Is the Bond Market as Disconnected from Reality as the Stock Market?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Everybody is wondering how the stock market can be so high while the U.S. economy is so low. But you don’t hear the same rumbling concerns about the bond market – even though something very similar to ultra-high P/Es is going on in the fixed income side of your portfolio.

Everybody is wondering how the stock market can be so high while the U.S. economy is so low. But you don’t hear the same rumbling concerns about the bond market – even though something very similar to ultra-high P/Es is going on in the fixed income side of your portfolio.

Recently, the Barclay’s AGG index, which is the most common index tracked by ETFs, was yielding roughly 1.07% with a duration of six years – meaning, in layperson’s language, that if interest rates were to rise 1%, the ETF investors would lose 6% in price terms. This is a horrible risk/return profile.

But what are your alternatives for the fixed income segment of client portfolios?

Recently, I moderated a discussion with three professionals who constantly monitor the bond market from very different angles. Part of the conversation took place in a webinar, part of the Insider’s Forum conference’s “Three for Free” summer series. The rest of it came in preparation and supplemental interviews.

How different were the perspectives? The conversation included Eddy Vataru, chief investment officer of the total return strategy and portfolio manager at Osterweis Capital Management in San Francisco. Vataru worked with the Treasury Department in 2008-9 on its TARP program, trying to help stabilize the mortgage market while working as a senior staffer at Barclays Global Investors (now Blackrock), so he has seen the stimulus efforts from the inside and closely follow the Fed’s ever-ballooning QE programs. Vataru’s sector rotation investment strategy involves constantly evaluating the spreads at every point in the yield curve among corporates, Treasury bonds and agencies (mortgage debt), to identify sweet spots as they arise while watching the big picture developments in the overall economy.

Vataru’s portfolio, in contrast to the Barclay’s AGG index, is currently yielding roughly 2% with a duration of about three years – 50-75 basis points higher than the index, with about half the duration.

Also part of the discussion: Venk Reddy, chief investment officer and portfolio manager at Zeo Capital Advisors in San Francisco. Reddy invests in short-term high-yield bonds, which primarily requires him to avoid credit risk – very much like stock analysis to determine which companies are positioned to pay their bondholders.

Reddy’s portfolio is currently yielding just over 6%, with a 1.5 year duration.

Finally, the conversation included Jason Stuck, senior managing director and head of portfolio management at Northern Capital Securities Corporation in Boston. Stuck created a service at Northern Capital which helps advisory firms buy individual bonds (U.S. corporates and munis, predominately), either for individual clients or as sleeves in model portfolios. The service includes defining the goals of the portfolio, and modeling the performance of a proposed bond mix over the next 1, 2 and 3 years if interest rates were to rise 1%, 2% and 3%. The firm will then identify the best-priced individual bonds and buy them on behalf of the advisory firm at a disclosed 10 basis point fee. (If the bond yield is 3.10%, the yield to the client would be 3.00%.)

Northern Capital’s advisory firm clients tell Stuck that their clients want the fixed income segment of their portfolios to act like bonds, which means that if they hold the bonds to maturity, they know precisely the return they’ll be getting.

The Fed put

Vataru set the stage with a big picture assessment of our current investment environment, and his view is that the Fed is propping up and driving the bond market.

“Back when we were working on the TARP program,” he says, “the intention was to stabilize the markets and maintain functionality. QE-1 kicked in in January 2009, and that was really more intended to impose the Fed’s will in terms of where rates should go, and to try to achieve an outcome that was beyond stabilizing the market.” The goal was to put a floor under bond prices, which benefits investors.

“What’s interesting about this mandate in today's QE-4,” Vataru says, “is that it has a little bit of both. On March 15, when the Fed cut rates to zero, it announced only $700 billion in Treasury purchases. But it went on to buy 3-4 times what it said it was going to buy, and the purchase of corporate bonds and corporate bond ETFs is a little bit different from what we’ve seen before.

