Just a week ago, central bankers, politicians and Wall Street were all asking when the market turmoil would end. The question now is whether it already has.

The S&P 500 started Tuesday 17% higher than a week ago, after gaining four days out of five and posting the best week for the benchmark U.S. stock gauge since 2009. Thank a range of catalysts, from dip buying and short covering to unprecedented monetary support and the largest fiscal stimulus ever.

Now, no one can agree if it’s sustainable.

At the heart of the debate is a phenomenon known as a bear-market rally -- a period during a protracted downward trend in which equities stage a short-term revival.

If the doomsayers are right, that’s what stocks have been experiencing, and investors can expect more declines in the weeks ahead. It’s a persuasive argument, given the backdrop of the coronavirus, and the S&P 500 opened in the red on Tuesday morning.

But if they’re wrong and the stimulus saves the economy, those on the sidelines risk missing out on a supercharged rebound.

So just how common is a bear-market rally, and what happens afterward? It’s a question loaded with difficulties, because even defining bear and bull markets is an area of fierce debate.

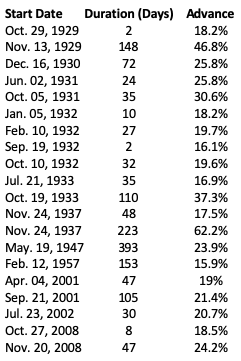

Since the end of 1927, the index that ultimately became the S&P 500 has experienced 14 separate bear runs, according to Bloomberg calculations that define them as beginning any time the gauge closes more than 20% below a record peak. Assuming a bear market continues until the index either doubles from a post-peak low or climbs above its pre-bear high, the average duration was 641 days.

Within those periods, America’s benchmark equity index has rallied more than 15% on 20 separate occasions before retracements. These advances lasted about 78 days each. But even some of the retracements were littered with upswings, underscoring how hard it is to divine a trend when sentiment is febrile.