Awareness has become widespread only recently that incomes before taxes of the bottom half – or more – of the American population have stagnated in the last 40 years, while incomes at the top rungs have soared. Now, a new book, The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay, by Emmanuel Saez and Gabriel Zucman, professors of economics at the University of California, Berkeley, shows that the divide is even greater after taxes. Taxes, they say, used to be progressive, but no longer are – because of tax rate changes over those years; payroll tax increases; and the rise of a gigantic tax avoidance and evasion industry that benefits only the wealthy. To remedy this situation, they propose – unflinchingly – a complete overhaul of not just the U.S. but the entire international tax system.

Some facts about the distribution of wealth and income before taxes

Saez’s and Zucman’s book is brimming with facts and statistics. It is what is called “wonkish” in the annals of public policy – intricate in details and numbers.

In 2019 the average income of all American adults was $75,000, while for the bottom 50% it was $18,500. This sounds low, but lower still when compared with the average cost of health care for American adults, $15,000. The next 40%, which Saez and Zucman call the “middle class,” averaged $75,000, similar to the overall average. The next 9% averaged $220,000. But it was the remaining top 1% that made up for a large part of the shortfall in the lower 50%, by averaging $1.5 million income a year.

The authors’ facts about how before-tax income among the adult population is distributed today are startling, but much more so when one realizes how that distribution has changed since 1980. Saez and Zucman say, “In 1980, the top 1% earned a bit more than 10% of the nation’s income, before government taxes and transfers, while the bottom 50% share was around 20%. Today, it’s almost the opposite: the top 1% captures more than 20% of national income and the working class [the bottom 50%] barely 12%.”

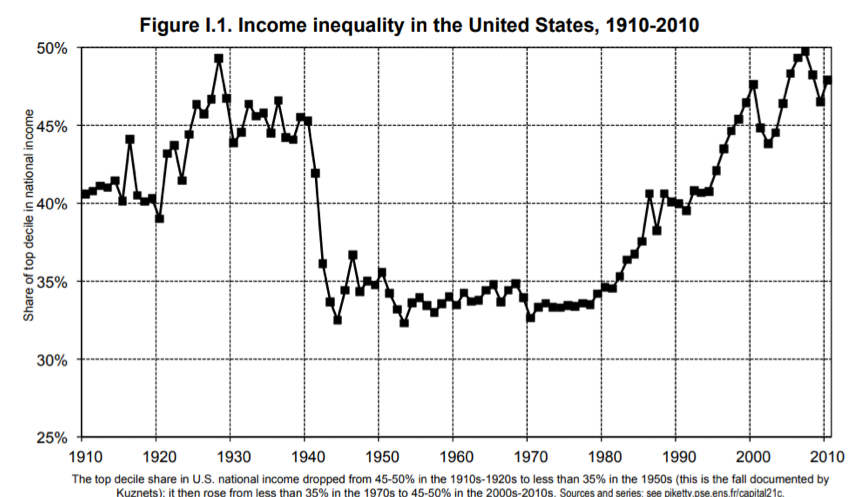

We have seen statistics like these repeated numerous times recently and in many versions. Thomas Piketty, who was Zucman’s thesis advisor, brought them to the world’s attention with the 2014 English translation of his 2013 book, Capital in the Twenty-First Century. In it, he showed how the income share of the top 10% had dropped in the United States during the years from 1945-1980, and has risen sharply since then – see graph below from Piketty’s website.

Inequality dropped precipitously during and after World War II for a variety of reasons, but Saez and Zucman attribute it in part to the quasi-confiscatory tax policies implemented under president Franklin Roosevelt, with marginal taxes on the highest incomes set above 90%. These taxes applied only to a very small fraction of taxpayers, the ultra-rich. They appear to have had the effect of discouraging those people from seeking even higher incomes, thus compressing the pre-tax income spectrum.

The express purpose of these high tax rates was, in fact, the authors say, to prevent extreme inequality: “On both sides of the Atlantic during these eras, tax policy reflected the view that extreme inequality hurts the community; that the economy works better when rent extraction is discouraged; and that unfettered markets lead to a concentration of wealth that threatens our democratic and meritocratic ideals.”

This view implies a tax policy that Saez and Zucman call, “beyond Laffer.” Arthur Laffer, as many will recall, is the economist who – according to legend – drew a curve, the Laffer curve, on a napkin at a restaurant in 1974 to show that high tax rates can actually reduce national tax receipts. Laffer argued that if tax rates get too high, people will work less, earn less income and pay less taxes.

Saez and Zucman say that the high tax rates in the uppermost brackets did reduce national tax receipts slightly. They were higher than the point on Laffer’s curve where the maximum tax receipts would be obtained. But they were deliberately set that way to prevent extreme income inequality.

How taxes in the U.S. have changed over time

The story of U.S. taxes over time is summarized in the exhibit that can be seen after opening the authors’ tax simulation tool at their website taxjusticenow.org. What one sees, scrolling down, is an animated version of the change in the progressivity of the tax curve over time, from 1950 to 2018. (The graph can also be seen in a New York Times article by David Leonhardt.)

In the most recent year, 2018, the total tax paid averaged 28% of income, and it was not progressive at all. The tax paid as a percentage of income did not, for the most part, increase with the level of income.

For the lowest income decile, the tax rate was about 28%. At higher income deciles it varied only a little and actually dropped to only 23% for the 400 highest income earners.

But looking back in time, the tax rate was much more progressive. In 1950, the tax rate was only 17% for the lowest income decile but rose to 70% for the highest. Since that time, the graph shows that the tax became less and less progressive until it reached its current almost flat profile.

Not just income tax but all the taxes

Key to understanding this graph is that Saez’s and Zucman’s numbers include all taxes paid by Americans – income taxes, payroll taxes, capital taxes, and sales taxes.

Capital taxes include not only dividends, interest, and capital gains but also the taxes that reduce shareholders’ earnings when corporations are taxed. In 1950 this was a substantial amount and was paid by capital owners, who tend to be the wealthiest citizens.

But as corporate tax rates have come down – and have been minimized by corporate practices, as we shall see, that could either be called tax evasion or tax avoidance – the tax on capital has become minimal. This, as well as other tax evasive practices, has reduced the overall tax rate for the wealthy.

Meanwhile, tax rates for the lowest levels of income earners have increased because of increases in payroll tax rates, which pay for Social Security and Medicaid.

Saez and Zucman break down the 28% total tax rate into its components: income taxes, payroll taxes, capital taxes, and consumption taxes (sales taxes and import duties).

I found their presentation confusing because the percentages presented for the various taxes are on different bases. Some, like the 28% total, are a percentage of total national income. Others, like Social Security payroll taxes, are quoted as a percentage of workers’ paychecks up to the cap of $132,700 a year in 2019. Consumption taxes are cited as a percentage of personal consumption. As a result, it was difficult to make the percentages for the taxation categories add up to the total of 28%.

The book would have benefited from a concerted effort to make these percentages compatible and to present them in an easy-to-understand way, perhaps in a pie chart, or series of pie charts.

However, here is the breakdown in the most recent year, as I understand it. Of the 28% total tax rate (total taxes divided by U.S. national income), individual income tax revenues were 11.5% of national income; payroll taxes (for Social Security and Medicare) were 8%; consumption taxes were 6% (but they are quoted in the book as a percent of total personal consumption expenditure, which is probably not the same as national income); and capital taxes were 4%. Since these add up to 29.5%, which is not too far from 28%, perhaps I have gotten them nearly right. It is not easy to glean fully comparable numbers from Saez’s and Zucman’s text.

Why the progressivity of the tax curve has disappeared: tax dodges of the rich

The progressivity of the tax curve has disappeared for two reasons: increases in payroll taxes, which hit only wage earners below the cap of $132,700; and sharp decreases in capital taxes, which reduce taxes mostly for the wealthy.

Increases in payroll taxes for Social Security were inevitable, since post-retirement life expectancies have more than doubled since 1950. Payroll taxes for Medicaid are new since then and have increased because of the increase in the cost of healthcare. There is little that can be done about these increases, other than to increase retirement age and squeeze healthcare costs.

But Saez and Zucman believe that much can be done about the sharp reduction in taxes collected from the upper wealth echelons – which means, of course, that taxes can’t be reduced for the lower echelons, since somebody has to pay them, or that national debt will continue to soar indefinitely; or both.

Capital gains taxes have, as we know, declined over recent decades. Saez and Zucman believe, as we shall see, that they should be at the same rate as taxation of income. But that is only a small part of the decline in capital taxes. The larger part is the decline in corporate taxes.

Corporate taxes have been reduced in the United States (and elsewhere) because of international tax competition, particularly from relatively small states like Ireland, Bermuda, Luxembourg, and numerous others, known as tax havens. Because of this competition, corporate taxes at the higher U.S. tax rate had become difficult to collect, because they can be dodged through the use of tax havens.

