Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Market crashes, such as we experienced in March at the onset of the pandemic, drive assets to the safe haven of government bonds. But our research shows this flight to safety mindset did not translate to an increase in demand for annuities.

The recent drop in annuity demand during the COVID-19 market turbulence is a mystery. Older Americans gravitated away from investment risk. Using a survey of older respondents conducted after the March market crash, we find evidence that there is a dissonance between those who understand what annuities do and those who value guaranteed lifetime income.

The annuity puzzle cannot be solved without educating those who value annuities the most.

The American College conducted an online retirement literacy survey through Greenwald & Associates in late April and early May on behalf of The New York Life Center for Retirement Income. The goal was to ascertain knowledge and attitudes about retirement income planning and financial products among 1,931 individuals approaching or in retirement (age 50-75) with at least $100,000 of non-housing wealth. The survey included a number of questions about annuities that assessed knowledge, gauged interest in guaranteed income, and evaluated whether the recent market turbulence increased demand for income security.

Annuity demand fell during the pandemic. This is surprising because older investors prefer less investment risk after market drops – a phenomenon we’ve documented in prior research. Since the demand for equities declines in times of higher market volatility, we expect that demand for “safe” assets to increase. Income annuities are perhaps the safest retirement assets, because they generally invest in bonds and protect against longevity risk.

So why didn’t demand for annuities go up after the March market crash?

In order to make good decisions about buying annuities, an individual needs to have a basic understanding of the product. Annuity knowledge was among the lowest of all surveyed retirement literacy areas. For example:

- 19% correctly guessed that the payout on a single-premium immediate annuity (SPIA) to a 65-year old male was about 6% and not 10% to 15%;

- Only 23% knew that SPIAs were more expensive for younger buyers; and

- Only 12.6% correctly answered that a VA with a GLWB rider continued to make income payments when the investment account falls to zero.

Only 1.5% got all three annuity questions right and 9.8% answered two questions right. The majority (58.1%) didn’t get any of them right. This is worth keeping in mind when judging a client’s ability to grasp the value of an annuity or even the effectiveness of product disclosures to an average buyer who has no idea what an annuity is all about.

Who had the highest annuity knowledge scores? When we ran a regression predicting the total three-question score, the significant predictors were being male, older, having financial assets more than $500,000 and having a college education.

When we asked people if they were interested in a financial product that provides lifetime income or whether guaranteed monthly income is important, we got a completely different profile.

On a scale of 1-7, where 1 is not at all important, 4 is moderately important, and 7 is extremely important, 68% felt that having a guaranteed monthly income source is either a 6 or a 7. Another 26% ranked guaranteed income of moderate importance or slightly higher. Only 6% ranked guaranteed income less than moderately important.

When we ran a multivariate analysis to predict which respondents would think guaranteed income is “extremely important,” we found that women, respondents without a college education, non-whites, and those with less wealth placed the greatest value on lifetime income. It is clear that retirees who are the most economically vulnerable placed the greatest value on the guaranteed lifetime income that can be provided by an income annuity.

Earlier in the survey, we asked, “How interested are you in owning a financial product that guarantees you (and your spouse/partner) with a certain amount of monthly income for the rest of your life?” Interest in a financial product that provides a source of guaranteed monthly income is more tepid than interest in the guaranteed income that the product provides. Only 16% were extremely interested in a guaranteed income product (compared to 46% who felt that a guaranteed monthly income source was “extremely important”).

Annuity products are less valued than the services they provide. This is a problem for annuity manufacturers. Consumers still don’t see a financial product as the solution to receiving what they clearly want – a guaranteed lifetime source of income. When we ran an analysis on predictors of demand for a lifetime income product, we found that education and wealth are negatively associated with interest in the product. This isn’t great news for insurance companies.

However, one variable is strongly associated with interest in a guaranteed lifetime income product: Near-retirees who are still working full time. The percentage of workers in their 50s and 60s who will receive lifetime income through an employer pension is far lower than for post-Boomer retirees in their 70s and 80s. Workers nearing retirement are feeling the anxiety of not knowing if they have enough to sustain their lifestyle in retirement. This lack of clarity is driving a far higher demand for a product solution to guaranteed income among those who won’t be able to rely on a pension.

The importance of clarity provided by guaranteed income is borne out by responses to this question: “Which do you think is the most helpful in terms of planning for retirement?” Answers included, “an estimate of how much money you will need to save for retirement,” “an estimate of what your expenses will be in retirement,” and “an estimate of how much monthly income in retirement you would receive based on your current level of assets.” Respondents answered “monthly income” at nearly twice the frequency of savings or spending needs. People want to know how much they can safely spend in retirement.

Did COVID-19 increase demand for annuities?

We wanted to better understand how the shock of a combined health and financial crisis impacted respondents’ willingness to take investment risk and their demand for the income security of annuities. Our survey results showed that while demand for guaranteed income increased, it did so at a lower rate than the interest in taking less investment risk. For example, while 38.6% of survey respondents were less comfortable taking investment risk (and 4.8% were more comfortable), only 19.1% were more interested in guaranteed income (while 6.3% were less interested). Respondents working with a financial advisor and those with higher stated levels of risk tolerance were the most likely to express increased interest in guaranteed income.

Overall, these findings show that interest in guaranteed income has risen lately – which is not surprising given the higher level of market volatility (and the increased demand for safe assets). What is surprising is the most risk-tolerant respondents exhibited the greatest increase in demand. This suggests that investors (and households) not previously interested in exploring additional guaranteed income (i.e., delaying claiming Social Security benefits and purchasing an annuity) may now be interested in those products.

