rationality cannot.

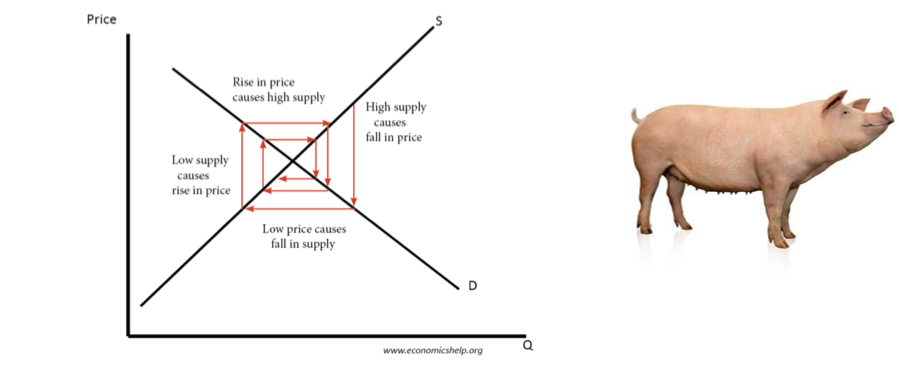

Or can it? There’s an old and entertaining trope in economics called “cobweb theory,” named after the shape of a diagram showing the progression of prices in agriculture. Exhibit 1 is a simple example:

Exhibit 1

Cobweb theory: Changes in the price of an agricultural product over time

The cobweb in Exhibit 1 results from farmers facing uncertainty about future outcomes, in this case the future price of a pig. Under such circumstances, “mispricing” the pig, with over- and undershooting of both the price and the number of pigs produced, is perfectly rational. It results from having incomplete information about the future value of the pig. This concept originates with the early 20th century agricultural economist Mordecai Ezekiel.1

First, the farmer faces a price signal (high prices) telling him to raise more pigs, so he does so. But it takes a long time to raise a pig. Meanwhile, other farmers, receiving the same signal, have also increased their pig production. By the time the pig is ready for market, there are too many pigs and the price falls. In the next round, farmers interpret the new low price of pigs as a signal to cut back on production. This causes an eventual price increase and a pig shortage. And so on ad infinitum.

Cobweb theory and value investing

What I’ve shown in Exhibit 1 is a converging cobweb. Financial asset prices tend to converge on fundamental value in much the same way; if they do so reliably, then value investing is a mechanical matter of identifying mispriced assets and waiting for the cobweb phenomenon to unfold.

But value investing is not that simple, and a “good deal” can become a “better deal.” And cobweb theory, in fact, allows for this possibility. The cobweb can diverge, with P and Q getting further away from fundamental value over time. (This happens if the supply curve is more elastic than the demand curve at the point where they intersect.)

Thus, under certain circumstances, cobweb theory predicts bubbles and crashes – without invoking irrational exuberance, animal spirits, irrational discouragement, or alternating cycles of greed and fear. Bubbles and crashes are just caused by incomplete information about the future. And cobweb theory can be applied pretty broadly, since most information about the future is incomplete. 2

Toward the end of this article, I propose that the irrationality that Howard Marks blames (or credits) for market cycles is not needed to explain the fact that cycles exist. They can be explained and predicted by an extension of cobweb theory, which doesn’t involve irrationality, only incomplete information. This simplifies matters a great deal because market cycles can then be seen as a natural consequence of agents responding to institutional incentives; one then merely has to observe this process (as revealed by market prices), instead of guessing what is in people’s heads. But Marks’ emphasis on investor psychology is useful and intuitive nonetheless.

The psychology of market extremes: Euphoria and despair

Now, back to the book. Marks possesses a wealth of practical knowledge about markets, ranging from public and private equities to bonds to distressed debt to real estate. Few readers are going to implement this knowledge directly. Instead, Marks’ gift to his readers is to emphasize the fact that moods – euphoria and despair – can identify market tops and bottoms.

These moods foreshadow bad performance when euphoria prevails, and good performance when the mood is desperate: the exact opposite of what the crowd is expecting. If you can see yourself in his description of euphoric or despairing investors, then you have enough self-awareness to benefit from Marks’ insights and, if you trade against your instinct, perhaps tip the odds to your side, as the subtitle of his book (“Getting the Odds on your Side”) implies.

Misperceptions of risk

The moods Marks describes have less to do with price than they do with risk. Market euphoria is defined by the feeling that there is little or no risk; the future is bountiful and corporate profits will grow at high rates forever. When this is the prevailing sentiment, Marks advises, sell! A near-unanimity of opinion that markets are not risky means they are, because everyone who is likely to buy the asset under consideration already has. When some sort of perturbation or tipping point occurs, there will be a flood of sellers and no buyers until the price falls dramatically, where a new equilibrium (matching buyers and sellers) is reached.

