The Asset-Location Decision and Related Topics

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The advisory industry is unaware that the traditional asset-location rules (i.e, put bonds in tax-deferred accounts and stocks in taxable accounts) don’t work in our low interest rate environment. The exact opposite is appropriate for most retirees and individuals entering retirement who do not have substantial unrealized capital gains in their taxable accounts.

This article begins with an analysis of effective tax rates on bonds and stocks held in one of three savings vehicles: a tax-exempt Roth account, like a Roth IRA; a tax-deferred account, like a 401(k); and a taxable account.1 This background information is necessary to discuss the asset-location literature, which is the main topic of this article. In addition, I will respond to several of the seven points raised by Reed (2019) in his recent criticism of prior asset-location studies.

IncomeSolver.com leverages Dr. William Reichenstein’s research and methodology to help advisors optimize how to generate retirement income and coordinate Social Security. In addition to identifying the best tax efficient withdrawal sequences, IncomeSolver.com incorporates Asset Location methodology showing advisors the “alpha” they can find by applying different approaches to their clients’ portfolios.

The asset-location decision asks whether an investor should 1) locate stocks in taxable accounts and bonds in retirement accounts (that is, Roth accounts and tax-deferred accounts) to the degree possible, while attaining the target asset allocation; or 2) locate bonds in taxable accounts and stocks in retirement accounts to the degree possible, while attaining the target asset allocation.

As we shall see, with the exception of when interest rates are extremely low like they are today, the consistent asset-location advice from what I call “Group 2” studies is that investors should locate stocks in taxable accounts and bonds in retirement accounts to the degree possible, while attaining their target asset allocation. The advice for investors in today’s extremely low interest rate environment depends in large part on whether they have substantial unrealized capital gains on stock held in their taxable account. This advice is presented later near the end of this article.

Effective tax rates across savings vehicles

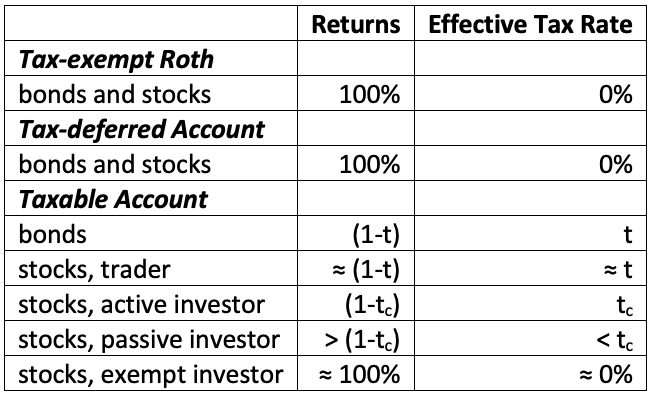

Table 1 considers two asset classes – bonds and stocks – and three savings vehicles – tax-exempt Roths, tax-deferred accounts (TDAs), and taxable accounts. For each savings vehicle, the investor begins with $1 market value and I calculate its current and future after-tax values. To hold everything else constant, I assume the underlying investment is the same across the savings vehicles. The annual pretax rate of return is r, the investment horizon is n years, the marginal tax rate on ordinary income this year is t0, the marginal tax rate on ordinary income in the withdrawal year n years hence is tn, and the tax rate on long-term capital gains and qualified dividends in all years is tc. Since the asset-location literature is concerned about savings strategies for retirement, the usual investment horizon is until some date during their retirement years. In this section, I develop models of the effective tax rate on stocks and bonds when held in each of the three savings vehicles. The portion of an asset’s pretax returns earned by the investor is 1 minus the effective tax rate.

Roth account

Tax-exempt Roth accounts include Roth IRA, Roth 401(k), and Roth 403(b). The $1 market value in a Roth account is $1 of after-tax funds. For bonds and stocks, its after-tax value grows from $1 today to (1+r)n dollars n years hence.2 As the name implies, the effective tax rate on funds held in a tax-exempt Roth is 0%; that is, investors receive all returns on funds held in a Roth.

Tax-deferred account

Examples of a TDA include traditional IRA, 401(k), 403(b), SEP-IRA, and SIMPLE accounts. The $1 market value in a TDA is $1 of pretax funds.3 The pretax value after n years is $1(1+r)n dollars and its after-tax value n years hence is (1+r)n (1-tn) dollars, where tn is the marginal tax rate at withdrawal n years hence. For clarity, the marginal tax rate is the tax rate on the next dollar of income.4 Thus, the original $1 of pretax funds in the TDA will buy (1-tn) as many goods and services as the original $1 of after-tax funds held in the Roth. For bonds and stocks held in a TDA, its after-tax value grows from (1-tn) dollar today to (1+r)n (1- tn) dollars n years hence. Notice that since the funds will be withdrawn during retirement, the effective tax rate is tn, the expected marginal tax rate in retirement, and not today’s marginal tax rate.

For example, assume the marginal tax rate in retirement will be 25%. Thus, (1- tn) is $0.75. The $1 of pretax funds in the TDA has the same purchasing power as $0.75 of after-tax funds held in a Roth. They will each buy $0.75(1 + r)n of goods and services n years hence.

Thus, as emphasized by Reichenstein (2006, 2007a), the TDA is like a partnership with the government. The investor effectively owns (1- tn) of the current principal, while the government effectively owns the remaining tn of the current principal. Without loss of generality, assume that the underlying investment earns a 100% cumulative pretax return between now and withdrawal n years hence and the marginal tax rate n years hence is 25%. The $1 of pretax funds in the TDA grows to $2 pretax, but the government gets $0.50 at withdrawal, which is 25% of the withdrawal amount. So, the TDA is worth $1.50 after taxes. Thus, the investor can buy this amount of goods and services. This is precisely the same as if this investor began with $0.75 of after-tax funds held in a Roth. The Roth’s after-tax value after n years would be $1.50, and the investor could withdraw this amount and buy $1.50 of goods and services.

This example demonstrates that the TDA is like a partnership with the investor serving as the majority partner and the government being the minority partner. As majority partner, the investor gets to make the investment decisions and decides when to withdraw the funds (subject to rules determining required minimum distributions). However, the government gets tn of each dollar withdrawn. The investor effectively owns (1 – tn) of the current principal value of the TDA, but its after-tax value grows from (1 – tn) dollar today to (1 – tn) (1 + r)n dollars in retirement. That is, the after-tax value of funds held in a TDA effectively grows tax free at the pretax rate of return, r. Thus, properly viewed, the effective tax rate on funds held in a TDA is 0%.

As explained in Reichenstein (2019), the decision to save this year in a TDA or a Roth depends primarily on the relative sizes of this year’s marginal tax rate, t0, and the expected marginal tax rate at withdrawal, tn. An investor should save in a TDA if t0 is greater than tn, but save in a Roth if t0 is less than tn. Similarly, Reichenstein (2019) shows that an investor should consider a partial Roth conversion this year if t0 is less than tn. Thus, the relative sizes of t0 and tn should affect the choice between saving in a TDA or a Roth.

However, consider an investor who has $1,000,000 (or any other amount) in a TDA today. If he bases his asset allocation decision on after-tax values, as I and Reed recommend, then he should view this as $1,000,000 (1 – tn) of his after-tax dollars, while the government owns the remaining $1,000,000 tn of this TDA’s current principal. In Point 6, Reed (2019) writes, “Never forget the [TDA’s] potential bonus from lower withdrawal tax rates.” As noted here, the relative sizes of t0 and tn should affect the choice between saving in a TDA or a Roth this year, but this investor’s marginal tax rate this year, t0, and the marginal tax rate in all prior years that he contributed funds to this TDA are irrelevant when calculating his current asset allocation. Therefore, he can forget the bonus he received from prior-year’s contributions to TDAs when that year’s t0 was less than tn. Instead, the current after-tax value of his TDA is $1,000,000 (1 – tn).

Bonds in a taxable account

To be consistent with prior asset-location studies, including Reed (2019), I assume the taxable account begins with $1 of after-tax funds, that is, the asset’s cost basis equals its market value. For bonds, each year’s pretax return is r, and this return is taxed each year at t. The after-tax value grows from $1 today to (1+r(1-t))n dollars n years hence. The after-tax value grows at r(1-t). The investor receives (1-t) of returns; the effective tax rate is t.

Stocks in a taxable account

For stocks held in taxable accounts, the portion of returns received by the individual investor varies with the stock-management style. In this section, I model investors with four stock-management styles. The management styles include those of a trader, an active investor, a passive investor, and what I call an exempt investor. The pretax return is the sum of capital gain, g, and qualified dividend yield, d; that is, r = g + d.

To qualify for the preferential tax treatment of long-term capital gains, an asset must be held for at least one year and one day. Capital gains realized on assets held for shorter periods of time are taxed as ordinary income. This tax treatment of capital gains is the key difference between the trader and the active investor. The trader realizes all capital gains within one year and pays taxes on these gains at the ordinary income tax rate. His after-tax value grows from $1 today to (1+ g(1-t) + d(1-tc))n dollars n years hence. This equation assumes this trader holds the stock long enough to qualify for the preferential tax rate on qualified dividends. Assume capital gains average 6% and the dividend yield averages 2% for the long horizons associated with most retirement savings, the ordinary income tax rate, t, is 25%, and tax rate on qualified dividends, tc, is 15%. In this case, the trader receives 77.5%, [{6%(0.75) + 2%(0.85)}/8%], of returns. Table 1 says this trader receives almost (1-t) of returns, that is, ≈ (1 – t) of returns; the effective tax rate is ≈ t.

The active investor realizes all capital gains in one year and one day and pays taxes at tc on capital gains and qualifying dividends. The active investor holds stocks just long enough to qualify for the preferential long-term capital gain tax rate, tc, but he does not allow the gains to grow unharvested for multiple years, and thus does not benefit from tax-deferred growth. Each year’s pretax return is r, and this return is taxed each year at tc. Thus, the after-tax annual return is r(1- tc). The after-tax value grows from $1 today to (1+r(1-tc))n dollars n years hence. This investor receives (1-tc) of returns; the effective tax rate is tc.

I defer discussion of the passive stock investor until later.

Table 1. Portion of returns received by individual investors in tax-exempt Roth, tax-deferred account, and taxable account

The ordinary income tax rate is t in the years before withdrawal and tn in the withdrawal year, and the tax rate on long-term capital gains and qualified dividends is tc in all years.

Tax-exempt Roths include Roth IRAs, while examples of tax-deferred accounts include 401(k)s, 403(b)s, Keoghs, and SEP-IRAs.

Source: Reichenstein, Income Strategies (2019) and In the Presence of Taxes: Applications of After-tax Asset Valuations, FPA Press, 2008. (FPA Press went out of business. Thus, this book is no longer in print.)

The exempt stock investor never realizes capital gains and never pays taxes on the gains, but he pays taxes each year on dividends. Eventually, the appreciated stock is either donated to charity or sold immediately after receiving the step-up in basis at the investor’s death. If donated to a qualifying charity, the individual can deduct the stock’s market value and the charity can sell the stock without incurring taxes. At the death of the taxable-account owner, the stock’s cost basis increases to the market value at death. So, the beneficiary can sell it at that time without incurring capital-gains taxes. The after-tax value grows from $1 today to (1+ g + d(1- tc))n dollars n years hence. For most stocks, this investor receives almost all returns. For example, if the dividend yield is 2%, capital gains average 6%, and the tax rate on qualified dividends is 15% then, on average, this exempt stock investor receives 96.25% [or {6% + 2%(1- 0.15)}/8%] of returns. Table 1 says this investor receives almost 100% of returns, that is, ≈ 100% of returns; the effective tax rate is ≈ 0%. However, relatively few investors are sufficiently passive to reap the tax benefits of an exempt investor.

