The last decade has seen a marked reduction in the performance of systematic, quantitative value strategies, and particularly so for U.S. markets. One critique has been that the growing importance of intangibles, and the failure of the accounting system to record their value on financial statements, renders value measures anchored to current financial statements, such as book value, useless. New research shows how to address this failure.

The last decade has seen a marked reduction in the performance of systematic, quantitative value strategies, and particularly so for U.S. markets. One critique has been that the growing importance of intangibles, and the failure of the accounting system to record their value on financial statements, renders value measures anchored to current financial statements, such as book value, useless. New research shows how to address this failure.

In their 2020 study, Explaining the Recent Failure of Value Investing, authors Baruch Lev and Anup Srivastava suggested that capitalizing research and development (R&D) expenditures and selling, general and administrative expenses, and amortizing this “asset” over industry-specific schedules yield adjusted, and possibly improved, measures of book equity and earnings. Their empirical analysis suggests an improvement for value strategies using such adjustments. Data vendors (e.g., Credit Suisse, HOLT and New Constructs) are now attempting to correct for multiple limitations embedded in the financial reporting systems.

One way that academics and fund managers have tried to address the problem is to use alternative value metrics such as price-to-earnings (P/E), price-to-cash flow (P/CF) and enterprise value-to-earnings before interest, taxes, depreciation and amortization (EV/EBITDA). Many fund families (such as AQR, BlackRock, Bridgeway and Research Affiliates) use multiple metrics. Another alternative is to add other factors into the definition of the eligible universe. For example, since 2013 Dimensional has included profitability as a screen in their value funds. A third alternative is to add back to book value an estimate of the value of intangibles, such as R&D expenses.

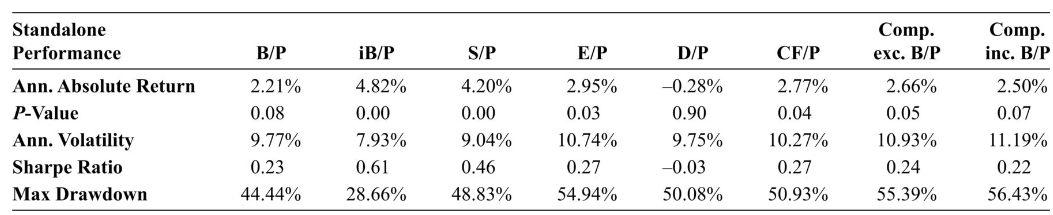

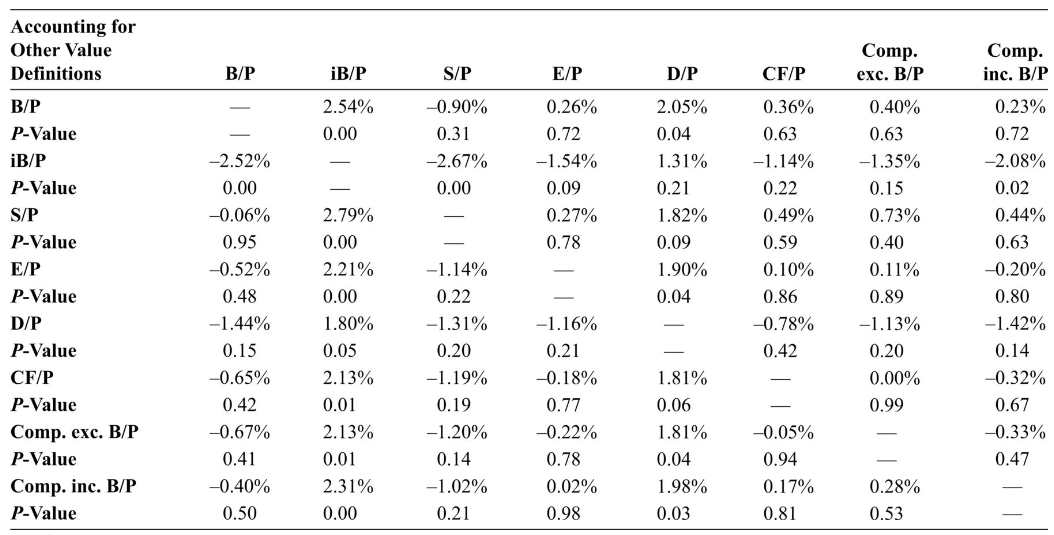

Noël Amenc, Felix Goltz and Ben Luyten contribute to the literature with their study, Intangible Capital and the Value Factor: Has Your Value Definition Just Expired?, published in the July 2020 issue of The Journal of Portfolio Management. They examined two methods of addressing the issue of the value of intangibles. They estimated knowledge capital by, “capitalizing past R&D expenses via the perpetual inventory method. For each year, the past year’s knowledge capital stock is depreciated and the current year’s R&D expenses are added to calculate the current amount of knowledge capital. Organization capital is obtained similarly. We capitalize 30% of selling, general, and administrative expenses (SG&A) expenses, assuming that the remaining 70% are expenses to generate income in the current period. For each year, these estimated values for knowledge and organization capital are added to the standard book value of equity. The amount of goodwill to be deducted is directly taken from Compustat. We refer to this alternative as the intangible-adjusted book-to-price ratio (iB/P).”Their analysis was based on annual accounting data for fiscal years January 1975 through December 2017. Following is a summary of their findings:

- Including unrecorded intangibles in the book value increases the value premium and aligns with risk-based explanations: Intangible capital exposes firms to shocks in financing conditions in the economy; firms with high organization capital are exposed to a risk of key talent leaving; talent dependency increases risk exposure to financing constraints because key talent will tend to leave financially constrained firms when financing conditions deteriorate; and knowledge capital is risky because firms may have to abandon R&D projects in times of financial stress, leading to additional losses in bad times. Firms with high capital, whether physical or intangible, are thus riskier.