“What has been amazing about this particular rendition,” Vataru continues, “is that in four months, it has already purchased what they bought, in terms of size, in the first three QE programs. The Fed balance sheet is around $7 trillion right now – a $3 trillion expansion over where we were just a few months ago. It’s pretty stunning.”

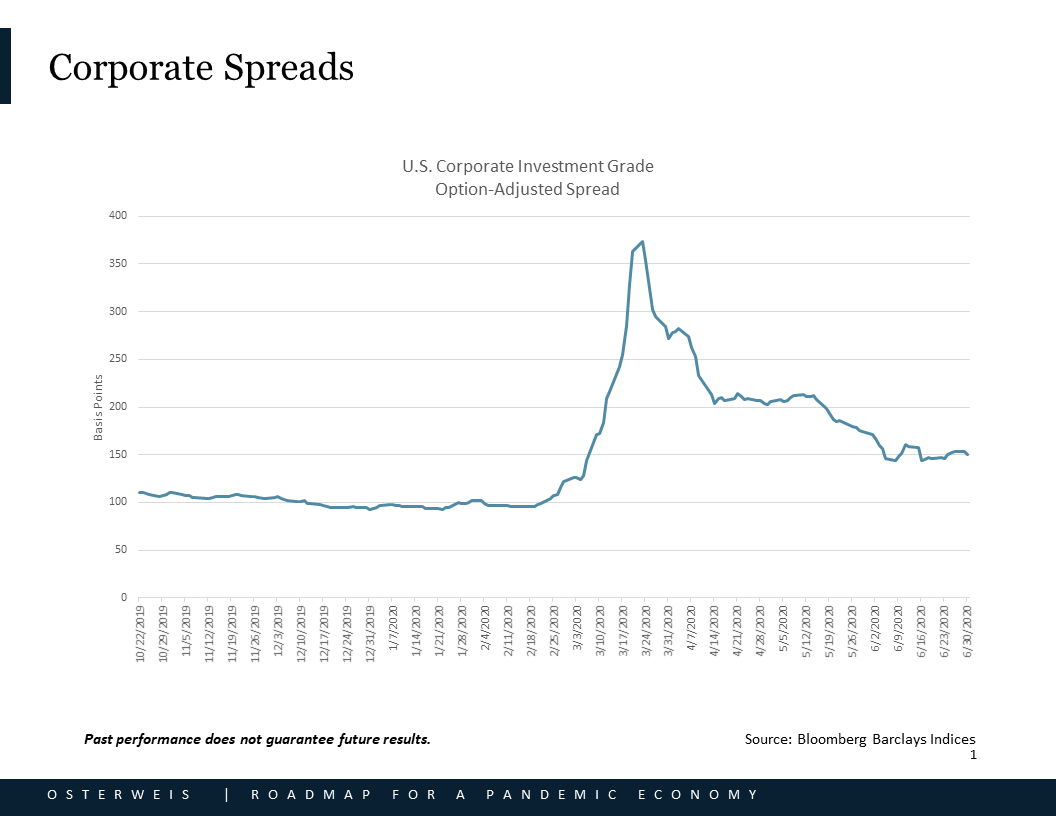

What are the implications? Under prior QE programs, when the Fed was buying Treasury securities and mortgages, the rest of the market was able to make profitable investments all across the risk spectrum. Vataru believes that this time the Fed action has also boosted stock returns, making it seem as if corporations are invincible to the savage COVID forces. Vataru offered the audience a slide that showed how the spreads between Treasury yields and corporate bonds have widened across the board. “The very widest point that we saw was actually March 23,” he says, “which was the day the Fed announced that they were going to be buying corporates in addition to the Treasury bonds and mortgages that they had already announced.”

Corporate bonds have moved back to pre-COVID value levels. “That’s pretty stunning,” says Vataru, “when you think about the fact that we haven’t solved for the virus, we don’t have a vaccine, we don’t have any therapeutics, and we have some pretty listless companies now whose business models are quite compromised as they navigate the patchwork of shutdowns we’ve had nationwide. The injection of liquidity has really helped bolster asset prices, very specifically corporate bonds, but also mortgages, and to some extent Treasury yields as well.”

