The market’s response to the coronavirus had a stark effect on portfolio values. Less apparent, but more important, was how it reduced the probability that your financial plans will succeed in reaching your clients’ financial goals. Here’s an example of how devastating that may be and how you should communicate this to clients.

A retiree holding a 50/50 portfolio with an assumption of 8% arithmetic returns on stocks and 4% bond returns (with 1% asset management and investment expenses) has a 94% chance of successfully following a 3% rule withdrawal strategy over 30 years. In other words, there is a 94% probability that they can spend $30,000 at age 65 and then increase this spending amount by a 2% rate of inflation annually through the age of 95.

But, after the first day of retirement, this probability is no longer 94%. The retiree realizes a daily random return that changes the probability of success. Returns above market expectations will increase the probability of success. Returns below expectations will reduce the probability that the client will successfully be able to maintain their desired lifestyle.

These incremental changes in probabilistic goal attainment are inevitable in any portfolio that invests in assets with future uncertain payouts. It is up to an advisor to understand these changes and decide when and how to communicate their implications to a client.

Anil Suri, head of portfolio construction and investment analytics at Merrill Lynch, once used the analogy of Google maps to explain probabilistic goal attainment using stochastic portfolios. When I input my destination, I get a highly precise estimate of the arrival time based on the amount of current traffic. But Google cannot anticipate an accident that hasn’t yet occurred. Halfway to my destination I receive a course correction recommendation that gets me to my desired destination most efficiently after factoring in new information.

This analogy is important because many advisors view the original estimate of probability as overly static. When market conditions shift, they assume that if their client “stays the course” and patiently maintains their portfolio allocation and spending strategy they will be fine in the long run. After all, when developing the investment policy there was a 94% chance of success.

If the accident had occurred prior to departure, the estimated length of my trip may have been five minutes longer and would have included a different route. If retirement was guided by Google maps, a retiree facing falling interest rates and a drop in equity values at the beginning of retirement would receive a course-correction warning. The retiree will now need to spend less and perhaps invest differently in order to maintain the same probability of success.

Helping a client understand retirement investment risk

Imagine that each annual return on an investment portfolio is printed on the back of a playing card. A deck of 40 cards contain a range of portfolio returns that is roughly normally distributed. Most will be between 0 and 10%. One is positive 40%. Two are -20%. One card has a return of -30%, or about the return on a 60/40 portfolio in 2008. This is the wild (or black swan) card.

At the beginning of retirement, the dealer shuffles the deck and spreads all the cards in front of the retiree face down. The retiree then picks up cards one at a time. Each year their portfolio rises or falls by the percentage on the card. They must live with whatever sequence of returns they draw. This is the essence of investment risk in retirement.

What are the consequences of picking up the wrong card the first year of retirement? I asked David Blanchett, head of retirement research at Morningstar, to estimate how picking up various cards impacts the probability of success. This is the probability that the 65-year old client will be able to spend $30,000 plus modest inflation until age 95.

What happens if the client picks up -30% the first year of retirement? The probability of success falls from 94% to 48%. This is the equivalent of setting off on a road trip and encountering a 50-car pileup.

The original 94% figure assumes a normal distribution of possible future returns in which some random runs led to failure. It just so happens that if one of these random runs results in a -30% return the first year of retirement, the likelihood of failure is now 52%.

What’s wrong with telling a client, “if you can just stick with the original asset allocation plan, you’ll be fine?” It is tempting to believe that since the original plan had a 94% chance of success, random turbulence at the beginning of retirement is simply normal and the client just needs to stick with the plan because they’ll be fine in the long run. After all, it was stress tested using a Monte Carlo analysis with thousands of simulations.

This is wrong.

The Monte Carlo analysis only shows the probability of success at a single moment in time. Had the client retired at age 66 with 30% less in savings, she would now be following a 4.3% rule instead of a 3% rule. She’d have to accept a far greater failure rate in order to maintain the goal of spending a higher percentage of her portfolio.

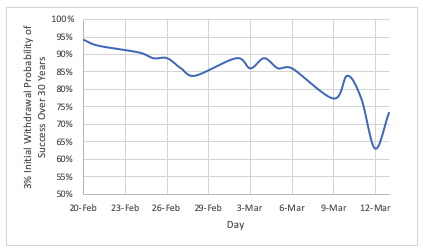

Let’s consider the impact of retirement success over a recent market decline. A 50/50 portfolio of the S&P 500 (VFINX) and a Vanguard intermediate-term corporate bond fund (VBILX) fell about 25% in the three weeks prior to March 12. How should an advisor communicate the implications of this loss? Should they simply tell their client to be patient and avoid adjusting their lifestyle expectations?

On March 12, the client experienced a drop in a retirement portfolio that decreased the probability of success from 94% to 63%. A 37% probability of failure may not be a risk that the client is willing to accept in order to withdraw the same amount from their portfolio to fund spending. If you’re driving to a wedding that starts at 2 p.m. on Saturday and the chances of getting there on time go from 94% to 63%, you’d want to have this information when planning what time to leave in the morning. Should Google maps continue to allow you to believe that leaving at 8 a.m. is fine when you now have less than a two-in-three chance of making it to the wedding on time?

This is the challenge posed by the instant availability of probability-based planning information. How should the advisor communicate the change in expectations to a client? Do they trust the client’s response to hearing that their safe investment strategy is no longer safe? Will this reduce the client’s trust in their advisor and possibly push them into making a rash, harmful decision to reduce risk? After all, in a single day on March 13, the probability of success rose to 73%. Perhaps if the client waits a few months they’ll be back up to 94%.

The lifestyle initially established using 3% of wealth was based on the end result of random (and positive) gains made over the last decade. Probability, and the reward for accepting risk, giveth and taketh away. If the advisor decides not to course correct because of faith that equity markets are going to “bounce back,” then they are guilty of subjecting their client to expectations that no longer match their current reality. The market does not owe your client a return to an initial wealth starting point that was itself arbitrary and based on random fluctuations in stock prices.

How should an advisor communicate rapid changes in a client’s likelihood of meeting future goals? There is evidence that investors become more risk averse when faced with market losses, and that individual investor underperformance occurs largely because they pull money out of risky assets after they have fallen in value. Making investors aware not only of their losses but of the impact those losses have on their likelihood of success may exacerbate counterproductive emotional responses to loss.

A better approach is for an advisor to monitor a client’s likelihood of success and suggest periodic changes to withdrawal rates, similar to the so-called guardrail approach of adjusting withdrawal rates within a prescribed band. Make a client aware that any safe withdrawal approach that involves investment in risky assets will require periodic lifestyle changes before they begin making withdrawals to prepare them for this possibility.

A variable withdrawal strategy in response to investment risk requires estimating what percentage of a client’s spending is fixed. Fixed spending is the lower bound of the guardrail. Social Security, pensions, bond ladders, or an income annuity (SPIA or DIA) are the only assets that should be used to fund retirement expenses that cannot be reduced if markets fall.

Michael Finke, PhD, is a professor of wealth management and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

Read more articles by Michael Finke