Consider most savers. They plan to liquidate their taxable accounts to finance spending during their lifetime. As we shall see, Reed (2019) assumes an effective tax rate on stocks held in a taxable account of 3.75%, [{2% (1 – 0.15)/8% total return]; that is, Reed assumes that no one ever pays taxes on unrealized gains on stocks held in a taxable account. If stocks earn a pretax return of 8% every year, as Reed assumes, then the only time this could happen is if the stocks are held in a married couple’s joint taxable account and the stocks are sold immediately after the death of the first spouse to die. In this case, the surviving spouse could sell the stocks immediately after the death of the first spouse to finance his or her spending needs that year without incurring capital gains taxes. But that is the only time this couple could sell these stocks to finance their spending needs without incurring capital gains taxes.

Furthermore, there is no time when a single taxpayer could sell the stocks during her lifetime to finance her spending needs without incurring capital gains taxes. In short, Reed’s assumption that the effective tax rate on stocks held in a taxable account is 3.75% is inappropriate for the overwhelming majority of investors who plan to use their savings to finance their future consumption needs.

Benefits of tax-deferred rowth

I now illustrate the advantages of tax-deferred growth that applies to passively-managed stocks held in a taxable account. Since this section is concerned about the benefits of tax-deferred growth, let’s assume the passively-managed stocks’ returns are all in the form of capital gains, that is, there are no dividends. The after-tax value grows from $1 today to the following values after withdrawal in n years:

(1+r)n – tc[(1+r)n – 1] or (1a)

(1+r)n (1-tc) + tc. (1b)

Equation 1a can be interpreted as follows. The original $1 grows to (1+r)n dollars after n years. At withdrawal, taxes at tc, the long-term capital gains tax rate, are due on deferred returns, where the amount in brackets, [(1+r)n – 1], represents deferred returns. For example, suppose the original $1 grows at 8% per year for 30 years and is worth $10.06. The $10.06 is withdrawn, and taxes are due at tc on the $9.06 of tax-deferred returns. The original $1 was already after-tax funds. So, it can be withdrawn tax free.

Equation 1b, which is algebraically equivalent to Equation 1a, can be explained as follows. At withdrawal, the (1+r)n is taxed at tc, but then the investor receives an additional tc (times the cost basis of $1), which is the taxes saved because the original $1 can be withdrawn tax free. From the prior example, the $10.06 is taxes at tc, but then we add $0.15 to (1+r)n (1-tc), because the $1 original principal can be withdrawn tax free.

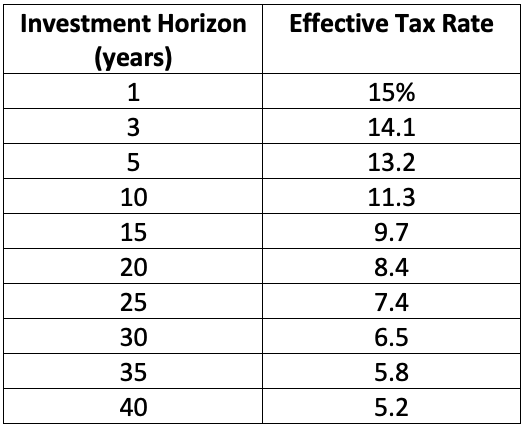

Table 2 illustrates the advantages of tax-deferred growth for most passive stock investors who will eventually pay a tax rate of 15% on their long-term capital gains. For an 8% annual tax-deferred return, it presents the effective tax rates for a passive stock investor who holds the stock until the end of the investment horizon, at which time taxes are paid on the deferred returns at 15%. There is little benefit to deferring gains for a few years. For example, for a three-year horizon the effective tax rate is 14.1%, which is less than 1% lower than the long-term capital gains rate. The 14.1% effective rate means that the after-tax wealth after three years is the same as if the returns were fully taxed each year at 14.1%.5

The effective tax rate decreases as the horizon lengthens. For a 10-year horizon, the effective tax rate is 11.3%, which is more than one-fifth lower than 15%. Although terms such as “large” and “small” are always open to interpretation, these numbers suggest that the benefits of tax-deferred growth are small for short horizons (e.g., five years or less), but large for horizons of 10 years or longer. Table 1 says the passive stock investor receives more than (1 – tc) of returns; the effective tax rate is less than tc. However, most investors sell stocks held in a taxable account, on average, within a few years, and for these investors there is minimal benefit to deferring gains beyond the one year and one day that is necessary to qualify as a long-term capital gain.

Table 2. Effective tax rates by investment horizon for 8% return

Table 2 summarizes the effective tax rates for stocks and bonds held in tax-exempt Roths, TDAs, and taxable accounts. Let’s consider stocks first. For stocks held in Roths or TDAs, the effective tax rate is 0%. For stocks held in taxable accounts, the effective tax rate is positive. For investors that plan to eventually liquidate stocks held in a taxable account to meet their spending needs, the effective tax rate is probably close to 15%.

Now let’s look at bonds. The effective tax rate on bonds held in Roths or TDAs is 0%. The effective tax rate on (non-tax-exempt) bonds held in a taxable account is t, the ordinary income tax rate.

In short, the effective tax rates on stocks and bonds held in a TDAs or a Roth are 0%, while the effective tax rates on stocks and bonds are positive when held in a taxable account. Therefore, in general, when saving for retirement, individuals should save all they are permitted to save or all they can afford to save in TDAs and Roths.

In point 1 of Reed’s (2019), he says there is a mistaken understanding in the asset-location literature that you should keep stocks out of retirement accounts, (that is, TDAs or Roths), even if that means using a taxable account. Similarly, in point 2, Reed says that, according to the asset-location literature, another rule of thumb is to hold volatile stocks in taxable accounts, instead of retirement accounts, because the tax benefit from capital losses are lost in retirement accounts, such as TDAs or Roths. As noted here and in my prior writings, I never made these arguments and they are not part of my asset-location advice. In short, Reid and I agree that, when saving for retirement, the tax structures facing assets, including stocks, held in TDAs and Roths are better than the tax structure facing assets held in taxable accounts.

Asset-location decision

For simplicity, but without loss of generality, consider a world with two assets – stocks and bonds – and two savings vehicles – taxable accounts and retirement accounts. The asset-location studies ask whether it is better to locate stocks in taxable accounts and bonds in retirement accounts (for example, TDAs) to the degree possible, while attaining the investor’s desired asset allocation, or vice versa.

There have been two groups of studies that have examined this asset-location decision. The first group of studies assumes constant rates of returns on stocks and bonds and examines whether the after-tax ending wealth is larger when stocks are held in taxable accounts and bonds are held in retirement accounts, or vice versa. This group of studies only considers after-tax wealth (that is, returns), but they do not consider risk. Examples of these studies include Daryanani (2004), Daryanani and Cordaro (2005), Jaconetti (2007), Kitces (2013), Reed (2019), and Trout (2013).

Group 1 studies

To illustrate the analyses in this first group of studies, I use examples in “Asset Location – Irrelevant,” by Reed (2019). He assumes pretax returns on stocks and bonds are 8% and 3%, respectively. In addition, he assumes bond returns when held in a taxable account are taxed at 25%, while stock returns when held in a taxable account are taxed at 3.75%, [2%(1 – 0.15)/8%], that is, he assumes that capital gains are never taxed.

In Reed’s first case, he compares the after-tax value of two portfolios after 30 years. Portfolio A begins with $750 of after-tax funds in stocks held in a taxable account and $750 of pretax funds in bonds held in a TDA. Portfolio B begins with $750 of after-tax funds in bonds held in a taxable account and $750 of pretax funds in stocks held in a TDA. After 30 years (with no rebalancing), the ending after-tax value of Portfolio A exceeds the ending after-tax value of portfolio B. Thus, this case that uses the group 1 framework would conclude that the optimal asset-location decision is to hold stocks in taxable accounts and bonds in TDAs.

Reed appropriately criticizes this comparison of portfolios A and B because it fails to recognize that the government effectively owns 25% of the current value of the TDA. Thus, portfolios A and B do not begin with the same after-tax asset allocations. That is, portfolios A and B do not compare portfolios that differ only with respect to their asset-location decision. I agree with Reed’s criticism of many group 1 studies, as demonstrated with my writings since at least 2001.

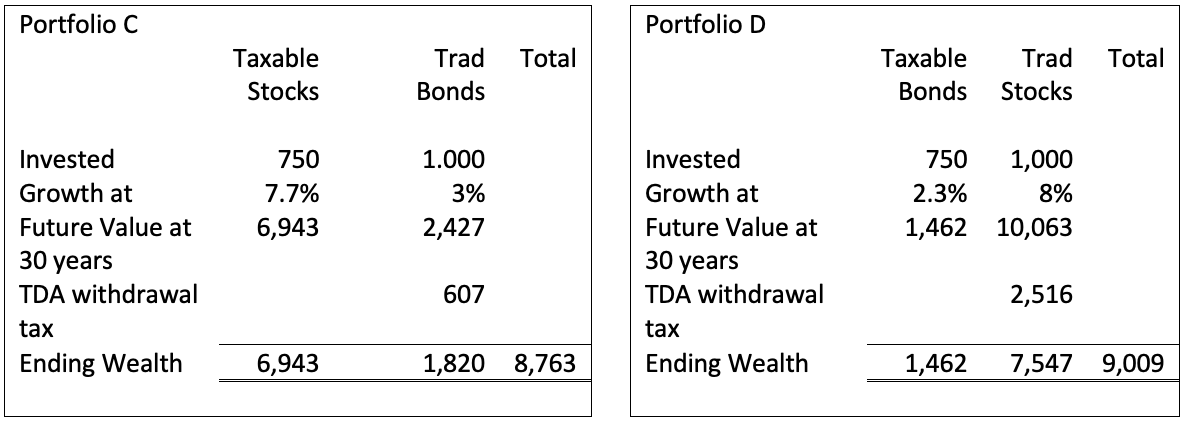

Reed then compares the after-tax value of two portfolios after 30 years. From Table 3, portfolio C begins with $750 of after-tax funds in stocks held in a taxable account and $1,000 of pretax funds, but $750 of after-tax funds (that is, $1,000 (1 – 0.25, where tn = 0.25), in bonds held in a TDA, (which he labels Trad). Portfolio D begins with $750 of after-tax funds in bonds held in a taxable account and $1,000 of pretax funds, but $750 of after-tax funds, in stocks held in a TDA. After 30 years (with no rebalancing), the ending after-tax value of portfolio D exceeds the ending value of portfolio C. Thus, Reed concludes that the optimal asset-location decision is to hold stocks in retirement accounts (that is, TDAs or Roths) and bonds in taxable accounts.

Table 3. Comparison of portfolios C and D

Furthermore, in his point 7, Reed (2019) concludes that the investor should not rebalance the portfolios over the 30-year investment horizon, because rebalancing “dilutes the benefits from asset location because high-return assets [i.e., stocks in portfolio C] are repeatedly sold.”

Let’s examine this argument. Portfolios C and D both begin with a 50% stock/50% bond after-tax asset allocation. However, after 30 years, when all funds are withdrawn and taxes paid, portfolio D’s asset allocation contains 84% stocks/16% bonds. Thus, Reed methodology for making the asset-location decision assumes that this typical investor should increase her portfolio’s stock allocation from 50% in her early working years to 84% after a 30-years accumulation period, when she is in or near retirement. This advice is contrary to the advice of the rest of the investment profession. The consistent advice in the profession is that, as an investor ages, she should decrease the stock allocation of her financial portfolio. To repeat, Reed argues that rebalancing the portfolio every year would greatly reduce the benefit of the asset-location decision to locate stocks in retirement accounts, and thus should be avoided. Thus, in my opinion, Reed’s recommendation that this typical investor should allow her stock allocation to increase from 50% to 84% after a 30-year accumulation period, because the after-tax value of assets held in her retirement account increased to 84% of her portfolio’s after-tax assets, represents an egregious error.

Let me point out another frequent misunderstanding in the asset-location literature. Consider an investor who has 90% of the after-tax value of her financial portfolio in retirement accounts and 10% in a taxable account. If she wants a 50% stock/50% bond after-tax asset allocation then the usual asset-location advice is that she should allocate 55.6%, [50/90], of her retirement accounts to bonds, while allocating the remaining funds in her retirement accounts and all funds in her taxable account to stocks. That is, the asset-location advice does not say that all retirement account funds should be allocated to one asset class and all taxable account funds should be allocated to the other asset class. In Reed’s examples and those in most asset-location studies, it may appear that the allocation of financial assets between retirement accounts and taxable accounts should determine the asset allocation. For example, from Reed’s prior example, it appears that 1) the investor should locate only stocks in the retirement account and only bonds in the taxable account because portfolio D has a higher after-tax value than portfolio C and 2) this investor’s optimal initial asset allocation should be 50% stocks/50% bonds because half of the initial after-tax value of her financial portfolio is held in taxable accounts and half in retirement accounts. The optimal asset allocation should not depend on the allocation of after-tax funds between taxable accounts and retirement accounts.

There are other errors in Reed’s framework for making the asset-location decision. To illustrate one of these errors, let’s return to his comparison of portfolios C and D. Portfolio C holds stocks in a taxable account. After 30 years, the stocks in portfolio C has a cost basis of $750, but a market value of $6,943. He assumes no one ever pays taxes on the $6,893 of unrealized capital gains. In Reed’s point 3, he says investors should not “ignore the reality that before-tax dollars are worth less than after-tax dollars” when calculating their asset allocation. However, in Reed’s framework for making the asset-location decision, he ignores the reality that before-tax dollars in the form of unrealized capital gains on stocks held in taxable accounts have an embedded tax liability, and thus are worth less than after-tax dollars.

Group 2 studies

As explained in Reichenstein (2019) and Reichenstein and Meyer (2013), group 1 studies make two errors. When these two errors are corrected, as they are in group 2 studies, then the optimal asset allocation decision (with the exception of when interest rates are extremely low like they are today) should be to hold stocks in taxable accounts and to hold bonds in retirement accounts like a TDA or Roth to the degree possible, while attaining the target after-tax asset allocation.

Portfolios A and B in Reed’s example above use the traditional approach to calculate the investor’s asset allocation. This approach says the investor has a 50% stocks/50% bonds initial asset allocation. However, the traditional approach fails to recognize that the government effectively owns tn of the current principal value of TDA funds. If we adjust for this fact, portfolio A initially contains $750 of the investor’s after-tax funds in stocks and $562.50, [$750 (1 – 0.25)], of the investor’s after-tax funds in bonds held in a TDA for a 57.1% stocks/42.9% bonds after-tax asset allocation; the government effectively owns the other $187.50, [$750 (0.25)], of TDA funds. In contrast, portfolio B contains $750 of the investor’s after-tax funds in bonds and $562.50 of the investor’s after-tax funds in stocks for a 42.9% stocks/57.1% bonds after-tax asset allocation. Thus, despite being the intent of most group 1 studies, the two portfolios do not change the asset location, while holding everything else constant. Rather, they also have different initial after-tax asset allocations.

To repeat, in Reed’s comparison of portfolios C and D, he compares portfolios that have the same initial after-tax asset allocation. Unfortunately, since he fails to adjust for the embedded tax liabilities on stocks held in taxable accounts, his calculation of the asset allocation of portfolio C after 30 years is wrong. The calculation of an investor’s after-tax asset allocation compares after-tax funds to after-tax funds, that is, it compares apples to apples. In contrast, the traditional approach of calculating asset allocation fails to distinguish between the pretax dollars in TDAs, the after-tax dollars in Roths, and the usual combination of pretax and after-tax dollars in taxable accounts. Thus, the traditional approach fails to recognize the embedded tax liability on 1) pretax funds held in a TDA and 2) unrealized capital gains on assets held in a taxable account. That is, the traditional approach to calculating asset allocation compares apples to oranges. For a partial list of studies on the logic and merit of calculating a household’s after-tax asset allocation, see Horan (2007a, 2007b) and Reichenstein (2006, 2007a, 2008, 2013), Reichenstein and Jennings (2003) and Reichenstein, Horan, and Jennings (2012).

However, Reed argues that the investor should not rebalance the portfolio during the accumulation period. Thus, in his example with a 30-year investment horizon, he argues that the typical investor should let her after-tax stock allocation rise from 50% to 84% over her 30-year accumulation period. Thus, Reed’s approach to the asset-location decision calls for investors 1) to disregard the embedded tax liability on stocks held in a taxable account and 2) to disregard risk in two ways. To illustrate the first way his approach ignores risk, note that he argues that the typical investor in portfolio D should allow her stock allocation to rise from 50% to 84% as she ages over a 30-year investment horizon. Second, his approach ignores the fact that the government bears some of the risk of the assets held in a taxable account. I make this point next.

The second error in group 1 studies is the failure to recognize that the government bears some of the risk on assets held in taxable accounts. That is, the investor does not bear all the risk on asset held in taxable accounts. Thus, the investor does not bear the same amount of risk in portfolios C and D. Therefore, despite Reed’s intent, portfolios C and D do not change the asset location, while holding everything else constant.

As the name implies, when held in a tax-exempt Roth, the investor receives 100% of the assets’ pretax returns and bears 100% of the assets’ risk. Although not as evident, when held in a TDA, the investor also receives 100% of the pretax returns and bears 100% of the risk on assets. Assume the TDA begins with $1 of pretax funds. Assuming tn is 25%, this TDA is best viewed as $0.75 of the investor’s after-tax funds with the government owning the remaining $0.25 of the current principal. Before withdrawal from the TDA n years hence, bonds’ pretax value is $1(1.03)n. After withdrawal, the after-tax value is $0.75(1.03)n. The investor’s after-tax value grows from $0.75 today to $0.75(1.03)n after withdrawal. Similarly, before withdrawal from a TDA in n years, stocks’ pretax value is $1(1.08)n. After withdrawal, its after-tax value is $0.75(1.08)n. Whether the underlying asset is bonds or stocks, the investor’s after-tax value grows from $0.75 today to $0.75(1+r)n at withdrawal, where r is the underlying asset’s pretax rate of return. The after-tax value grows tax free. Therefore, when held in a TDA, the investor receives 100% of the asset’s pretax returns and bears 100% of the asset’s pretax risk, whether the underlying asset is bonds or stocks.

To be consistent with Reed’s comparison of portfolios C and D, let’s assume the investor’s portfolio begins with $750 of after-tax funds in both the taxable account and the TDA. Thus, Reed assumes that the market value and cost basis of the asset held in the taxable account are each $750. The after-tax value of the bond held in a taxable account grows from $750 today to $750(1 + 0.03(1 - 0.25))n or to $750(1.0225)n at withdrawal. The after-tax value grows at the after-tax 2.25% rate of return. Here, I assume that the effective tax rate on stocks held in a taxable account in portfolio C is 15%, which is consistent with most asset-location studies. To repeat, this removes Reed’s assumption that no taxes are ever paid on capital gains on stocks held in a taxable account. However, this substitution does not affect the merits of my major criticisms of his study. The after-tax value of stocks held in a taxable account grows from $750 today to $750(1 + 0.08(1 - 0.15))n or to $1(1.068)n at withdrawal. When held in a taxable account, the investor gets 75% of bonds’ pretax return and 85% of stocks’ pretax returns.

Studies from both groups of asset-location studies agree that the preferential tax rate that applies to long-term capital gains and qualified dividends compared to the higher ordinary-income tax rate that applies to interest income is a major factor explaining the usual asset-location advice to hold stocks in taxable accounts and bonds in retirement accounts to the degree possible, while attaining the target asset allocation. Now, let’s examine the risk borne by the investor.

Assume the pretax returns on stocks are -7%, 8%, and 23% in a three-year period. The average pretax return is 8% and the pretax standard deviation (that is, risk) is 15%. Assuming the 7% loss can be used to offset long-term gains, the pretax returns for the investor become after-tax returns of -5.95%, 6.8%, and 19.55%. This active investor receives 85% of stocks’ pretax returns and bears 85% of stocks’ pretax risk when held in a taxable account. Similarly, since the government takes some of bonds’ returns, it also bears some of bonds’ risk. The investor receives 75% of bonds’ pretax returns and bears 75% of bonds’ pretax risk when held in a taxable account. In short, even though there are only two assets, there are effectively four “assets” to consider in the asset-location decision, because bonds and stocks are effectively different assets when held in a taxable account and a retirement account.

For example, when stocks are held in a TDA or a Roth, the investor’s after-tax expected return is 8%, while his after-tax risk is 15%. In contrast, when stocks are held in a taxable account, the active investor’s after-tax expected return is 6.8%, while his after-tax risk is 12.75%, [15%(1 – 0.15)]. Thus, stocks are effectively different assets when held in a retirement account (i.e., TDA or Roth) or a taxable account. Similarly, when bonds are held in a retirement account, the investor’s after-tax expected return is 3%, while his after-tax risk may be 5%. In contrast, when bonds are held in a taxable account, the investor’s after-tax expected return is 2.25%, while his after-tax risk is 3.75%, [5%(1 – 0.25)]. Thus, stocks and bonds are effectively different assets when held in a retirement account or a taxable account.

Of course, investors are concerned about both returns and risk. Consequently, once we recognize that the investor bears different amounts of after-tax risk and receives different amounts of after-tax returns in portfolios C and D, we can all agree that group 1 studies that only consider after-tax returns use a flawed approach to determine the optimal asset allocation and optimal asset location. Like other group 1 studies, Reed’s framework looks only at the after-tax returns earned by investors, and it ignores differences in the after-tax risk borne by investors. Thus, this framework is unacceptable.

Recall that Reed’s approach calls for no portfolio rebalancing for the 30-year investment horizon. Thus, it recommends the opposite of the conventional asset-location advice. In my opinion, Reed’s argument that the investor should not rebalance her portfolio each year, but instead allow her stock allocation to dramatically increase during a 30-year accumulation period, presents another egregious error in his approach to deciding the optimal asset location.