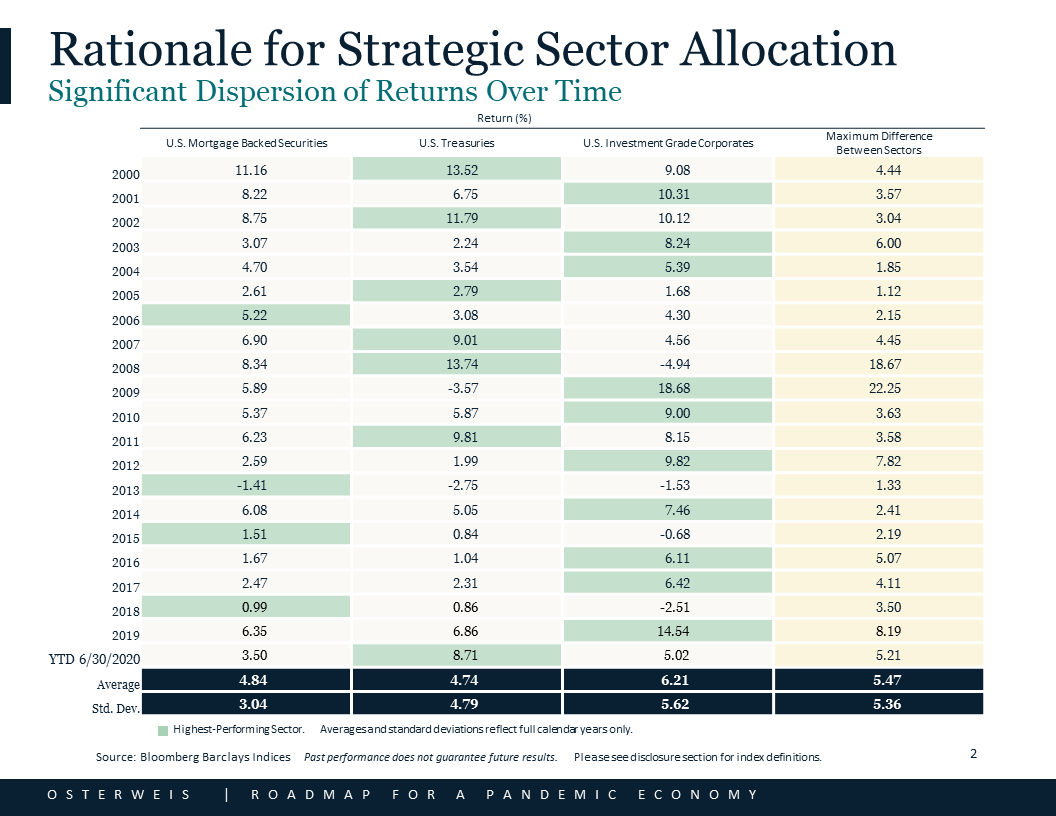

Vataru touched on sector rotation, and showed a slide that illustrated how different areas of the fixed income market take turns offering the highest returns.

Regarding today’s market environment, he noted that corporates, Treasury securities and mortgages all carry different risks, and are thus less correlated than most lay investors imagine. Corporates come with default and liquidity risk, mortgages have liquidity and prepayment risk, while all (including Treasury securities) carry interest rate risk.

But these dynamics are somewhat inverted today. Vataru noted that the Fed’s intervention has basically taken away any liquidity risk, which means default risk is the primary concern in corporates, and the risk in mortgages is related to that of borrowers pre-paying or refinancing their loans.

What is Vataru overweighting now?

“At the moment, I like mortgages the most,” he says. “We don’t know how the pandemic is ending,” he adds, “and one thing about owning an agency mortgage is, you have some prepayment risk, but it is not real homeowner risk, since Fannie Mae, Freddie Mac or Ginnie Mae are going to make you whole in any delinquency related to ability to pay. Mortgages today are a good sleep-at-night sector,” he adds, “and one with less interest rate sensitivity than the other two.” Plus, of course, you are getting roughly quadruple the return you would get by owning comparable-maturity Treasury bonds.