- Many valuation alternatives deliver higher returns than the standard book-to-price measure. The standard book-to-price ratio delivered a return of 2.2% per year. Earnings-to-price, sales-to-price, and cash flow-to-price led to significantly positive returns ranging from 2.8% to 4.2%. Including intangible capital in the book-to-price ratio led to a return of 4.8%. Only the dividend yield factor failed to deliver a positive return.

- Other valuation ratios do not add investment value beyond picking up implicit exposure to factors other than value – metrics such as P/E, P/CF and EV/EBITDA can provide exposure to the profitability/quality, investment and low volatility factors. Thus, adding intangibles provides a diversification benefit to investors who already have exposure to those other factors.

- Including unrecorded intangibles aligns the value premium with risk-based explanations, such as: Market beta of the standard value factor is higher in bad economic times; value stocks tend to produce losses in bad times, when marginal utility of consumption is high; value stocks have more irreversible capital; and value stocks have higher operating leverage. Alternative accounting ratios often fail to align with the systematic risk exposures that were established for the book-to-price factor.

The authors’ findings of R&D being risky are entirely consistent with those of Woon Sau Leung, Khelifa Mazouz and Kevin Evans, authors of the study, The R&D Anomaly: Risk or Mispricing?, published in the June 2020 issue of the Journal of Banking & Finance. They found that R&D-intensive companies generally are, “smaller, have higher book-to-market equity ratio, better past stock performance, smaller asset growth, lower operating profitability, higher idiosyncratic volatility, lower stock liquidity, more extreme positive daily returns, greater information asymmetry, tighter capital constraints, less tangible assets and greater firm-specific human capital.” These findings are generally consistent with a risk-based explanation. The authors also provided logical, risk-based explanations for an R&D premium: “There are four risks to R&D. Technical risk is the uncertainty of the success or failure of each stage of development, which is idiosyncratic. The risk of obsolescence is that competitive firms develop faster driving future cash flows to zero, which is idiosyncratic. The third risk is uncertainty about the expected cost to completion of the project. This is also idiosyncratic, but evolves endogenously as managers learn about the probability of success as stages are completed. The final risk is uncertainty surrounding the potential cash flows from the project. Cash flows upon completion are a stochastic process and include both idiosyncratic and systematic components.”

Leung, Mazouz and Evans also found that “the R&D premium correlates positively with innovations to the aggregate dividend yield, and negatively with shocks to the default spread and risk-free rate, demonstrating the sensitivity of R&D stocks to variables that predict future business conditions. Moreover, the loadings on these three state variable innovations are significantly priced in the cross section of R&D stocks returns and even drive out size and book-to-market equity factors. These results demonstrate that the R&D premium represents significant and incremental reward for bearing intertemporal risk.”

Summarizing, Amenc, Goltz and Luyten concluded: “Our results suggest that for investors who have access to additional factors, moving from book-to-price to alternative valuation ratios or composite value definitions does not improve performance. Instead, this practice creates substantial overlap with other factors, in particular profitability. Such factor overlap tends to increase portfolio risk and reduce risk-adjusted performance for multifactor investors. Intangible-adjusted book-to-price emerges as the only alternative that provides significant benefits when accounting for other factors.” They added: “The intangible adjustment thus improves investment outcomes for multifactor investors. It also aligns closely with the risks of the standard book-to-price factor. It leads to similar countercyclical variation in market betas, and value stocks according to this definition also have higher operating leverage and earnings cyclicality than growth stocks.” That said, the improvement did not show up in the last few years.

While keeping this in mind, many investor portfolios do not have exposure to factors other than size and value. Thus, using value metrics other than P/B has provided diversification benefits and improved the returns and efficiency of the portfolio.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners.

Full disclosure: My firm, Buckingham Wealth Partners, recommends AQR, Bridgeway and Dimensional funds in constructing client portfolios.

Read more articles by Larry Swedroe

The last decade has seen a marked reduction in the performance of systematic, quantitative value strategies, and particularly so for U.S. markets. One critique has been that the growing importance of intangibles, and the failure of the accounting system to record their value on financial statements, renders value measures anchored to current financial statements, such as book value, useless. New research shows how to address this failure.

The last decade has seen a marked reduction in the performance of systematic, quantitative value strategies, and particularly so for U.S. markets. One critique has been that the growing importance of intangibles, and the failure of the accounting system to record their value on financial statements, renders value measures anchored to current financial statements, such as book value, useless. New research shows how to address this failure.