The data used to measure a company’s compliance with environmental, social and governance (ESG) guidelines is inconsistent and leads to misleading results. Moreover, when teams at the same company manage comparable ESG and non-ESG funds, the former more often underperforms the latter.

The data used to measure a company’s compliance with environmental, social and governance (ESG) guidelines is inconsistent and leads to misleading results. Moreover, when teams at the same company manage comparable ESG and non-ESG funds, the former more often underperforms the latter.

The popularity of sustainable (ESG) investing has led to increased attention from researchers. Mark Anson, Deborah Spalding, Kristofer Kwait and John Delano contribute to the literature with their study, The Sustainability Conundrum, which was published in the March 2020 issue of The Journal of Portfolio Management.

They began by noting that “sustainability or ESG is a very broad term that is interpreted in many different ways by many different investors.” This leads to problems in definitions and wide dispersions in ratings of the same companies. Their findings led them to conclude that the data regarding sustainability and ESG rankings are inconsistent and hinge on the application and interpretation of different ranking systems using different factors with different weights on those factors – the available ESG data does not provide clear guidance on which companies are delivering superior environmental results.

Next, they devised a closed-loop experiment to identify whether sustainable investing adds or subtracts value. They identified 24 asset managers in which the same fund company, and the same portfolio team, managed two comparable funds –portfolios with and without constraints using sustainable metrics. They stated: “This is as close to a scientific experiment as we can devise to determine whether there is an advantage or disadvantage to sustainable investing.” They added: “The choice of sustainable data source is not an input for our analysis or conclusions. Last, we do not need to worry about the choice of benchmark, because the active manager is competing against itself.”

They found:

- More managers earned lower returns when pursuing a sustainable mandate or when applying sustainable metrics: 13 managers with negative returns and 11 managers with positive returns.

- The negative alpha of those managers that generated negative returns was larger than the positive alpha generated by those managers with positive returns.

- The average alpha generated across the full sample of managers was almost -1% and was statistically significant at the 5% confidence level (t-stat of -2.01). (But the sample is small.)

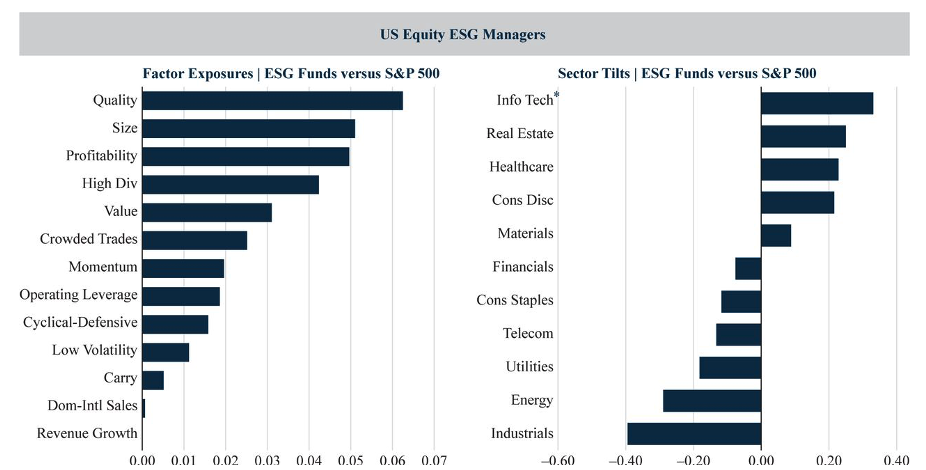

They next looked to see if they could draw conclusions regarding differences in factor exposures (risks). They found:

- ESG active equity managers load up on quality, size, profitability, high dividend, value, low volatility and momentum.

- ESG managers typically do not invest in companies that have low volatility or high operating leverage, or that are defensive in nature.

- Technology is the largest industry overweight in ESG portfolios. Other sectors that are over-weighted are real estate, healthcare and consumer discretionary.

- ESG managers underweight utilities, energy, financial, consumer staples and industrials.

Source: Commonfund and Bloomberg US Equity Funds Universe

Summary

Anson, Spalding, Kwait and Delano summarized their findings, noting that there are many challenges with sustainable investing, including databases that purport to rank companies along sustainable qualities, but apply different metrics to measure those qualities. That leads to considerable dispersion in ranking public companies with respect to sustainable attributes. Those inconsistencies lead to inconsistent conclusions about which companies are green versus gray, which in turn leads to confusion about how to construct ESG portfolios.

Consequently, this leads to inconsistent empirical results that feed the ongoing debate about whether sustainable investing adds value to or subtracts value from an investment portfolio. In their attempt to resolve the debate over the value of sustainable metrics embedded in an investment portfolio, their “closed loop” experiment identified a negative alpha associated with sustainable investing. This is consistent with economic theory that if a large enough proportion of investors choose to favor companies with high sustainability ratings and avoid those with low sustainability ratings (“sin” businesses), the favored company’s share prices will be elevated and the sin stock shares will be depressed. Specifically, in equilibrium, the screening out of certain assets based on investors’ taste should lead to a return premium on the screened assets. They did add a caution because the results were based on a small sample.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners.

Read more articles by Larry Swedroe

The data used to measure a company’s compliance with environmental, social and governance (ESG) guidelines is inconsistent and leads to misleading results. Moreover, when teams at the same company manage comparable ESG and non-ESG funds, the former more often underperforms the latter.

The data used to measure a company’s compliance with environmental, social and governance (ESG) guidelines is inconsistent and leads to misleading results. Moreover, when teams at the same company manage comparable ESG and non-ESG funds, the former more often underperforms the latter.