Reddy agreed with Vataru, but said that he worries that what the Fed is trying to do has been misinterpreted by the markets. “The market has interpreted the Fed buying as a Fed put,” he says. “Investors are saying to themselves, the Fed is not going to let anything go bad, and they think [the buying] has taken away a lot of risk.”

Reddy notes that the central bank's response is similar in this crisis to what it was in 2008-9, but he says that the economic challenge is very different. “Unlike 2008-9, the challenges in this environment are not financial system challenges,” he says. “They are more directly related to the underlying fundamentals in the economy. I think whatever the Fed does, the fiscal policy component, what Congress and DC does, is a much bigger piece of the solution that we’re trying to figure out here, than simply shoring up the financial system.”

Investors, because of their prior experience with the various QEs starting in 2008, have misinterpreted the Fed’s massive liquidity infusion as a free pass in the marketplace. When Reddy looks at the underlying damage to businesses and corporations, the unemployment rate and the other aftermaths of COVID, he sees other risks that “are not being properly factored into the pricing in the markets as a whole.”

Chief among these, of course, is default risk. “In 2009, corporate bond defaults were pushing 10%,” he says, adding that if this happens again, index investors will take their proportional share of losses. “If you buy the index, you are buying the good, the bad and the ugly. You are not necessarily concentrating on those stronger fundamental names.”

Is there a better way to come out unscathed? “When you do the fundamental work that we aim to do, you’re looking for resilience factors,” says Reddy. “You’re looking at business models and management teams, cash flow and reasonable levels of leverage.”

Beyond that, a savvy bond investor is trying to understand the difference between companies that are temporarily versus permanently scarred by COVID-related breakdowns. “Is this going to be a factor for the long term, or a one-time cost?” says Reddy. “It’s not unlike somebody has savings and they lose their job, but they get another job. The period of time between jobs is a one-time cost. It’s not great, but you can replace it. But it’s different if you lose your job and there isn’t any demand for you in the marketplace; it represents a permanent loss of income.”

Reddy offered some examples of companies that were able to issue debt and raise capital in order to shore up liquidity – and boost resiliency in the process. Yum! Brands, which owns fast-food companies (KFC, Pizza Hut, Taco Bell), raised debt at high interest rates in order to buy some of its ailing franchises. “It’s a strategy that could earn high returns on that money in excess of debt,” says Reddy. “And then in two years, if things are normalized, they can refinance the debt and lower their cost of capital.”

United Airlines is another example. “They just issued debt that was secured by their MileagePlus program,” Reddy explains. “Their loyalty program actually gets cash in times like this, when people cancel tickets they bought with miles and they don’t actually have to pay for that ticket.”

Binary versus diversified

What about the muni bond market, where Stuck is buying and selling on behalf of advisory firms? There’s a lot of talk about unfunded pension liabilities, and not long ago the Senate majority leader floated the idea of states declaring bankruptcy. Isn’t this a market to avoid altogether?

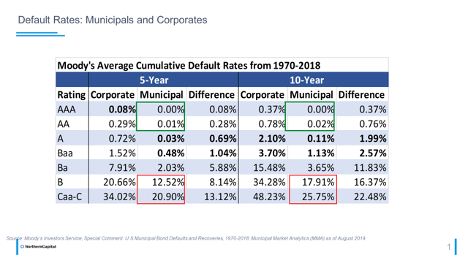

“The media likes to take a special project or a housing project and make an example of it, and create fear that everything is a disaster and the market is going to fall apart,” says Stuck. “But historically, the default rate among muni bonds has been very low,” says Stuck. He cites a study by Moody’s (see below) looking at municipal bond defaults from 1970 through 2018, which found that the default rate for AAA-rated muni bonds was zero, and for AA-rated paper it was 0.02%.

But this is a different environment, isn’t it? “It’s always important to look at the credits,” says Stuck. “As bond holders, we want to know, how are we getting paid? Is it some kind of special tax? Or is it a general obligation bond, where we get compensated when everybody pays their real estate taxes?”

