Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article originally appeared on ETF.COM here.

As the chief research officer for Buckingham Strategic Wealth and the BAM Alliance, I receive many questions from advisors and investors regarding concerns about factor-based investment strategies. A brief background on factor-based investing is helpful before discussing those concerns.

William Sharpe, Jack Treynor, John Lintner and Jan Mossin are typically given most of the credit for introducing the first formal asset pricing model – the capital asset pricing model (CAPM). It was important because it provided the first precise definition of risk and how it drives expected returns.

The CAPM looks at returns through a “one actor” lens, meaning the risk and return of a portfolio is determined only by its exposure to market beta. In the 1993 publication of the study “Common Risk Factors in the Returns on Stocks and Bonds,” Eugene Fama and Kenneth French proposed a new asset pricing model, which became known as the “Fama-French three-factor model.” This model proposes that, in addition to the market beta factor, exposure to the factors of size and value further explain the cross section of expected stock returns.

The authors demonstrated that we live not in a one-factor world but in a three-factor world. They showed how the risk and expected return of a portfolio is explained by not only its exposure to market beta but by its exposure to the size (small stocks) and price (stocks with low prices relative to book value, or value stocks) factors.

Fama and French hypothesized that, while small-cap and value stocks have higher market betas (more equity-type risk), they also contain additional unique risks (they are not free lunches) unrelated to market beta. The Fama-French three-factor model improved the explanatory power from about two-thirds of the differences in returns between diversified portfolios to more than 90%.

The Fama-French model became the workhorse model for financial economists. The fund family Dimensional Fund Advisors (Fama and French led their research efforts) led the way in introducing factor-based funds based on the Fama-French research. (Full disclosure: My firm, Buckingham Strategic Wealth, recommends Dimensional funds in constructing client portfolios.)

Today, while hundreds of factors have been identified in the literature, only a few are generally accepted as adding incremental explanatory power. And while there is some competition as to which is the best model, the most accepted four- and five-factor models include some combination of market beta, size, value, momentum, profitability and investment.

With that background, we’ll now examine three concerns that are often raised about factor-based investing. The first is that factor-based investing is complex.

Factors introduce complexity

An objection often raised is that factor-based investing introduces complexity. The increase in complexity refers to the increase in the number of funds needed to build a portfolio. Investors in total stock market funds need only two equity funds. For example, they could invest in the Vanguard Total Stock Market ETF (VTI) and the Vanguard Total International Stock ETF (VXUS).

However, investors can also build global factor-based portfolios with just two funds. For example, the “Larry Portfolio,” highly tilted to small and value stocks, requires only two funds. Personally, I use the Bridgeway Omni Small-Cap Value Fund (BOSVX, or BOTSX for taxable accounts) for U.S. exposure, and the DFA World ex-U.S. Targeted Value Fund (DWUSX) for international exposure.

Of course, there are many other choices that don’t require the use of more than a few funds. As just one example, Goldman Sachs recently introduced a suite of what they call “active beta ETFs” (Goldman Sachs ActiveBeta), which provide exposure to four factors: value, momentum, quality and low volatility.

For example, you could build a global portfolio using these three ActiveBeta funds: the Goldman Sachs ActiveBeta U.S. Large Cap Equity ETF (GSLC), the Goldman Sachs ActiveBeta International Equity ETF (GSIE) and the Goldman Sachs ActiveBeta Emerging Markets Equity ETF (GEM).

If you wanted more small exposure, you could add the Goldman Sachs ActiveBeta U.S. Small Cap Equity ETF (GSSC). Or you could use two of Dimensional Fund Advisors’ (DFA) funds: either its U.S. Core Equity 1 (DFEOX) or its U.S. Core Equity 2 (DFQTX), and its World ex-U.S. Core Equity Portfolio (DFWIX).

One more point to make is that not all “complexity” is bad. There’s a quote, often attributed to Einstein (anything you attribute to him gives it credibility): “Everything should be made as simple as possible, but not simpler.” If adding one or two funds to the two total market funds adds value by diversifying sources of risk and return, then the complexity is good, not bad.

There really isn’t much difference in complexity between a portfolio of two equity funds and one with three or four. The bottom line is that building a portfolio of factor-based funds doesn’t have to be any more complex than building a portfolio of total market funds.