The same principle applies to despair but taking advantage of it is even harder. When almost everyone is despairing of the future, thinking it is unimaginably risky, a rational investor should buy as much as she can. It is, however, extremely difficult to do so, because the investor has typically already lost a lot of money and wants to (or has to) protect herself from losing even more.

That is when a plucky buyer can make a lot of money. Of course, she has to be prepared to lose some more money first, as when the S&P 500 achieved a double bottom: first in November 2008 (752.44) and then again in March 2009 (676.53). It subsequently doubled and then doubled again.

Marks is amused – and heartened when thinking about taking advantage of market opportunity – by the observation that market sentiment goes to such irrational extremes. “That’s one of the crazy things,” Marks says. He continues,

In the real world, things generally fluctuate between “pretty good” and “not so hot.” But in the world of investing, perception often swings from “flawless” to “hopeless.” The pendulum careens from one extreme to the other, spending almost no time at “the happy medium” and rather little in the range of reasonableness.

Memory is subject to exponential decay

The euphoria-despair cycle described by Marks arises from memory being subject to exponential decay. People place way too much emphasis on recent events. Behavioral scientists call this “recency bias.” It means that, in forming expectations, the large recent rise in prices that is remembered toward the end of a bull market (in any asset class) overwhelms memories of earlier declines. The result is a feeling that nothing can go wrong and that one should be 100% invested in, say, equities (or risky credit) forever. The consequences are, of course, high prices for everything. The bear market follows when, for whatever catalytic reason, the mood turns sour and asset owners stampede for the exits.

Hyman Minsky on how institutions contribute to market extremes

It’s time for another meditation on cycles, this time based on the work of the late unorthodox economist Hyman Minsky, a professor at Bard College celebrated posthumously for predicting the financial crisis of 2007-2009.3 He did so by observing the structure of institutions such as banks, and seeing how their executives and employees responded to the incentives with which they had been provided. Many economists have said that “people respond to incentives” are the four most important words in economics, although the expression is most closely associated with Steven Landsburg, author of The Armchair Economist.4

While Marks’ understanding of the market cycle draws on mainstream behavioral finance – it is a mark of progress that we can now call behavioral economics and finance “mainstream” – it is even more closely allied with the unique behavioral institutionalism of Minsky. Most behaviorists focus on the irrationality of individuals, but Minsky was mostly concerned with banks.

I bring this up because Marks’ career has been primarily in the credit markets, which arise from bank lending as well as other capital sources. Marks was a true pioneer in this territory, buying high-yield (“junk”) bonds and distressed debt at a time, in the late 1970s, when few other investors knew or cared about those cryptic asset classes. They are mainstream portfolio holdings now.

Thus, whether Marks knows it or not (he doesn’t mention Minsky’s name), he’s a Minskyian, relying on the by-now familiar concept of “Minsky moments” to provide the extremes of valuation and sentiment on which his cyclical investment strategy relies. A Minsky moment, in the professor’s own words, is when, “over periods of prolonged prosperity, the economy transits from financial relations that make for a stable system to financial relations that make for an unstable system.”5 That’s when you sell; you buy when the transition reverses, at low market prices.

The most basic cycle: Credit

Following the above logic, Marks observes that banks are eager to lend when they should be reluctant, and reluctant when they should be eager. This sounds a lot like investors who faced the double bottom in the S&P, and produces the credit cycle on which Marks has principally depended for making money for his clients (and himself) throughout his career.

The reason banks are eager to lend at the top of a credit cycle is that the low-hanging fruit has already been picked: loans to sound, well-managed businesses have already been generously made and these businesses don’t want to borrow any more money. So, to continue to build their asset base and look good to shareholders, banks lower their lending standards. This is all well and good until the borrowers stop repaying, which (you know this already) is why the banks should not have been so eager to lend.

The behavioral extremes that Marks (and Minsky) attribute to banks also apply to “non-bank banks,” that is, other capital providers. These include investment banks, hedge funds, private equity funds, mortgage companies, mutual funds, and ultimately end-user investors.6 No one in this long list of institutional bad actors is immune from the euphoria-desperation cycle, so there is no countervailing force preventing the cycle from getting out of hand.

