Is it cheap or expensive?

It used to be a question that strategists answered with a simple formula, but it’s turned into a fool’s errand. The S&P 500 Index’s 12% rally in April and sharp fall in profit estimates sent its forward price-to-earnings ratio to the most expensive level in almost two decades. In the words of Muddy Waters Capital founder Carson Block, “It makes no sense.”

Still, investors want to know what an asset is worth even in a world where there’s an unprecedented level of uncertainty on earnings, monetary policy and economic activity -- and analysts have had to get creative to deliver them.

Stocks: Thinking Outside the Box

Bottom-up equity analysts tend to be behind the curve in adjusting their earnings estimates to a negative economic shock, usually doing it well after the market prices in a drop in corporate profits and sales.

This means the widely-used ratio of price-to-estimated earnings tends to indicate stocks are cheap at first, before analysts scramble to slash forecasts, causing the metric to surge higher again. The measure becomes irrelevant, particularly with so much uncertainty surrounding the pandemic and the future business environment.

Bloomberg

Dividend yields, previously a stalwart of European companies known for their lofty payouts, have also been rendered impotent. A third of companies in the Stoxx 600 have canceled or postponed dividends, while other big names such as Royal Dutch Shell Plc cut theirs. Strategists are warning that more dividend cuts and cancellations are coming, which means investors can no longer rely on the yields metric as a guide to picking stocks.

So what are analysts turning to instead? Price-to-book and cyclically adjusted P/E are both “more reliable metrics” than P/E during times of elevated earnings uncertainty, according to Barclays Plc strategist Emmanuel Cau.

Discounted cash flow is a useful method for estimating the value of an investment based on projections of how much money it will generate in the future, according to Oddo BHF’s Sylvain Goyon. But this means more homework for investors, as the metric is only useful when looking at a stock-by-stock basis instead of an overall market or sector.

In such turbulent times, purchasing managers indexes can turn out to be more useful than regular valuation metrics to trigger buy and sell signals, especially for cyclical sectors such as autos and basic resources, according to Bank of America Corp. strategist Sebastian Raedler.

History suggests that even modest improvement in PMIs point to a rally in equities. It will certainly be a low bar for gains -- the JPMorgan Global Manufacturing PMI measure slumped last month to the lowest since the financial crisis more than a decade ago.

Currencies: ‘A Dark Art’

Currencies aren’t following the usual macroeconomic cues either, making valuation -- already inherently difficult for this asset class -- that much harder.

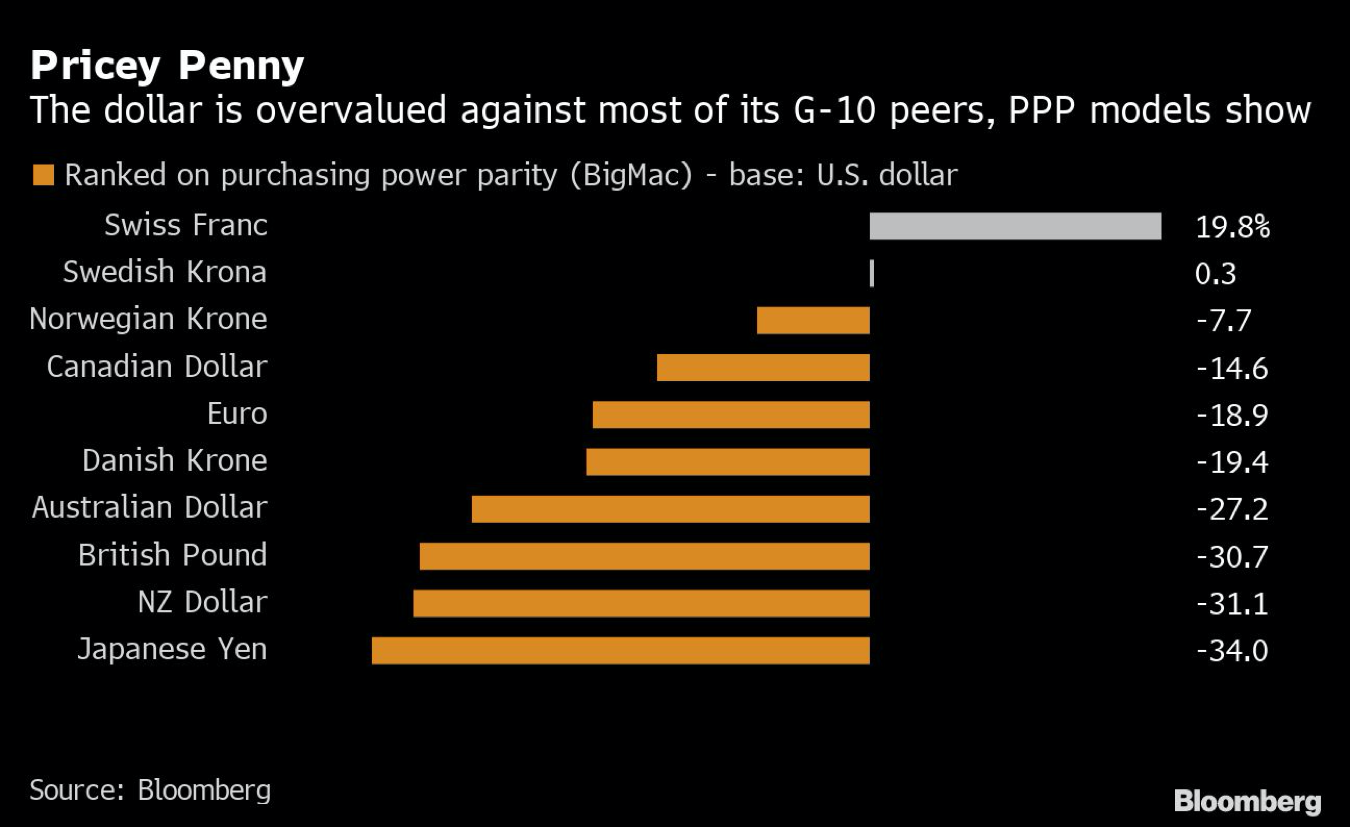

“Currency valuation is a dark art,” said Ned Rumpeltin, European head of currency strategy at Toronto-Dominion Bank. In the short term, analysts might look at measures such as rate differentials, commodity prices and relative equity market performance to gauge fair value. Over the longer term, purchasing power parity models might be useful, though big deviations can persist for years, Rumpeltin said.

The dollar is a case in point. Based on PPP, it’s overvalued compared to almost all of its Group-of-10 peers. Yet the pandemic-inflicted market turmoil has ensured haven demand for the dollar, boosting the Bloomberg Dollar Spot Index to a record in March, on the way to its largest quarterly gain since 2016.

Bloomberg

“One of the biggest challenges we face as a community in terms of assessing fundamental value right now is to determine whether we have seen a structural break in the global economy,” Rumpeltin said. FX valuation frameworks will probably need to evolve if recent events have changed macro relationships, he added.

Credit, Bonds: Central Bank Put

Forget about the historical relationship between corporate bond yields and the issuer’s growth and rating trajectory. In investment-grade credit, it’s now all about sensitivity to central bank action, according to Guilhem Savry, Unigestion’s head of macro and dynamic allocations who helps oversee $23 billion in assets.

Policy makers have never been more aggressive in the corporate sector. The Federal Reserve is getting ready to unleash a buying program that includes recently downgraded corporate bonds, and the European Central Bank is now also buying credit through its 750-billion-euro ($809 billion) pandemic quantitative easing program.

Central bank demand, rather than economic fundamentals, has also become the dominant driver in sovereign bonds, according to Antoine Bouvet, senior rates strategist at ING Groep NV. Where yields go next will depend on whether monetary policy stays aggressive, if a lifting of lockdown measures sparks a second wave, and if long-term economic disruptions lead to recession, Bouvet added.

Oil: Life After Sub-Zero

Oil’s slump below zero last month showed just how hard it is to price commodities in a fragmented world where demand is at a standstill, storage is full and, in some cases, transportation links have broken down. Similarly, gold prices saw record dislocations between New York and London, because the planes that transport bullion stopped flying.

Bloomberg

Most assets -- with the relatively recent exclusion of bond yields -- can only ever go as low as zero and are assumed to have a log-normal distribution. Suddenly, commodity analysts have had to adapt their models for a world where that’s not the case.

“Oil has always been difficult to forecast, and right now it is close to impossible with even the brightest minds changing direction within the space of a few days,” Ole Hansen, head of commodity strategy at Saxo Bank A/S, said by email from Copenhagen. “The market is trading themes without knowing the full details.”

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Msika, Anooja Debnath