We now turn to the second concern often raised: A factor can provide negative returns for a long time.

Factors can lag for long periods

It is true that all factors are likely to go through long periods of underperformance. In the most recent example, the value premium was an annual average of -1.9% a year from 2009-2018, and it was 0% outside the U.S. (Data is from Ken French’s website). However, what advocates of total market funds may fail to recognize is that the same is true for the one factor in which they have concentrated all their equity risks – market beta.

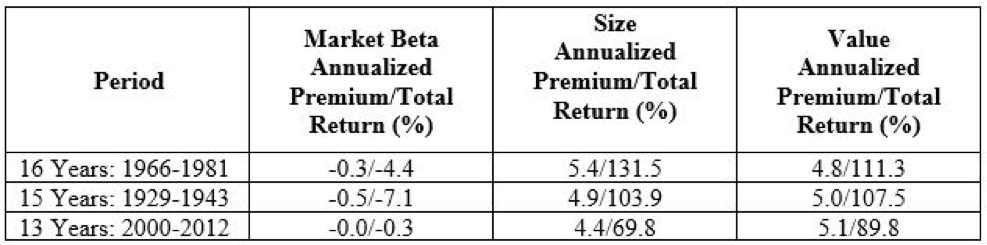

For example, we have had three periods of at least 13 years over which the S&P 500 provided no risk premium relative to riskless one-month Treasury bills. The table below shows the annualized premiums for the U.S. market beta premium as well as the annualized premiums for size and value (Fama-French research factors) over the same period. (Data is from Ken French’s website.)

The table provides some important takeaways. First, the market beta factor goes through long periods of underperformance. Second, the three periods total 44 years, or almost half the period for which we have data on U.S. stocks. Third, in each of those periods, while market beta (the U.S. stock market) did not provide any risk premium, the size and value premiums were large – the size premium averaged 4.9% and the value premium averaged 5.0%. Clearly, diversifying across factors provided significant benefits.

The problem for investors is that there are no gurus who can predict which factor will provide premiums in the future. Thus, the prudent strategy, when you don’t have a clear crystal ball, is to diversify the sources of risk and return in your portfolio.

Wise investors know that diversification means some part of your portfolio is almost always going to be underperforming. If there is never any pain, there will not be a premium. In addition, they know that diversification from the market portfolio means accepting the risk of tracking error and having to live with that pain for long periods. That’s the price you have to be willing to pay to gain the benefits of diversification (as evidenced in the table above).

We now turn to the third concern: Factor-based strategies are more expensive.

Factor-based strategies pricier

While the statement is true in a relative sense, factor-based strategies do not have to come with high expense ratios. For example, the expense ratios of the aforementioned DFA core strategies range from 0.19% to 0.23% for the domestic funds (DFEOX and DFQTX, respectively), and 0.39% for their international core fund (DFWIX).

Vanguard’s U.S. Multifactor Fund Admiral Shares (VFMFX) has an expense ratio of just 0.18%, while the Goldman Sachs ActiveBeta U.S. Large Cap Equity ETF (GSLC) costs just 0.9% (its international fund costs 0.25% and its emerging markets fund costs 0.45%). And today there are many low-cost, factor-based ETFs from which individuals can choose. Factor-based investing needn’t be expensive.

That said, expense ratios should not be the only consideration when choosing a fund, except if choosing between two index funds based on the same index.

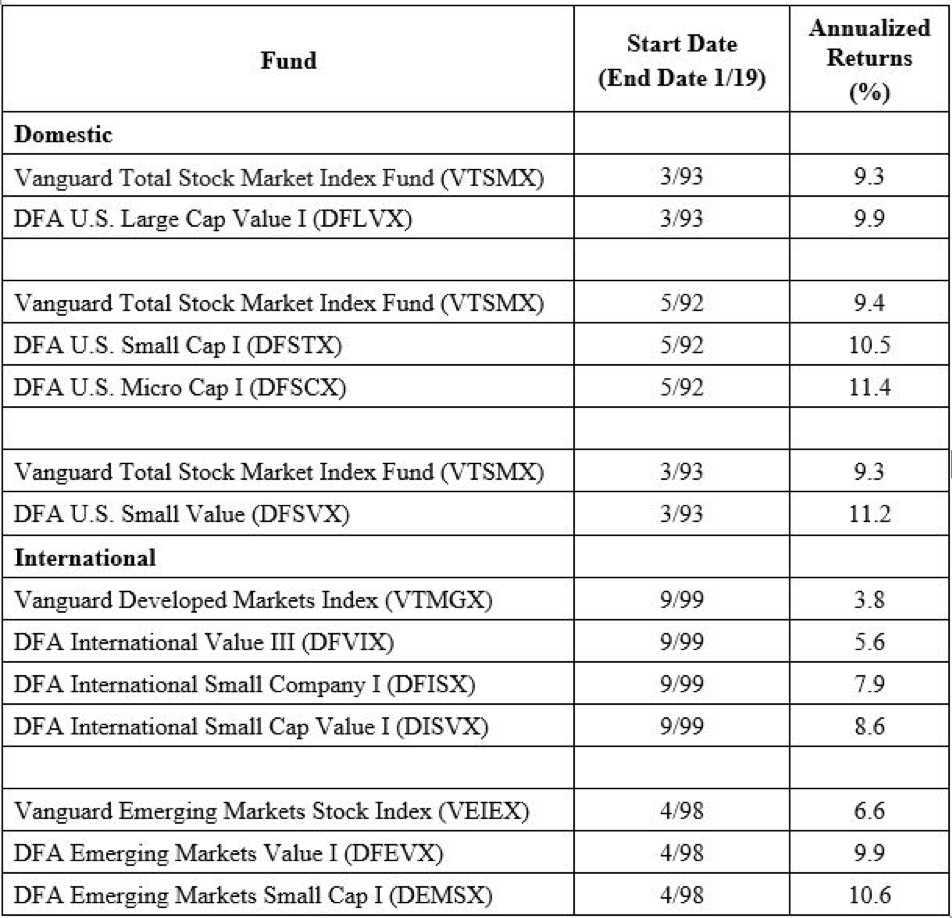

To demonstrate this point, we’ll examine the live returns of the factor-based funds with the longest track record, those of Dimensional, and compare their returns with those of the marketlike portfolios of the premier provider of index-based strategies, Vanguard.

We’ll look at data for the longest period that both the factor-based fund of Dimensional and the total market fund of Vanguard have been available. Using live funds allows us to account for fund expenses and trading costs. Data is from Portfolio Visualizer.

In each of the nine cases, the factor-based fund run by Dimensional outperformed the Vanguard total market fund, with the outperformance ranging from 0.6 percentage point to as much as 4.8 percentage points.

Despite the higher fund expenses, both in terms of expense ratios and trading costs (due to higher turnover and trading in less liquid small stocks), the nine Dimensional funds produced an average outperformance of 2.6 percentage points. Even if factor-based investing were to add a small amount of complexity, it’s safe to conclude most investors would find the complexity more than compensated for by the added return as well as the demonstrated diversification benefits.

One other point to consider is that, by increasing exposures to factors that have expected premiums, investors can lower their exposure to market beta because the equities they hold have higher expected returns than the market. That allows them to hold more safe bonds. And by purchasing individual Treasuries directly or CDs, investors can eliminate the costs of a fund manager.

The savings reduce the impact of the higher costs of factor-based funds. In other words, you have to consider the total portfolio’s implementation costs and not look at the expense ratios of the funds used in isolation.

Summary

As you have seen, well-designed factor-based strategies, which focus on the factors that have provided evidence of persistence, pervasiveness, robustness to various definitions and survive transactions costs, while also having intuitive explanations for why their premiums should persist, have historically provided higher returns than market-based strategies. In addition, they have provided significant diversification benefits, performing well over the three long periods when market beta provided no risk premium at all.

In addition, factor-based strategies do not require a great increase in complexity, as we now have many multifactor funds that can be used to develop globally diversified portfolios. And while they tend to be somewhat more expensive, they are not necessarily dramatically higher than those of market-like portfolios.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 130 independent registered investment advisors throughout the country.

More Factor-Based Investing Topics >