Until there is a countervailing force. In the credit crunch of 1990, Marks himself was it. He writes:

[T]he market for sub-investment grade debt collapsed in the first of the three major crises Bruce [Karsh] and I have worked through together. In addition to creative the low purchase prices that made our 1990 funds above-average gainers, this episode was highly educational, as it gave us our first glimpse of the process through which superior opportunities arise in distressed debt.

Marks’ sober writing style masks the drama of that period, in which considerable fortunes were lost and made, although it was nothing like 2008, the biggest credit crisis (and opportunity) since the Great Depression.

Weaknesses of the book

If I have a substantive criticism of Marks’ book, it’s that it goes into a lot of detail on issues that are unlikely to benefit readers who are at the retail-investor level for whom much of the book is written. For example, his extensive treatment of junk bonds, the topic on which Marks is most expert, might lead some readers to think that they, too, can master the junk-bond cycle – or, a little less ominously, buy-and-hold junk bonds. Actually, casual investors have no business buying junk bonds, although a smidgen of one’s assets in a high-yield (junk) bond fund is unlikely to do much harm.

The book is a riff on Sir John Templeton’s aphorism, “To buy when others are despondently selling and to sell when others are greedily buying requires the greatest fortitude and pays the greatest reward.” If you can do that, you’ll beat the market almost every time. The miserable track record of both individual investors and the average institutional investor suggests that you can’t do that, unless you are really, really exceptional.

Do cycles exist?

Marks’ book is structured so tightly around the idea of cycles (the word “cycle” appears in 16 of 18 chapter titles) that it verges on being a gimmick. In a Wall Street Journal review of Mastering the Market Cycle, Burton Malkiel, the legendary author of A Random Walk Down Wall Street, writes: “Mr. Marks acknowledges that there are no real cycles in the market.” Has Marks written a 323-page book about cycles that don’t actually exist?

Of course not! They do exist. Malkiel is exaggerating. What Marks is saying is: unlike cycles in the physical sciences, where, as Darwin said, “this planet has gone cycling on according to the fixed law of gravity,” you can’t predict how far market cycles will go or when they will turn. You also don’t know where you are in the cycle. You can predict eclipses a thousand years ahead, but you can’t predict GDP or market prices for the next quarter. Precise physical cycles don’t exist in markets. Economics is animal behavior, not physics, and there are no exact answers.

While fully predictable cycles in markets don’t exist, there is no doubt in my mind that the euphoria-despair cycle does exist. It does not have a known periodicity or intensity, but it’s real. What Marks calls the “pendulum of investor psychology” does swing between almost universal optimism (with a few voices in the wilderness crying, to deaf ears, “Sell! Sell!”) and almost universal pessimism (when Time Magazine prints a bear on the cover and a few brave souls whisper “Buy”). And profits can be made from knowledge of these tendencies by investors with the right combination of guts, patience, and liquidity.

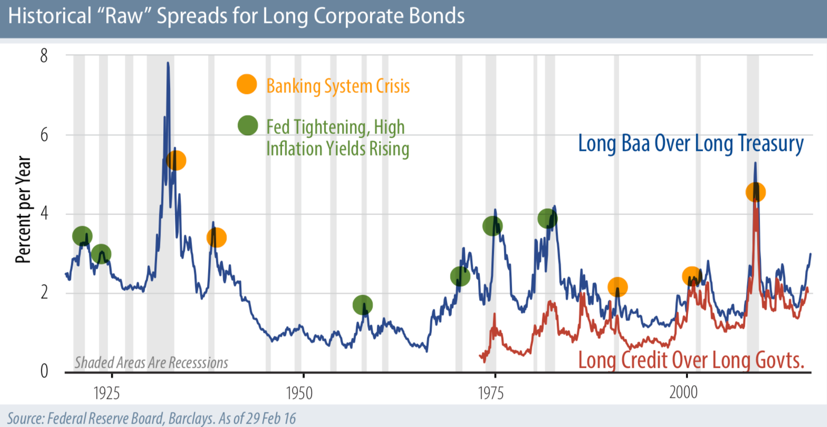

At any rate, corporate bond spreads, the metric most important to Marks’ success, fluctuate a lot, enough to tempt anyone with the inclination to look for regularities in markets. Exhibit 2 shows their very long-run fluctuations. They may not fit everyone’s conception of a “cycle” – it’s not the solar cycle, where sunspots and auroras peak every 11 years, every time – but there sure were a lot of profit and loss opportunities in this market, as in equities, real estate, and most other markets, over the last 100 years.

Exhibit 2

Yield spreads of long-term corporate bonds over Treasuries, 1919-2016

Source: using Federal Reserve Board and Barclays data.