Group 2 studies use an after-tax approach to jointly address the asset-allocation and asset-location decisions. These studies include Reichenstein (2001a, 2001b, 2006, 2007a, 2007b, 2008), Reichenstein, Horan, and Jennings (2012), Reichenstein and Jennings (2003), Reichenstein and Meyer (2013), Dammon, Spatt, and Zhang (2004), Horan (2007a, 2007b), and Horan and Al Zaman (2008). Since both after-tax risk and after-tax return must be considered, this group of studies uses mean-variance optimization to jointly determine both the optimal asset-allocation and the optimal asset-location decisions.

The optimal asset-location in the framework considered by this second group of studies is, except when interest rates are extremely low, always the following: Investors should locate stocks in taxable accounts and bonds in retirement accounts (e.g., Roths and TDAs) to the degree possible, while attaining the household’s target after-tax asset allocation. This asset-location advice is the default option in the Income Solver software.

Extremely low interest rate environment

Now, let’s address the exception, which exists today. As discussed in Reichenstein and Meyer (2013), when interest rates are extremely low, the usual asset-location advice can be reversed, especially for individuals with above-average risk aversion, which would include most investors in or near retirement. Consider the interest rate environment after the COVID-19 pandemic hit the U.S. For example, today’s (May 7) yields on five- and 10-year Treasury bonds are 0.29% and 0.63%. Assume bonds return 0.6% and stock return 5% for the next decade. Assuming an ordinary income tax rate of 25%, if bonds are held in taxable accounts then the lost return due to taxes would be 0.15%. Assuming a tax rate of 15% on stocks held in taxable accounts, the lost return would be 0.75%. As explained earlier, properly viewed, there is no return lost on the asset held in retirement accounts. Thus, in todays’ extremely low interest rate environment, the asset-location strategy of holding bonds in taxable accounts and stock in retirement accounts to the degree possible, while attaining the target asset allocation, would provide a higher after-tax return than the opposite asset-location strategy. As discussed above, the government bears some of the risk of assets held in taxable accounts. Nevertheless, for many middle- and high-income taxpayers (that is, those who would pay taxes on long-term capital gains and qualified dividends), the optimal asset-location advice would be the opposite in this extremely low interest rate.

My advice concerning the asset-location decision for investors in this low interest rate environment depends, in part, on whether they have substantial unrealized capital gains on assets held in their taxable account. Suppose an investor has stocks with substantial unrealized capital gains located in his taxable account. I would not recommend that he change his asset-location strategy because this would require him to sell these stocks and thus incur capital gains taxes, and then move bonds into the taxable account. A key objective of asset-location strategies is to minimize taxes. Thus, I recommend that this investor retain his stocks with unrealized capital gains in his taxable account. He could sell stock with no or trivial unrealized gains in his taxable account. In addition, while this low interest rate environment exists, new investments in his taxable account should be allocated to bonds and new investments to his retirement accounts should be allocated to stocks, while attaining his target asset allocation. However, he should not incur unnecessary capital gains taxes by selling stocks with unrealized capital gains held in a taxable account.

In contrast, an investor with no or trivial capital gains on stocks held in his taxable account could sell those stocks held in his taxable account and replace them with bonds. At the same time, he should replace bonds with stocks in his retirement accounts, while attaining his target asset allocation. In short, such investors (and new investors with no current investments) should adopt the optimal asset-location advice in this low interest rate environment. This advice is to hold bonds in taxable accounts and stocks in retirement accounts to the degree possible, while attaining their target asset allocation.

Summary

The overwhelming majority of investors calculate their asset allocation using the traditional fashion that fails to distinguish between the pretax dollars in TDAs, the after-tax dollars in Roths, and the usual combination of pretax and after-tax dollars on assets held in taxable accounts. I encourage investors to convert all financial account values to after-tax dollars and then to calculate their asset allocation based on those after-tax dollars. Yes, this requires estimates such as the estimate of tn, a representative marginal tax rate in retirement. However, by ignoring the embedded tax liability inherent it TDA balances and thus using their pretax market values in the asset-allocation calculation, the investor is implicitly assuming that tn will be 0%. As I argued in Reichenstein (2006) and elsewhere, it is better to estimate tn and calculate an after-tax asset allocation that is approximately correct than to implicitly assume tn is 0%, and thus calculate an asset-allocation that we know is wrong.

Similarly, investors should reduce the market value of assets held in taxable accounts for the embedded tax liability associated with unrealized gains on assets held in taxable accounts. Ironically, Reed emphasized the need to adjust TDA balances for their embedded tax liability, but he failed to adjust taxable account balances for their embedded tax liability.

Regardless of the method used to calculate an investor’s asset allocation, this investor should also consider how their asset-location decision will affect their portfolio’s after-tax risk and after-tax returns. As argued by numerous authors, the usual asset-location advice in a typical interest rate environment is that an investor should locate stocks in the taxable account and bonds in retirement accounts (i.e., TDAs and Roths) to the degree possible, while attaining their target asset allocation. An investor’s asset-allocation decision is more important than her asset-location decision. Thus, Reed’s approach to making the asset-location decision forces an investor to ignore her asset allocation during a potentially decades-long accumulation period. Personally, I suspect few in the financial profession, besides Reed, who would conclude that a typical investor should allow her stock allocation to rise dramatically as she ages.

To the contrary, the profession appears to be in unanimous agreement that Reed’s approach to making the asset-location decision is wrong for multiple reasons. First, it would likely cause an investor to forego an optimal asset-allocation decision in the pursuit of an alleged optimal asset-location decision. However, the asset-allocation decision is more important than the asset-location decision. Second, Reed’s framework for making the asset-location decision fails to adjust for the embedded tax liability on assets held in taxable accounts. That is, it fails to distinguish between pretax dollars and after-tax dollars. Third, as explain in this study, Reed’s framework for making the asset-location decision is also wrong in that it does not recognize that the government bears some of the risk of assets held in taxable accounts.

