Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I’ve always been frustrated by the lack of clarity about what advisors earn. And then I did my own research…

Advisor pay matters

There’s lots of talk about fees and how advisors are paid, but very little about what the actual numbers are. There should be more conversations about it. Why?

What you earn matters because it is an expression of the value you create for your clients with your time.

For people who are supposed to be financial experts, I see a great deal of behavior that doesn’t make financial sense. I wish I could say that advisors are practicing what they preach in terms of managing their own financial lives, but the reality is that far too often they are not.

Examples:

- Trying to be the personal butler for impossible-to-please net-present-value negative relationships. This runs your profitability to the ground.

- Appointing successors who can’t develop new business. I see advisors in excruciating pain from this all the time. Before you sign the paperwork making an employee a partner, make sure they are going to be able to get new clients – not just rely on the ones you brought in for referrals.

- Telling your clients to have three months of cash saved in an emergency fund when your credit cards are tapped out right and left. Or when you’re so strapped for cash that you need to haggle vendors over every little expense – but yet you’re advising business owners about setting up a SEP IRA so you can manage it for 0.75%? It’s one thing if you are just starting out, but these are seasoned advisors. Imagine you go to buy a new car at the Lexus dealership and you find out the salesperson drives Toyota.

If the average advisor isn’t following his or her own advice, how seriously do you expect to be taken as a profession? You don’t think people see through that?

Sorry, not sorry.

Transparent? Hardly.

I’ve never been impressed by the so-called authorities who claim to track advisor pay data (I’ll get to the actual data in a minute). And then it hit me as to why.

- Just like our prospects, clients are confused about how advisors are paid, so are the journalists and the industry associations trying to track it.

- It’s one of the few remaining industries where you can get away with not being straightforward about what you charge before the fact. I remember one instance when I worked as a broker-deal rep and the firm said I had to present my client with a range of fees that a particular trade could cost. This breeds trust?

- It’s a highly fragmented, broad industry. According to FINRA, there are 600,000 broker-dealer reps alone. It may be hard to get data from isolated advisors who aren’t tapped into some central line of communication.

- Compensation is highly variable due to market forces.

- The industry sources that track this don’t publish the data for free. You can pay $20,000 to see the report, though!

- The data does not follow a normal distribution. There is a large cluster of small advisory firms and a large cluster of the big players. The data is highly skewed and it displays kurtosis (I’ll explain this later).

- Advisors claim to be transparent and objective on your websites. Then why aren’t your fees published on your website? Oh, I didn’t mean I was completely transparent.

The non-fiduciary cohort of the profession has an abhorrent reputation and on top of it that you are asking everyone to tell you everything about their money. How about you start by talking about yours with a modicum of transparency? You don’t think it bugs people that they have to tell you how much they earn and they don’t get to know how much you make?

The BLS data is ridiculous

I looked at what the Bureau of Labor and Statistics (BLS) had to say about what advisors make. It was nearly useless. I wrote a full blog about it if you want the full detail; here are the summary points.

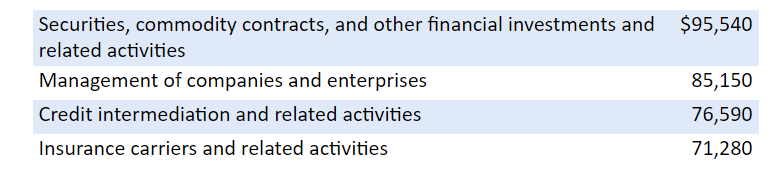

The BLS present this table below, littered with terms that are as relevant to advisor pay as what I ate this morning for breakfast.

The BLS then states, “The median wage for personal financial advisors was $87,850 in May 2019…The lowest 10 percent earned less than $42,950, and the highest 10 percent earned more than $208,000.”

The way this data is presented makes me doubt there is one iota of accuracy. I have zero confidence that what the BLS calls “personal financial advisors” lines up with how we define advisors. Is that the private banker at Chase that gets you a business credit card or checking account? Is that an RIA firm out in Omaha, Nebraska charging 1%? Is that a broker dealer rep at Merrill with $1MM in AUM?

