Is the Shift to Passive Investing Increasing Risks?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEarlier this year, passive management was attacked in two high-profile articles. Those criticisms were proven to be false – and driven by active managers seeking to protect their livelihoods. But that still left the question, which I now examine, of whether flows to passive funds have increased certain risks.

The active management industry has ridiculed passive investing for decades. The reason is that their profits – and their very survival – is at stake. The criticism reached an absurd level when a team at Sanford C. Bernstein called passive investing “worse than Marxism.” The authors of the note wrote: “A supposedly capitalist economy where the only investment is passive is worse than either a centrally planned economy or an economy with active market led capital management.”

Another example of such criticism is the article “What They Don’t Tell You About Passive Investing.” The thrust of that Morgan Stanley paper was that “the exodus from active to passive funds may be reaching bubble-like proportions, driven by an exaggerated critique of active management.”

The basic argument of those and other critiques is that the popularity of indexing/passive investing is distorting prices as fewer shares are traded by active investors performing the act of “price discovery.” Each of those critiques is fallacious.

That said, it’s possible that the trend to passive investing has increased some financial risks.

To determine if that is the case, Kenechukwu Anadu, Mathias Kruttli, Patrick McCabe and Chaehee Shin (all from the Federal Reserve), authors of the September 2019 study “The Shift From Active to Passive Investing: Potential Risks to Financial Stability?” examined how this shift affects financial stability through its impacts on funds’ liquidity and redemption risks, asset-market volatility, asset-management industry concentration, and co-movement of asset returns and liquidity.

The authors began by noting: “The shift to passive investing is a global phenomenon. In the U.S. … the shift has been especially evident among mutual funds and in the growth of exchange traded funds, which are largely passive investment vehicles. Passive funds made up 47% of the AUM in equity funds and 27% for bond funds at the end of 2018, whereas both shares were less than five% in 1995. Similar shifts to passive management appear to be occurring in other types of investments and vehicles. For example, the share of assets under management in university endowments and foundations invested in passive vehicles has reportedly increased substantially in recent years.” They added: “The shift to passive investing is also occurring in other countries.” Following is a summary of their findings:

- The growth of exchange-traded funds (ETFs), largely passive vehicles that do not redeem in cash, has likely reduced risks arising from liquidity transformation in investment vehicles.

- Investor flows for passive mutual funds are less reactive to fund performance than the flows of active funds. The result is that passive funds face a lower risk of destabilizing redemptions in episodes of financial stress. For example, in charting the cumulative flows for equity funds from December 2007 through mid-2009, and the cumulative flows for bond funds during the “Taper Tantrum” in mid-2013, passive funds had cumulative inflows and active funds had cumulative outflows in both cases.

- Passive mutual funds are less likely than active funds to hold highly illiquid assets – holdings of highly illiquid assets can create severe liquidity risks for funds that offer daily redemptions.

- Leveraged and inverse ETFs, which seek daily returns that are respectively positive and negative multiples of an underlying index return, must both trade in the same direction as the market moved earlier in the day. Thus, they must buy assets (or exposures via swaps or futures) on days when asset prices rise and sell when the market is down, amplifying market volatility.

- Since passive funds use indexed-investing strategies, these funds’ growth could contribute to “index-inclusion” effects on assets that are members of indexes, such as greater co-movement of returns and liquidity. They added that the research found that the effects of index inclusion had declined significantly since 2000. In addition, equity co-movement has declined significantly since 2000.

- Stocks with more ownership by ETFs display higher volatility than otherwise similar securities. The volatility arising from ETF trading induces a non-diversifiable source of risk, at least in the short term. However, while ETF trading may lead to pricing distortions for individual ETF-held securities, such trading helps move aggregate market prices closer to fundamentals.

- Research has found that passive-investor demand leads firms to issue larger bonds with lower yields, longer maturities and fewer investor protections. This suggests the shift to passive investing may be contributing to increased corporate leverage by encouraging firms to issue corporate bonds that will be included in indexes.

- The removal of assets from an index causes their prices to fall. This may affect financial stability because of the recent shift in the ratings distribution of investment-grade bonds towards triple-B, the lowest investment-grade rating. About 50% of investment-grade corporate bonds outstanding had triple-B ratings as of March 2019. In an economic downturn, widespread downgrades of these bonds could push them out of investment-grade status, rendering large numbers of bonds inappropriate as investments for investment-grade corporate bond mutual funds, leading to widespread bond sales that exacerbate any price declines due to the downgrades themselves.

- The liquidity for investment-grade bonds has declined, but it has increased for high-yield bonds.