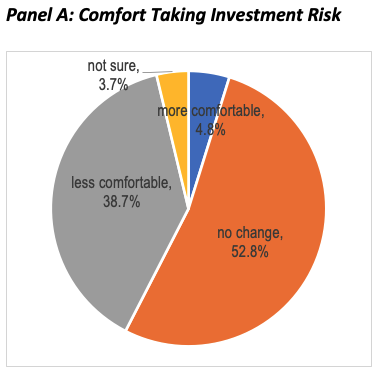

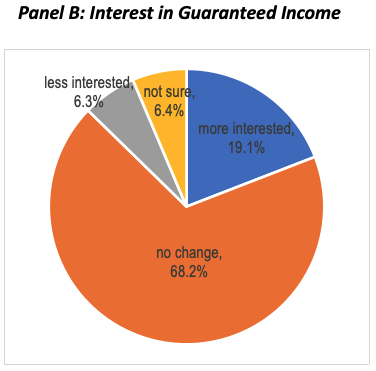

To assess changes in risk and annuity preference, we asked, “How has the coronavirus (Covid-19) crisis and subsequent market downturn impacted the amount of investment risk you are willing to take?” Responses included, “more comfortable taking investment risk now,” “no change,” “less comfortable taking investment risk now,” and “not sure.” We also asked, “How has the coronavirus (Covid-19) crisis and subsequent market downturn impacted your interest in owning a financial product that guarantees you (and your spouse/partner) with a certain amount of monthly income for the rest of your life?” The four possible responses were, “more interested now,” “no change,” “less interested now,” and “not sure.”

The pie charts below summarize the respondents’ interest in taking investment risk (panel A) and in guaranteed income (panel B) given the coronavirus (Covid-19) crisis and subsequent market downturn:

There is a notable reduction in the desired investment risk level, with 38.7% being less comfortable and only 4.8% being more comfortable. This is consistent with our expectations that older respondents have become increasingly risk averse given market movements. Even with older investors wanting less investment risk, this didn’t translate into a spike in interest in guaranteed income. Only 19.1% of respondents were more interested and 6.3% less interested, for a net change of 12.8% (vs. a 33.9% net change in taking risk).

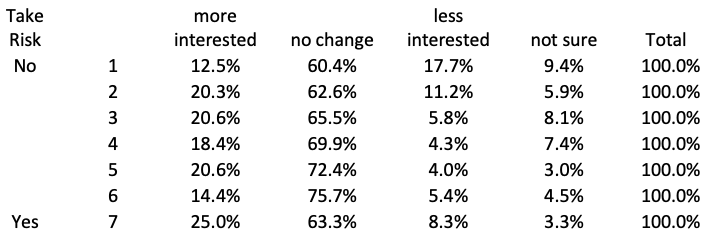

The survey asked, “How much investment risk are you willing to take?” with responses ranging from 1 (“Not willing to take any investment risk, even if it means getting almost no return on your money”) to 7 (“Willing to take a substantial amount of investment risk in order to have a chance for very high returns”). The most common response was the middle value, which was 4 (32.7% of respondents), and the remaining values were pretty consistent as you move away from that value (i.e., approximately the same number of respondents selected 3 and 5).

The table below groups respondents into their risk tolerance score (1 to 7) and notes for each level how the interest in guaranteed income changed.

There is a clear difference in responses across risk tolerance levels. Respondents who described themselves as risk averse (i.e., a score of 1) were less interested in more guaranteed income, while respondents who described themselves as risk tolerant (i.e., a score of 7) were more interested in guaranteed income.

Annuities are in theory more attractive to investors with higher levels of risk aversion (i.e., replacing the bond component of a portfolio). We saw the exact opposite. Respondents who were less risk averse were more interested in annuities given the recent market volatility compared to those who were more risk averse. This effect is hard to explain if consumers truly understood the purpose of income annuities.

A series of regressions shows that those using a financial advisor were more likely to be interested in guaranteed income. This correlation suggests that those respondents with financial advisors might be more aware of the benefits of guaranteed income. Advisors can make up for the lack of product knowledge among older investors – particularly Baby Boomers, women, and mass-affluent near-retirees who are likely to value lifetime income the greatest. Those investors are attracted to the idea of guaranteed income following market turbulence, but may not understand the role of annuities in reducing risk. And the most attractive ways to do this are through delayed claiming of Social Security retirement benefits or by purchasing an income annuity.

Conclusions

Although the market for income annuities is small enough to be considered a “puzzle” by most economists, it’s clear that demand for guaranteed income is high particularly among mass affluent consumers. But people won’t buy a product they don’t understand, and annuity knowledge is clearly limited. The wealthy, financially sophisticated consumers who understand annuities are least likely to value them (although the recent financial crisis has increased their interest). Respondents who most wanted to avoid risk didn’t understand how annuities enhance retirement security by providing lifetime income.

Advisors must play a crucial role in helping consumers understand how annuities provide value in meeting demand for income security among a growing population of Baby Boomers who do not have an employer pension.

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar's Investment Management group.

Michael Finke, PhD, is a professor of wealth management and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

Timi Joy Jorgensen, PhD, is an assistant professor and director of financial literacy at The American College of Financial Services.

Read more articles by David Blanchett, Michael Finke and Timi Jorgensen

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.