The only way I can make sense of this is that this data tracks only what advisors make in salary – neglecting their bonuses, long-term incentives and profit sharing.

The CFA Institute is better but …

I’m a CFA® charterholder so I have access to the CFA Institute Compensation Study for 2019. I have confidence that the CFA knows what a financial advisor does, but do not think that it tracked this correctly in its survey.

Here’s what it said financial planners earned in 2018:

- Median base salary of $85k

- Median cash bonus of $30k

- Median long term incentives of $26k

- Median profit sharing/partnership earnings of $27k

The CFA Institute also tracked what they call, “individual investment relationship management,” which I believe is more akin to a private banker role:

- Median base salary of $117k

- Median cash bonus of $54k

- Median long term incentives of $27k

- Median profit sharing/partnership earnings of $25k

These numbers seem to be more accurate than the BLS, but tell me, who’s working on salary? How many advisors reading this are making only a base salary?

Red flag. It makes me doubt this is really tracking the kind of advisor we are talking about.

I saw a statistic at the bottom of the report stating the increase in salary for financial planners from 2018 to 2019 was 7.04%. In some regions, such as Asia Pacific, it was 10.5%. This is almost twice what the growth rate was for individual investment relationship management over the same period.

The CFA report said that the wealth management industry has been growing in the Americas and Asia, but shrinking in EMEA. Apparently the Swiss banking industry has been under fire due to FBAR and the Bank Secrecy Act.

This raises questions about changing compensation structures in these growth markets. I’d be curious to know if these financial planners are being paid in subscription fees, hourly, or a flat fee for financial plans. Were services bundled? I’d love to know.

Saving Athens

I feel like Theseus, the character in Greek mythology charged with saving Athens from King Minos. To do so he had to make his way through a labyrinth and slay the Minotaur. The more data I look at, the more I get stuck in the maze.

I see all these reports talking about fee compression, the average age of advisors, average client size, and how we should charge fees like Netflix. But what is this all based on?

Do we have the foundational data on which to base any of our assumptions? We should start there. But it doesn’t seem like anyone has put together a comprehensive analysis of:

- How many advisor firms there are across the entire industry;

- How many advisors there are (RIA, B/D, dual registered); and

- What advisors make.

Why is little ole me the only one asking this? Doesn’t Michael Kitces know? He seems to know a ton. Where’s the Accenture study?

**sigh**

I decided to slay the Minotaur and do my own study.

I collected data from the SEC as of July 2020 and am in the process of analyzing what was reported for all SEC registered, non-exempt entities on Form ADV Part 1A. I was hoping to have the data in time for this article, but upon analysis I found this data to be highly skewed and leptokurtic (meaning relative to the normal distribution, this data set has tails that are fatter.)

So Theseus is still wandering around in the maze – but I will slay the beast soon.

Sara’s upshot

It’s going to take me some time to study the data correctly. And as I do, I plan to share my findings in future blogs and articles and also on my podcast, which you can subscribe to here.

Sources

CFA Institute. September 2019. CFA Institute Compensation Study – Executive Summary

CFA Institute. September 2019. CFA Institute Compensation Study – Financial Planners. All Regions, All Locations, All Job Areas, All Focuses, All Seniorities

CFA Institute. September 2019. CFA Institute Compensation Study – Individual Investment Relationship Management. All Regions, All Locations, All Job Areas, All Focuses, All Seniorities

US Bureau of Labor Statistics. Occupational Outlook Handbook. Business and Financial. Personal Financial Advisors/Pay. Retrieved on July 3, 2020 from https://www.bls.gov/ooh/business-and-financial/personal-financial-advisors.htm#tab-5

Sara Grillo, CFA, is a marketing consultant who helps investment management, financial planning, and RIA firms fight the tendency to scatter meaningless clichés on their prospects and bore them as a result. Prior to launching her own firm, she was a financial advisor.

Read more articles by Sara Grillo

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.