Stuck says that comparing munis to corporates is wrong. “With a corporate bond, it’s binary,” he says. “You’re either going to get paid or you’re not. Whereas if I buy a general-obligation muni bond, I’m expecting tax revenues from everyone who resides in that area. If you think about the risks, it’s much more diversified.”

But what about returns? The yields move around a bit day to day, week to week. But at the time of the webinar, 10-year Treasury bonds were yielding about 54 basis points, while AAA-rated 5% coupon munis were trading at a 1.08% yield. “You’re getting double the yield from an AAA-rated muni compared to the Treasury,” says Stuck, “and you get the tax benefits on top of it.”

Shifting rates

We started the conversation with the increasingly unhappy risk/reward ratio of the Barclay’s AGG – and Stuck says that the same concerns about the indices are generally true in the municipal market. Experienced bond investors concede that buying the index was a generally winning strategy for the past 11 years, as money flowed into index ETFs and passive funds, and they were net buyers.

But even during the best of times for the indices, managers and individual buyers could take advantage of the fact that, during times of volatility, the huge passive investment funds would become forced buyers and forced sellers. “In March, when we saw an extreme selloff from the early stages of the pandemic,” says Stuck. “We ended up with some incredible opportunities to pick up very high-quality bonds at very cheap prices.”

Reddy has talked previously about how a patient buyer in his high-yield sandbox could pick up an extra 100 basis points of yield simply by waiting for times when the index funds and ETFs were required to sell into a market with few buyers. “It’s just the natural friction of volatility,” he says. “If you have to lift offers because you have inflows, and the next day you have to hit bids because you have outflows, you’re paying that bid/offer spread. And what’s unfortunate,” he adds, “is that investors who are sticking around in that ETF or index funds are the ones who have to pay that.”

Managers and individual buyers, he says, have the luxury of not having to transact on a given day. “In markets like this, it is nice to be able to be cautious and to take advantage of the fact that we are not forced to put money to work on any given day, and really pick our prices,” says Reddy. “If tomorrow is a better day to deploy capital, we can be patient.”

Vataru notes that index yields have been dropping for decades. “Now you’re left with an index which, as a passive investor who is not able to pick winners and losers in a very uncertain environment, bonds are pretty difficult to like,” he says.

What about interest rate risk? Are we are finally nearing the end of the long bull run in fixed income? Vataru says that his main worry is that the markets will do what they did in 2013, during the so-called taper tantrum, when the 10-year Treasury rose 100 basis points almost overnight, and everybody in fixed income was looking at negative returns. “There wasn’t even an actual taper,” he says. “It was just a worry that there was going to be one.”

Today, with the Fed pouring money into the market, investors who believe in the Fed put might suddenly realize that this buying spree will someday come to an end. At best, the markets might return to normal valuations, which alone would not be pretty. “When we look at rates now and compare them to other asset classes,” says Vataru, “the 10-year Treasury yield just sticks out as something that is probably 100 basis points lower than it otherwise would be, if you look at where the equity and other markets are today.”

Reddy says that an active participant in the bond market will typically fluctuate between offense and defense depending on the underlying economic fundamentals – something that passive investors don’t have the luxury of doing. “Traditionally,” he says, “fixed-income has an ebb and flow. Rates go up when things are really good, and it’s good to own duration because, when things reset and rates come down, and you’re in a situation like we’re in now, you can rotate to credit. And then,” he adds, “over time, there is a rotational shift back to duration, and so forth. This,” says Reddy, “is a time to buy cheap, not to buy everything, and it’s a time to focus on security selection, a time to tilt toward paying attention to credit risk and away from duration risk.”

Doesn’t his fund always keep duration low? “That’s how I manage,” says Reddy. “In general, it is easier for me to wrap my head around whether a company is fundamentally strong than it is to figure out which direction interest rates are going to go – even in the asymmetries in the market right now.”