This section is highly speculative: A cobweb theory of security prices

Like many economists, I don’t like to rely on investor irrationality to explain observed phenomena if there’s a rational explanation. How is it possible, as I speculated at the outset, that markets can provide the extremes of high and low prices on which Howard Marks relies for his cyclical investing without investors being irrational?

The idea of “rational expectations with limited information” is one possible way. In a recent lecture,7 Jonas Dovern at the University of Heidelberg exposited this idea, which I regard as an extension of the cobweb theory of our pig man, Ezekiel. Dovern applied the limited-information variant of rational expectations to the macroeconomy, but I’ll apply it to securities prices.

Cobweb theory is just rational expectations with limited information – about future pig prices and quantities. In the pig market, producers have to decide how much to produce without knowing the future price at which they’ll be able to sell it. That’s why they over- or under-produce. This is loosely analogous to the situation in securities markets, where “producers” (primary or secondary-market sellers) of securities cannot observe fundamental values or future prices, only current market prices. Thus, they possess profoundly incomplete information about what’s important for decision-making. So do buyers.

Moreover, let’s assume investors think their opportunity cost of capital or hurdle rate (hereafter “COC”) is the riskless bond yield; that is, they think the next-best alternative to holding risky assets is holding riskless ones. This isn’t strictly correct (again, incomplete information, not irrationality) but if people believe it’s correct you get the following result:

- At low prices, people perceive their expected rate of return on risky assets (hereafter “ROR”) to be higher than the COC. So they buy.

- They keep doing so as prices rise and the ROR falls until they pass through the point where the ROR equals the COC.

- However, they don’t know they’ve passed through this point because they can’t observe the ROR, or even make a close guess of it: again, incomplete information.

- As equity prices rise to high levels, eventually the ROR is obviously so much lower than the COC – maybe ROR is even negative – that buyers become sellers and you have a point of inflection and a panic or bear market.

The same applies to credit, real estate, and so forth.8

Note that I haven’t invoked irrationality or any psychological factor, only incomplete information about what the expected rate of return and opportunity cost of capital are.

Since I admitted that this section is highly speculative, I welcome critiques from macroeconomists and anyone else who thinks they can find the flaw in my argument.

If irrationality is not needed to explain market cycles, let’s not invoke it. Maybe cobweb theory, as I’ve applied it to securities markets, is enough.

Conclusion

I hope you remember, from your high school days, Rudyard Kipling’s inspiring (if slightly corny by today’s standards) verse:9

If you can keep your head when all about you

Are losing theirs…

…Yours is the Earth and everything that’s in it…

That’s Howard Marks’ advice in a nutshell. It is worth trying to follow. It’s just much more difficult to do, especially with your own hard-earned money that you hate to part with, than it is to express in poetry.

Larry Siegel is the Gary P. Brinson Director of Research for the CFA Research Foundation and an independent consultant. Prior to that, he was director of research in the investment division of the Ford Foundation. He is a member of the editorial boards of The Journal of Portfolio Management and The Journal of Investing and serves on the board of directors and program committee of the Q Group. He may be reached at [email protected].

1 Ezekiel, Mordecai. 1938. “The Cobweb Theorem.” Quarterly Journal of Economics, Vol. 52, No. 2 (February), pp. 255-280. He wrote about it as early as 1925. The better-known Nicholas Kaldor also addressed cobweb theory.

2 More fully, the cycles are caused by the passage of time as well as the existence of uncertainty (incomplete information about the future). A common definition of finance is that it is the branch of economics that deals with time and uncertainty.

3 For more on Minsky, see my review, entitled “What Would Minsky Do Now,” of L. Randall Wray’s book Why Minsky Matters.

4 Landsburg, Steven E. 1993 [2012]. The Armchair Economist: Economics And Everyday Life. Second edition (2012), New York: Free Press.

5 Minsky, Hyman P. 1972. “The Financial Instability Hypothesis” Levy Economics Institute of Bard College (May),” pp. 7-8

6 The catch-all category of end-user investors (these are, of course, the true capital providers) includes pension funds, endowments and foundations, sovereign wealth funds, and individuals. But they are not always the decision makers, except in extremis when they hire and fire managers.

7 Dovern, Jonas. 2018. “The History of Expectations in Macroeconomics” (February 12).

8 Note that this scenario is very much akin to classical business cycle theory where the economy grows until input costs become too high for companies to make a profit, then they start laying off people and not buying resources until input costs become so low as to make investment profitable, sparking another boom. Cobweb theory for the real economy, based on incomplete information.

9 Rudyard Kipling. 1895 [1910]. “If —.” In Rewards and Fairies (1910)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All