Since investors are concerned with both after-tax risk and after-tax returns and the asset-location decision framework in group 1 studies, like Reed (2019), ignores risk it is unacceptable. The proper framework for making their asset-allocation and asset-location decisions requires that investors consider the impact of these decisions on both risk and return. The profession’s methodology for considering both portfolio risk and return is mean variance optimization.

To the best of my knowledge, all group 2 studies agree that the usual asset-location advice in a typical interest rate environment should be the following: Hold stocks in taxable accounts and bonds in retirement accounts to the degree possible, while attaining your target asset allocation. As noted, the optimal asset-location advice changes in an extremely low interest-rate environment like the one that exists today.

Dr. William Reichenstein is principal of research for IncomeSolver.com and professor emeritus investments at Baylor University. He has taught and researched in finance since 1978, with his recent work concentrating on the interaction between investments and taxes. Bill has written more than 130 articles for professional and academic journals. He is a frequent contributor to the Journal of Financial Planning, Journal of Investing, Financial Analysts Journal, Journal of Portfolio Management, and Journal of Wealth Management, and is frequently quoted in the Wall Street Journal and elsewhere. Bill earned a BA in math from St. Edward’s University and his MA and Ph.D. in economics from the University of Notre Dame. He is a Chartered Financial Analyst (CFA).

References

Dammon, Robert M., Chester S. Spatt, and Harold H. Zhang. 2004. “Optimal Asset Location and Allocation with Taxable and Tax-Deferred Investing,” Journal of Finance, vol. 59, no. 3, 999-1037.

Daryanani, Gobind. 2004. “A Different Approach to Asset Location,” in The Investment Think Tank, Edited by Harold Evensky and Deena Katz; Princeton, NJ: Bloomberg Press.

Daryanani, Gobind and Chris Cordaro. 2005. “Asset Location: A Generic Framework for Maximizing After-Tax Wealth,” Journal of Financial Planning, vol. 18, no. 1, January, 44-54.

Horan, Stephen M. 2007a. “An Alternative Approach to After-Tax Valuation,” Financial Services Review, vol. 16, no. 3, Fall, 167-182.

Horan, Stephen M. 2007b. “Applying After-Tax Asset Allocation,” Journal of Wealth Management, vol. 10, no. 2, Fall, 84-93.

Horan, Stephen M. and Ashraf Al Zaman. 2008. “Tax-Adjusted Portfolio Optimization and Asset Location: Extensions and Synthesis,” Journal of Wealth Management, vol. 11, no. 3, Winter, 56-73.

Jaconetti, Colleen M. 2007. “Asset Location for Taxable Investors,” Vanguard Investment Counseling & Research.

Kitces, Michael. 2013. “Asset Location: The New Wealth Management Value-Add for Optimal Portfolio Design?” The Nerd’s Eye View, March.

Reed, Chris. 2019. “Asset Location – Irrelevant?” Advisor Perspectives, June 26, 2019.

Reichenstein, William. 2019. Income Strategies: How to create a tax-efficient withdrawal strategy to generate retirement income. Retiree, Inc.

Reichenstein, William. 2008. In the Presence of Taxes: Applications of After-tax Asset Valuations. FPA Press, August. (The FPA Press went out of business.)

Reichenstein, William. 2007a. “Calculating After-tax Asset Allocation is Key to Determining Risk, Returns, and Asset Location,” Journal of Financial Planning, vol. 20, no. 7, 44-53.

Reichenstein, William. 2007b. “Implications of Principal, Risk, and Returns Sharing across Savings Vehicles,” Financial Services Review, vol. 16, no. 1, 1-17.

Reichenstein, William. 2006. “After-Tax Asset Allocation.” Financial Analysts Journal, vol. 62, no. 4, July/August, 14–19.

Reichenstein, William. 2001a. “Asset Allocation and Asset Location Decisions Revisited,” Journal of Wealth Management, vol. 4, no. 1, Summer, 16-26.

Reichenstein, William. 2001b. “Rethinking the Family’s Asset Allocation,” Journal of Financial Planning, vol. 14, no. 5, 102-109.

Reichenstein, William, Stephen H. Horan, and William W. Jennings. 2012. “Two Key Concepts for Wealth Management and Beyond,” Financial Analysts Journal, vol. 68, no. 1, January/February, 14-22.

Reichenstein, William and William W. Jennings. 2003. Integrating Investments and the Tax Code. John Wiley & Sons, Inc. New York, NY, January.

Reichenstein, William and William Meyer. 2020. “Using Roth Conversions to Add Value to Higher-Income Retirees’ Financial Portfolios,” Journal of Financial Planning, vol. 33, no. 2, February, 46-55.

Reichenstein, William and William Meyer. 2013. “Asset Location Decision Revisited,” Journal of Financial Planning, vol. 26, no. 10, November, 48-55.

Trout, R. Kevin. 2013. “An In-Depth Look at the Tax Consequences of Asset Location,” AAII Journal, vol. 35, no. 3, March, 26-33.

1 Most of this article comes from Reichenstein (2019).

2 Technically, the returns are tax exempt if the taxpayer withdraws the funds from the Roth at least five years after a Roth account (not necessarily this one) has been established for this taxpayer and the taxpayer is at least age 59.5. If we assume these funds are being saved for retirement then these conditions are met.

3 A few investors have made non-deductible contributions to a traditional IRA, in which case some of the principal consists of after-tax funds. In this article, I assume TDAs only contain pretax funds.

4 As explained in Reichenstein (2019) and Reichenstein and Meyer (2020), due to the taxation of Social Security benefits and income-based Medicare premiums, an investor’s marginal tax rate in retirement years may be substantially higher than the tax bracket in those years.

5 Mathematically, (1+.08(1 - 0.141))3 = (1.08)3 (1 - 0.15) + .15.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All