Northern Capital, meanwhile, mitigates interest rate risk by defining exactly how the mix of corporate and muni bonds will behave as interest rates move up or down. “Most of our advisor clients want to protect against a move to higher rates,” says Stuck. Instead of bond ladders, where the portfolio is invested equally in maturities and reinvests accordingly, the portfolios might have several short-duration bonds and a number of longer-duration bonds, taking advantage of inefficiencies in the yield curve. “The key with interest rate risk, with many advisors,” says Stuck, “is that clients are protected from the worst case scenario, and that they don’t get hit with unexpected losses.”

Negative rates?

One question on the minds of advisors is: Will the U.S. follow Japan, Switzerland, Denmark, Sweden and Spain in issuing Treasury securities at negative nominal rates? This is another way of asking: is the bull market in Treasury bonds, which has seen 10-year yields drop from nearly 16% in the early 1980s to below 1% today, finally at its logical conclusion? Or do Treasury rates have a few percentage points yet to go?

Vataru says it’s highly unlikely that Treasury yields will ever go below 0%. He doubts that the Fed would undermine the thriving U.S. money market fund business, which is more robust than Japan’s or Europe’s. “But the bigger issue is the mortgage market,” he explains. “We have a third of the AGG index in this asset class that is extremely efficient at bringing duration in supply when rates hit local lows. You can see that refi ad on TV. When that happens, whether it is through purchases or refis, it actually brings a lot of duration to market that investors need to absorb.”

He says the Fed is absorbing a lot of these bonds. “They are buying about 40% of the mortgage origination market that is happening right now, on a daily basis,” says Vataru. “If they were committed to seeing rates go to zero or below, that means that mortgage spreads would have to widen dramatically and be the best buy in the history of the universe, or mortgage rates would go to zero, which would create such a swoon of duration that it is unrealistic to fathom it. This is a part of the U.S. market that you don’t see in Europe or Japan. They don’t have a residential mortgage market that brings duration as efficiently as we see it in the U.S.”

Vataru cautioned that this doesn’t mean the 10-year Treasury cannot go negative on a trade. “That trade might be part of the greater fool theory, that rates might go even lower on a momentum trade,” he says. “But the reality is, fundamentally, it’s very difficult to see rates in the U.S. go negative.”

Biggest fears

So what are the panelists most worried about in the bond market? “This is not a fear for August of 2020,” says Vataru, “but I most worry about the normalization trade, longer-term.”

Meaning? “What happens when things go back to normal?” he says.

“We are looking at markets that have obviously been buoyed by a tremendous amount of stimulus. But eventually the Fed is going to take away the punch bowl.” Vataru notes that the Fed seems to be extremely concerned that the markets will experience another taper tantrum. “That’s why the Fed announced that they are committed to buying Treasuries and mortgages through the end of 2021,” he says. “They don’t want a repeat of what happened in 2013, when more folks were worried about what was going to happen than what was going on then. But I think we all know, someday, we will have a day of reckoning when this is all over.”

Reddy is most concerned that the consensus expectations might be off base. “The general assumption in the marketplace,” he says, “is that at some point, one way or another, we’re going to get our arms around this pandemic, and things will return to normal in a year or so.” But, he adds, “What happens if the search for a vaccine doesn’t work? Or it doesn’t last long enough? What if we have to live with this virus for a long period of time?”

Investors, says Reddy, are engaging in temporary risk avoidance, waiting until things return to normal. “If the consensus is wrong,” he says, “then things are going to get really bad before they get better, and we’re going to be in a constant stage of managing risk. If you want a scenario that keeps you up at night, that is one thing that keeps ME up at night.”

Stuck worries about investors who might be tempted to reach for yield in a market that offers little extra return for the risk they might be taking. He says that the key to navigating the future is to pay attention to fundamentals.

“There’s good debt and there’s bad debt,” he says. “For the companies that are taking on new debt to pay off old debt, and reduce their costs, it is a good strategic move. Everybody is going to take a hit in this environment; it is going to be stressful and painful due to the pandemic,” he says. “But we just have to make sure we are not reaching for yield with a company where we are not quite sure about their finances.”

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits