Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

There is simply no proof that outcomes have improved, or that risks have diminished from the proliferation of new ETF products. Instead, this has been little more than marketing to appeal to over-saturated advisors who desperately seek the next “story.”

To view the proper role that new product development should take in the context of an outcome-oriented industry, consider medicine.

Practice management consultants frequently compare investment advisors to doctors. Advisors, we are told, should conduct a thorough examination of our clients’ fiscal health, screen all possible investments, and prescribe effective investment strategies towards the objective of improving financial well-being. I too have used medical analogies and have told clients that net worth is their most important vital sign.

However well medical analogs work in communicating with clients, there is very little comparison to the way that the investment industry and the medical industry creates new products.

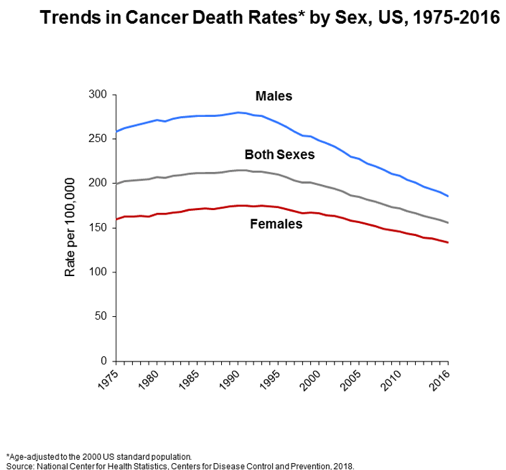

For example, cancer drugs have followed a mostly positive century-old continuum from radiation to chemotherapy to immunotherapy. At each stage not only has the treatment become more effective, it has become less invasive.

Radiation in the form of X-rays was first used in treatment in the early-20th century surprisingly soon after it was first discovered. Later, during World War II the U.S. military adapted peaceful uses of a medicinal form of mustard gas to fight lymphoma, becoming the first chemotherapy. This agent killed rapidly growing cancer cells. Then, in 1953 the structure of DNA was discovered by Watson and Crick. The medical applications were quick and revolutionary. Armed with the realization that DNA is the carrier of genetic information, doctors could make changes within patients’ cells to stimulate the immune system to fight cancer naturally. Immunotherapy was born. In recognition of this near miraculous achievement the Nobel Prize was recently awarded to two cancer immunotherapy researchers, James P. Allison and Tasuku Honjo.

All three treatments are still in use because, in some cases, radiation and chemotherapy are more effective. However, the path has been one of focused objectives with continually improved outcomes.

The bounty from these innovations is that the U.S. cancer death rate has dropped 27% in 25 years. This is a glowing testament to the power of medical innovation.

From doctors to investors

Can the investment industry claim equal success? Is product development moving along a course of more effective, less invasive? Can we assure investors that we have focused objectives with continually improved outcomes?

Look at the macro trends: the formation of the New York Stock Exchange, creation of the mutual fund, elimination of fixed commissions, advent of the index fund, or creation of the ETF, the answer is unambiguously yes. From Rothschild to Bezos, we witnessed a remarkable democratization of wealth, from an invincible 250-year-old banking family to the adopted son of a Cuban immigrant. Almost everyone on the Forbes world’s billionaires list got there from stock ownership. According to a Gallup poll, 54% of Americans own stocks. Anyone can do it. Thank you, Wall Street.

But if we narrow the lens to the last 30 years it doesn’t look as progressive. Nothing comes anywhere close to the invention of the ETF in 1993. ETFs have added $192 billion yearly in assets for 26 years. The astronomical growth of the ETF is without precedent in the investment industry or any other industry. Exchange traded funds are the most successful product of any type in history.

So far, so good. But I am not convinced that ETFs are getting better; they are just getting more numerous and soaking up more oxygen in the room. For 15 years through the last quarter the S&P 500 was up 8.57% annually, while the average ETF with a 15-year track record was up 7.44%. I am aware that mixed into these 15-year totals are ETFs that are not U.S. large blend, as is the S&P 500. However, when you compare the 145 U.S. large-blend ETFs, you see the same results – general underperformance, or merely comparable performance for every meaningful period up to 15-years.* Only 15 of 53 U.S. large-blend ETFs with a five-year track record outperformed the S&P 500. Is this innovation? Are investors benefiting? Or is this just everyone in the industry saying, “I want a piece of that $192 billion?”

The ETF industry’s response to improve this has been smart beta, a supposed improvement to mere indexing.

