Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The number of coronavirus cases in the United States has eclipsed five million and the U.S. economy is mired in its deepest recession since the end of World War II. To combat the crisis, Congress passed the largest fiscal stimulus package in history and is in the later stages of negotiating another round. Preliminary estimates put the total price tag of already enacted stimulus somewhere in the neighborhood of $6 trillion dollars.

That’s twelve zeros.

In response to this unprecedented fiscal stimulus, investors have turned to perceived “safe havens”, specifically gold, to hedge their portfolios against the prospect of runaway inflation. But does history support this belief? And what should advisors be thinking about for client portfolios?

Does gold hedge inflation?

Contrary to popular belief, the data clearly shows that gold’s track record as an inflation hedge is spotty

Nor has it been a reliable store of value.

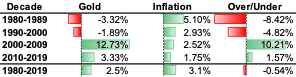

Exhibit 2: Gold versus inflation by decade, 1980-20191

Consider the early 1980s. If ever there was a classic textbook case for owning gold, it was then. Inflation peaked at 12.4% in 1980. For the decade of the 1980s, inflation averaged 5.1% annually. Yet gold returned -3.32% annually from 1980-1989. When an inflation hedge was needed most, gold underperformed by nearly 8.5% per year for the decade; an investor buying gold at the end of 1979 saw its value decline nearly 30% by the end of 1989.

And things didn’t get any better during the 1990s

Gold’s decline continued, underperforming inflation by 5% annually from 1990-1999. It wasn’t until the mid-2000s that gold finally began to catch up and deliver positive returns to investors; it would take 26 years – until January 2006 – for investors buying gold at the end of 1979 to see a positive return on their investment.

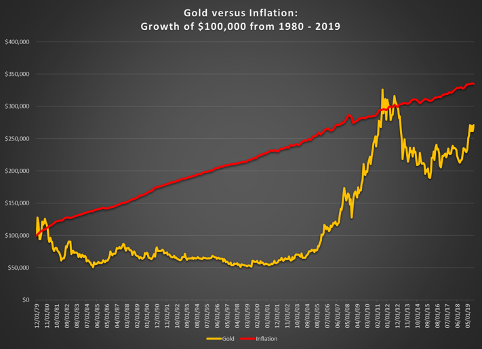

Exhibit 3: Gold versus inflation: 1980-20192

Consider the global financial crisis, when gold delivered the best returns in our 40-year sample period. Let’s assume an investor timed it perfectly and invested in gold in early 2008, just as the crisis began to unfold but before the Fed began to dramatically expand its balance sheet. For the five-year period from 2008-2012, gold returned a staggering 14.94% annually while inflation averaged just 1.80%.

Does this cherry-picked, five-year time horizon from 2008-2012 make the case for gold as an inflation hedge? Only if we ignore gold’s track record both before and after that window. Upon closer examination, the 10-year period from 2008-2017 includes two very different experiences for gold investors: While gold returned a staggering 14.94% from 2008-2012, gold returned a pitiful -4.85% annually from 2013-2017. Subsequently, if an investor was late to the game and added gold at the end of 2012 (but before the most aggressive QE), their returns were considerably worse for the remainder of our crisis period.

Finally, on a more practical level, how many investors in 2008, given how horribly gold underperformed inflation since 1980, believed it would outperform inflation going forward? From 1980-2007, gold returned 1.49% annually versus 3.80% for inflation. Subsequently, any decision to invest in gold in early 2008 would have relied on something other than gold’s historical track record relative to inflation.

Is gold a reliable store of value?

A related claim is that gold is a reliable store of value. But the data tells a very different story.

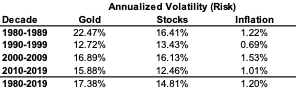

Over the past four decades, gold has been more volatile than stocks. From 1980-2019, the volatility of gold exceeded stocks. Gold was more volatile than stocks in three of the past four decades and had a volatility only marginally less than stocks during the decade of the 1990s. Subsequently, there is zero evidence that gold is a reliable store of value; at least not any more than that of a portfolio of stocks.

Exhibit 4: Annualized volatility of gold, stocks, and inflation, 1980-20193

Advice for advisors and your clients

Keep three things in mind when discussing gold and inflation with clients.

Put gold in context relative to other asset classes. Every decision you make to own something is a decision to not own something else. There are opportunity costs to including all assets in a portfolio; this is especially true of gold, given its high volatility and poor returns relative to inflation. There are other asset classes better suited to hedge inflation (like stocks or TIPS) that have much better long-term expected returns.

If you decide to include gold (or any hedge) in client portfolios, ask yourself whether the amount you’ve allocated will have a meaningful impact on hedging a portfolio or specific cash flows against inflation. Most portfolio allocations to gold are far too small to have a material impact on either. Most advisor portfolios that I see in the RIA space have gold allocations in the 3% to 7% range. Is that enough to have a material impact on client portfolios or financial plans? Of course it isn’t; any decision to increase gold allocations beyond a token amount has serious opportunity costs given gold’s poor risk/return profile.

So why own it?

Finally, try to hedge inflation over time, not every time. If the notion of increasing or decreasing portfolio withdrawals every month (or even every year) to adjust for CPI sounds foolish, then so is trying to hedge the purchasing power of those cash flows on a monthly or annual basis. Think longer-term; if you don’t think long-term, your clients won’t either.

Donald Calcagni is chief investment officer of Mercer Advisors. Mercer Advisors Inc. is the parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. Content, research, tools, and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. Past performance may not be indicative of future results.

1 Source: FactSet, Inc.

2 Source: FactSet, Inc.

3 Source: FactSet, Inc.

Read more articles by Donald Calcagni

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.