The authors did express concern that the shift to passive vehicles has increased concentration in the asset management industry (because passive asset managers tend to be more concentrated than active ones), resulting in the growth of some very large asset management firms. They noted that this has probably exacerbated potential risks that might arise from serious operational problems at those firms. The reason is that a significant idiosyncratic event at a very large firm could lead to sudden massive redemptions from that firm’s funds and thus potentially from the asset management industry as a whole.

However, they noted: “To be sure, past instances of serious problems at asset management firms, such as the 2003 mutual fund trading scandal, do not appear to have caused aggregate problems; although redemptions from affected funds were sizable, they occurred over many months, and investors appear to have largely moved assets from scandal-tainted mutual funds to other mutual funds.” That said, they also cautioned: “An operational event, such as a cyber-security breach that immediately puts investors’ wealth at risk, plausibly could trigger more sudden redemptions, aggregate shifts out of mutual funds, and fire sales with broader financial consequences. … As such, the continued growth of very large asset management firms raises concerns about the repercussions of serious problems at those firms for financial stability.”

The authors concluded that the shift from active to passive investment is, in fact, affecting the composition of financial stability risks. However, the impact is not unidirectional; while the effect is increasing some risks, it has in fact reduced others.

Impact on price discovery

Now that we have seen that many of the one-sided claims against passive investing increasing risks are false, we can return to the main argument against the trend toward passive investing: Prices are distorted, as fewer shares are traded by investors performing the act of “price discovery.” Let’s examine the validity of that claim.

If indexing’s popularity were actually distorting prices, active managers should be cheering, not ranting against its use. It would provide them easy pickings, allowing them to outperform. (If money flowing into passive funds distorts prices, it could still make it difficult for active managers because distortions could persist as long as the flow continued. Eventually, though, the opportunity would manifest itself.)

But the rise of indexing has coincided with a dramatic fall in the percentage of active managers outperforming on a risk-adjusted basis.

The study “Conviction in Equity Investing” by Mike Sebastian and Sudhakar Attaluri, which appeared in the summer 2014 issue of The Journal of Portfolio Management, found that the percentage of skilled managers was about 20% in 1993. By 2011, it had fallen to just 1.6%. This closely matches the result of the 2010 paper “Luck versus Skill in the Cross-Section of Mutual Fund Returns.” The authors, Eugene Fama and Kenneth French, found only managers in the 98th and 99th percentiles showed evidence of statistically significant skill. On an after-tax basis, that 2% would be even lower.

In our book “The Incredible Shrinking Alpha,” Andrew Berkin and I present evidence as well as the reasons for the dramatic decrease in active investors’ outperformance on a risk-adjusted basis.

In addition to the evidence on the failure of active management to persistently generate risk-adjusted alpha, it’s easy to check whether increased flows to index funds are causing price distortions. If that were the case, then all securities in an index would be rising/falling by about the same percentages, as cash is invested based purely on market capitalization. In 2018, while the Vanguard S&P 500 Index Admiral Shares Fund (VFIAX) lost 4.4%, providing active managers with the advantage of being able to go to cash, the fund still outperformed 73% of all actively managed funds. In addition to being able to go to cash, there was a great opportunity for active managers to generate alpha through the large dispersion in returns between 2018’s best-performing and worst-performing stocks. For example, while the S&P 500 lost 4.4% for the year, including dividends, in terms of price-only returns, 10 companies were up at least 42.6%, and three more than doubled in value. The following table, with data from S&P Dow Jones Indices, shows the 10 best returners.

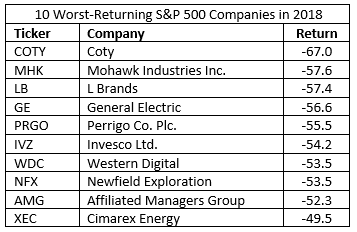

To outperform, all an active manager had to do was to overweight those big winners, each of which outperformed the index by at least 47%. On the other hand, 10 stocks lost at least 49%, with the worst performing losing 67% on a price-only basis.

To outperform, all an active manager had to do was to underweight, let alone avoid, these dogs.

This wide dispersion of returns is typical. Yet, despite the opportunity, year after year, in aggregate, active managers persistently fail to outperform. For example, over the 15-year period ending October 2, 2019, VFIAX outperformed 91% of the actively managed funds that even managed to survive the period. If survivorship bias were accounted for, the figure would be even higher, and that is before taxes. Because taxes are typically the largest expense for taxable investors, after-tax results for VFIAX would be even more favorable.

Summary

The proponents of active management will continue to attack passive investing. The reason is simple: It threatens their livelihood. Thus, their behavior should not come as a surprise. But the trend toward passive investing will continue because it is the winning strategy, providing you with the greatest odds of achieving your financial goals.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 130 independent registered investment advisors throughout the country.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All