Smart Beta Is Not Just Marketing

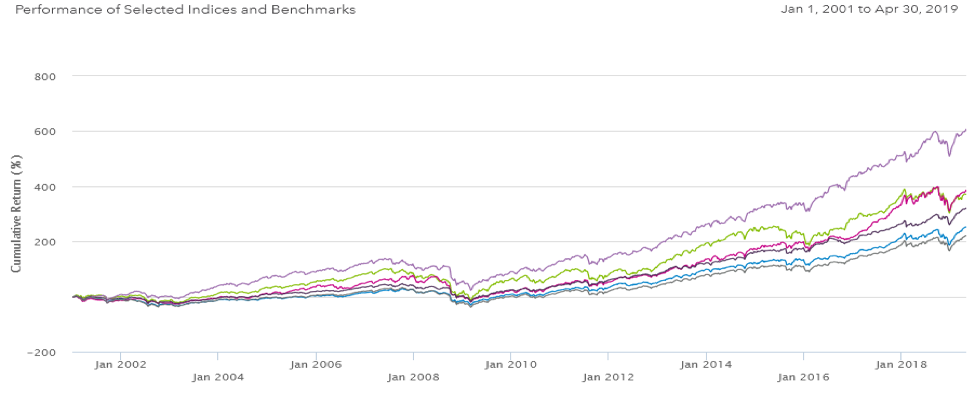

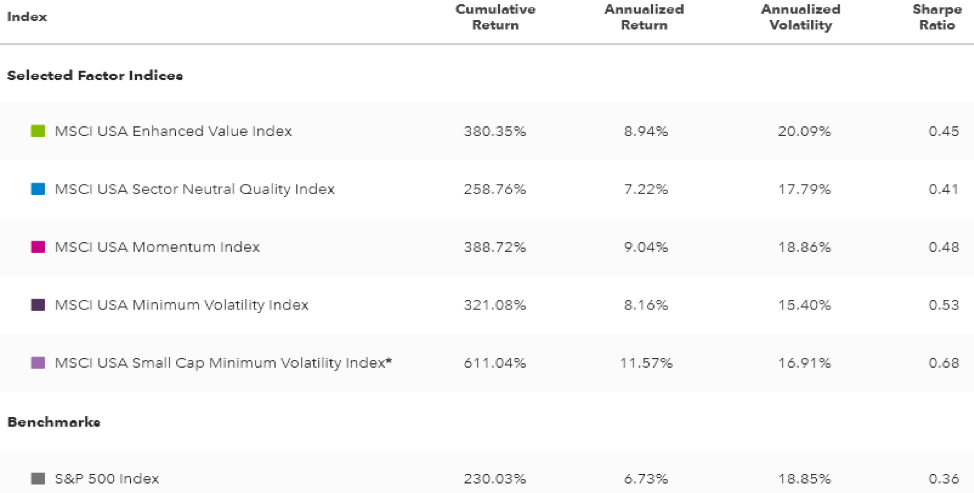

Smart beta has generally worked. By optimizing indexes, the resulting performance enhancement has been positive. Each of the factors above materially outperformed the S&P 500 for this 19-year period ending 3/31/19, according to Blackrock. But, beware, a study by Rob Arnott found, “Using past performance to forecast future performance is likely to disappoint. We find that a factor’s most recent five-year performance is negatively correlated with its subsequent five-year performance.” This is a 19-year period, not a five-year period. Even so, says the study, “By significantly extending the period of past performance used to forecast future performance, we can improve predictive ability, but the forecasts are still negatively correlated with subsequent performance: the forecast is still essentially useless!”

Sorting ETF constituents by profits, volatility, weight, momentum and various other factors, has, if not improved, at least added a productive variety to beta.

This is where the story ends.

Step right up!

Pick a prize, any prize!

After the smart beta era, ETF product development sunk to a collection of state fair arcade game prizes and bric-a-brac. Many, if not most, of the new ETFs should have never been built. If you weren’t in the ETF industry and were instead objectively trying to decide which of these stuffed animals, furry dice, hand spinners, or Moscow mule mugs to invest in your IRA, you would agree.

But since we are in the industry, we’re good at describing the benefits of investing in something that is three-times riskier than an already risky stock market (leveraged ETFs.) We sound believable when we describe the benefits of a magic trading vehicle that is easier to steal than profit from (bitcoin ETFs.) We make perfect sense when we explain the investment strategy that is either a seat belt that might work, or a rocket that might boost you into orbit (130-30 ETFs.) Everyone believes us when we claim that what made us relish Pink Floyd’s Pulse tour in 1994 would also make a terrific investment in our daughter’s custodial account (marijuana ETFs.) These are just some of the prizes on the midway. Additionally, there are millennial anything, blockchain anything, China anything, and my idea is better than your idea anything ETFs. You get the picture.

These are push them in the direction they are leaning ETFs because, yes, even you can find people who love pot, crypto, muddled investment strategies, and excessive leverage. Does that mean we have to build investments out of them? Is push them in the direction they are leaning the new fiduciary standard?

How did this happen? This was the objection that John Bogle had when we called investments “products.” The commodification of investment management distorted the way we manage money, according to Bogle. He spoke approvingly of Judge Robert Healy, SEC Commissioner, who said that SEC Commissioners, “were anxious to protect the fund investor from the distorting impact of sales. Products designed for their appeal to the market did not, and do not, necessarily make the best investments.” That Judge Healy was an author of the Investment Company Act of 1940, and ETFs are mostly ’40 Act Funds, is a rich irony.