Here is how it works. Subsidiaries are set up in tax havens to hold intangible corporate properties that generate a lot of profit such as logos, patents, and know-how. Then because these intangibles are difficult to value, they are sold (transferred) by the parent to the subsidiary (or vice-versa) at tax-beneficial virtual prices. To aid in this transfer pricing, an enormous transfer pricing industry has grown since the 1990s, housed in the Big Four accounting firms and in large international corporations. Saez and Zucman say that “today, 250,000 people work as transfer pricing professionals in private firms, either in the Big Four or as direct employees of multinationals.”

The lowering of corporate taxes in response to international corporate tax competition has also increased the attractiveness of another tax-dodging practice: incorporating. Saez and Zucman say, “Teachers, clerks, and most other employees will never be able to pretend their wages are in fact dividends. But for the wealthy, shifting income is child’s play. The way this is done in practice is by incorporating.” Thus, receipts taxed at income rates become corporate profits taxed at the lower corporate rates.

The authors say that these practices should really be illegal, by dint of a taxation principle – the “economic substance doctrine” – that I’m afraid they say too little about. The economic substance doctrine, they say, makes, “illegal any transaction that has no other purpose than a reduction of tax liability.” But because this doctrine is not being enforced, corporate tax evasion has run amuck.

In a future edition of their book, the authors should include an entire chapter on this doctrine – its legal basis and history, and what it would take to enforce it. Perhaps because they are economists and not lawyers, they should recruit a lawyer to write the chapter.

In addition, both tax avoidance and outright tax evasion – as has recently been impressed upon us by the leaks from the Panamanian law firm Mossack Fonseca – have been abetted by the setting up of shell companies in tax havens. These shell companies, say Saez and Zucman, “disconnect bank accounts from their owners, creating financial opacity that makes it harder for tax authorities, investigators, and regulators to know who really owns what.” Saez and Zucman say that hundreds of thousands, perhaps millions of these shell companies have been set up worldwide.

Laborers who earn a regular wage have little means of dodging taxes because their wages are reported directly to the Internal Revenue Service. But wealthier capital-owners whose incomes are more varied and complex and less reportable can do it much more easily. This is facilitated by the fact that the IRS budget has decreased over the last decade by more than 20%, adjusted for inflation. The resources of multinational companies and wealthy individuals, in their pursuit of tax avoidance swamp those of the IRS.

The proposed remedies

After detailing all of these methods of tax avoidance, tax evasion, and their consequences, the authors present their own prescription for remedying the situation. It is not a modest proposal; nor is it as simple as the authors may have come to believe that it is, immersed as they are in its details.

They believe all tax rates should be the same, whether imposed on labor or capital, combined in a form that they call the “national income tax.” Before proposing this, they even critique the taxation regime used in most of Europe, the value-added tax or VAT. They find that wanting too. Their solution is therefore one they recommend not only for the United States but for other countries too – and one that, in fact, needs international coordination.

To discourage international tax competition and tax avoidance through the exploitation of tax havens, they propose that corporations be taxed in their aggregate rather than for each subsidiary in a different country. And they propose that nations cooperate to harmonize corporate tax rates so that international tax adventurism will no longer be profitable.

They also believe that a wealth tax is necessary. Why? Because great wealth usually generates little taxable income.

For example, they cite the case of Warren Buffett: “Warren Buffett reports a tiny amount of taxable income to the IRS compared to his true economic income. But he cannot hide the fact that he’s worth more than $50 billion. With a wealth tax at a rate of 2% on the fortunes above $50 million and 3% above $1 billion (such as the one proposed by Senator Elizabeth Warren in 2019), Buffett would pay around $1.8 billion a year, a thousand times his 2015 income tax bill of $1.8 million.”

These proposals had the effect of causing a thought bubble to form in my mind: “Dream on.”

But there is a saying that in politics, the impossible can become the inevitable without even passing through the improbable. Take, for example, the case of gay marriage.

Bold proposals have to be made if they are ever to have a chance. For better or for worse, don’t count this one out entirely.

Economist and mathematician Michael Edesess is adjunct associate professor and visiting faculty at the Hong Kong University of Science and Technology, chief investment strategist of Compendium Finance, adviser to mobile financial planning software company Plynty, and a research associate of the Edhec-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

More Innovative ETFs Topics >