I won’t attack any ETF company by name, but one company (there are many like this) that has brought out numerous ETFs boasts this track record: an average two-star rating by Morningstar, higher than average net expense ratios, and aggregate underperformance of the S&P 500 overall for three-, five-, and 10-year periods. The S&P 500 has roughed up many of us since 2009, but I see so few examples of outperformance with each new ticker that I have to ask why we keep adding more and more.

More is less

To try to understand these dynamics, I ran two informal unscientific polls on Twitter that asked the following questions:

- In 1980 there were 560 mutual funds (source: John Bogle). Today there are 27,481 mutual funds (source: Morningstar, all share classes).

Do we need more mutual funds?

Responses, 8% YES, 92% NO.

- According to @etfgi there were 123 ETFs in 2003, and by March of 2019 there were 2,012 ETFs in the U.S.

Do we need more ETFs?

Responses, 54% YES, 46% NO.

Conclusion: 27,000 is too many mutual funds, yet 2,000 is not enough ETFs. Supply is driven by industry, not investor demand. The fact that 35% of all ETFs have less than $30 million AUM is proof.

Does it solve one of these six problems?

Am I being unfair to the ETF industry? To circle back to my original comparison, I will ask again: Are healthcare’s aims nobler than the investment industry’s? Healthcare is more outcome-based than the investment industry; statistics back this claim. Thus, my proposal to the investment industry is to stop, reflect, and, moving forward, filter any proposed new ETF issue through these six screens:

-

Lower cost. Are you bringing to market a name in a category that is materially less expensive than your competitors? Granite Shares, for example, attacked an expensive asset category – commodities – and is winning. Investors are better off for it.

-

Hard-to-invest markets. Emerging markets, commodities, and senior loans, as examples, are difficult to invest in for retail investors. ETFs make it much easier.

-

Scale prohibitive. TIPS and GNMAs, for example, are difficult to invest in for a different reason. They need size, bond desks won’t talk to small buyers, and there is a lot of “friction” or spread in the bid/ask. TIPs or GNMA ETFs overcome those hurdles.

-

Diversified. Much like a mutual fund, an ETF can provide significant diversification. Will your ETF provide diversification beyond what would be possible for investors on their own, or a type of diversification that hasn’t been available?

-

Enhanced. There are a few newer fund complexes (Delta Shares and Innovator ETFs) that brought to market ETFs much like structured notes that, if not guaranteed, offer some level of protection in a down market. There is a lot of room for growth in this category. Likewise, there are other fund companies that offer currency hedges in developed markets. These are an investable value-add.

-

Certainty. Invesco (formerly Guggenheim) Bullet Shares are a good example by providing ETFs that have a set “defined” maturity date. They offer the diversification of a bond fund with the certainty of a due date. They are more liquid and less expensive than a UIT; it will be hard to imagine not seeing growth in this space.

If your proposed ETF competes in at least one of these categories, proceed. If not?

There is one category missing from my list – the one in which you should be most interested: the great idea category. I can’t give any guidance here. These are more art than science – or, in many cases, more fiction than science. They are demographic storm chasers for the first born’s of the world. Online retail, hacking, semiconductor this, internet that, there is even a benighted bitcoin offering on the five years ago you should have list. I can’t help you get in on it, and I can’t keep those on it, off it. Some are staggeringly successful; most are not. Perhaps that is the profile of the aggressive investment. No serious investment company can build only these and serve investors at the same time. One fund company in this category has on average for all its ETFs negative six-month, 12-month, three-year, five-year, and 10-year returns in the longest bull market in history. Those are clearly not “improved outcomes.”

Innovation is not a ticker symbol

Innovation doesn’t start with a product. It starts with an idea. There are no innovative products – only innovative ideas. Rob Arnott didn’t start with a clever ticker symbol and work back. He started with a question – something like “what would happen if we built an index that was weighted by company profitability, instead of asset size?” The answer to that question was the invention of smart beta. Will Rhind asked, what if we could attack the real assets space with more reasonable pricing? What benefit could that bring investors? We must start with questions like these, or we might as well start guessing peoples’ weight and selling cotton candy.

Perhaps your favorite program is Deadliest Catch. I love it too, so I can relate. I know you met its protagonist, Sig Hansen, by accident in Seattle on your 20th wedding anniversary trip with your wife. And I know you asked him to give you all the bait, diesel fuel, tackle, sonar equipment, life jacket, and gaff hook brands he uses, so you could smartly identify the publicly traded companies that sell them. And, I agree, DEAD is an awesome ticker symbol, and yes it really fits. But please don’t build that ETF.

Buy a bass boat instead? It will be a lot cheaper for all of us.

*US Large Blend ETFs (“Average”) vs S&P 500. 15 years through 3/31/19. 145 ETFs total, source: Morningstar, Inc.

Andy Martin is co-founder and president of 7Twelve Advisors, LLC, creator of 3Twelve Total Bond, and author of Dollarlogic: A Six-Day Plan to Achieving Higher Returns by Conquering Risk, foreword by Arthur B Laffer, Ph.D. Nothing here should be construed as investment advice or a recommendation for any company, ETF, or investment strategy.

More Factor-Based Investing Topics >

Pick a prize, any prize!

Pick a prize, any prize!