Guaranteed Returns in a Low-Yield Environment

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

These are trying times for investors who want safe assets. Vanguard had to temporarily close its Treasury money market fund as a result of record inflows. With Treasury Bills yielding about 10 basis points and CDs not yielding that much more, investors seeking yield and low risk are effectively stuck.

These are trying times for investors who want safe assets. Vanguard had to temporarily close its Treasury money market fund as a result of record inflows. With Treasury Bills yielding about 10 basis points and CDs not yielding that much more, investors seeking yield and low risk are effectively stuck.

One product worth considering is fixed annuities, which are also referred to as multi-year guaranteed annuities (MYGAs). MYGAs provide a straightforward, predetermined guaranteed rate of return over a term. In contrast, the return in a fixed-indexed annuity (FIA) or equity-indexed annuity (EIA) typically depends on the performance of some underlying index or portfolio (and is not known with certainty in advance).

The significant spreads between MYGAs and Treasury securities, which are as much as approximately 300 basis points, coupled with the guarantee, may raise some questions about the nature of the guarantee. Like other annuities, MYGAs are backed by insurance companies whose general accounts are regulated and there is the additional backstop in the form of state guaranty associations.

In this piece, we compare MYGAs to other safe investments, such as CDs and Treasury securities. We hope to better understand whether guaranteed MYGAs can provide attractive risk-adjusted performance, and whether they’re a reasonable alternative for risk-averse investors. This is a topic we plan to explore more in the future.

Overview

U.S. Treasury securities are commonly assumed to be the “risk-free” asset in investment research. While default risk hasn’t been an issue with U.S. government-issued debt (it has been for other countries), there is still interest-rate risk if the bonds are sold before they mature or are held in some type of pooled investment (like a mutual fund). There is also reinvestment risk, since changes in future interest rates can impact the true end-of-period rate of return.

CDs are well-known products offered by banks and credit unions and provide a fixed rate of return for a specific period, with terms up to five years. Bank-issued CDs are insured by the FDIC and CDs issued by credit unions are insured by the NCUA. Both provide protection up to $250,000 based on the total funds on deposit at an institution. Withdrawal penalties may apply if the funds are accessed before the term, but are currently low because they are levied as a forfeiture of interest for a period of time.

Fixed annuities, or MYGAs, have been around for decades but have increased in popularity because of ultra-low interest rates. They are issued by insurance companies with terms typically ranging from three years to 10 years and are similar to CDs in that they provide a fixed guaranteed return over the term. Surrender charges typically decline over time and are often higher than withdrawal penalties on CDs. For example, a high-yield MYGA may charge 9% if liquidated in the first year falling to 5% on a five-year contract. They are typically purchased for accumulation purposes, although they can be converted (annuitized) to guaranteed lifetime income at the end of the term. MYGAS are backed by the issuing insurance company, as well as the respective state guaranty fund, in the event the insurance company defaults.

Unlike CDs, where taxes must be paid annually on interest, gains in a MYGA are not taxed until distributions are taken. This could make MYGAs more attractive for investors holding them in taxable accounts, depending on the investor’s tax situation.

Current yields

The table below summarizes yields for intermediate and long-term Bloomberg Barclays indexes as of 10/09/20. With respect to the ratings for the individual securities in the Bloomberg Barclays indexes, they are based on the middle rating of Moody’s, S&P and Fitch. Maturities for intermediate bond indexes must be between one and 10 years and long-term indexes have maturities of 10 years or greater.

Yields increase for bonds with lower credit quality and longer durations.

Yields are unlikely to reflect the actual realized rate of return over the respective period, especially for lower quality bonds, given the impact of defaults (even ignoring future interest rate changes).

The probability of impairment, or default, increases significantly as credit quality weakens and time horizons lengthen. With respect to corporate bonds, S&P expects defaults to rise from 3.5% in March 2020to 12.5% by March 2021.

Just because a company defaults on a liability does not mean that bond holders lose all their money. For example, research by Moody’s notes that corporate “family” recovery rates, which measure the enterprise value of the corporate entity relative to its total liabilities at default resolution, are widely dispersed with a mean recovery rate of 52% and a standard deviation of 26%.

With respect to MYGAs, in the event of default, in addition to the company’s assets, policyholders also have the benefit of state guaranty associations, where insurers can access a share of the amount required to meet the portion of the guaranty association’s covered claims not covered with the insurer’s assets, where the assessment is based on the amount of premiums each insurance company collects in that state.

Guaranteed income payouts

Treasury securities

The yield of the Bloomberg Barclays intermediate government index is close to the five-year U.S. Treasury yield of 0.34% as of 10/09/20. While any direct investment in Treasury securities technically are liquid1, the value of the bonds can change if they are sold before maturity (based on how interest rates evolve over the period) and coupons would be subject to reinvestment risk (assuming it’s not a zero-coupon bond). We assume someone holds the bond for the entire period (five years), given the liquidity provisions for other guaranteed investments (e.g., CDs and MYGAs), and we ignore reinvestment risk.

CDs

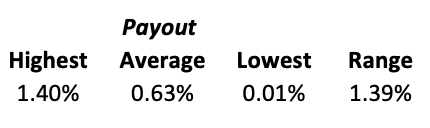

The table below summarizes the distribution of CD rates for a five-year term., based on data as of October 11, 2020, assuming a $100,000 deposit amount and a zip code of 60602 (Chicago, IL).

There is a considerable range in payouts. The average payout is only about 30 basis points above Treasury securities, although the highest available payout has a spread of 108 basis points.

The average CD rate from bankrate.com is higher than the national rate on jumbo deposits for 60-month CDs according to the FRED Economic Data website, which is 0.38%.

MYGAs

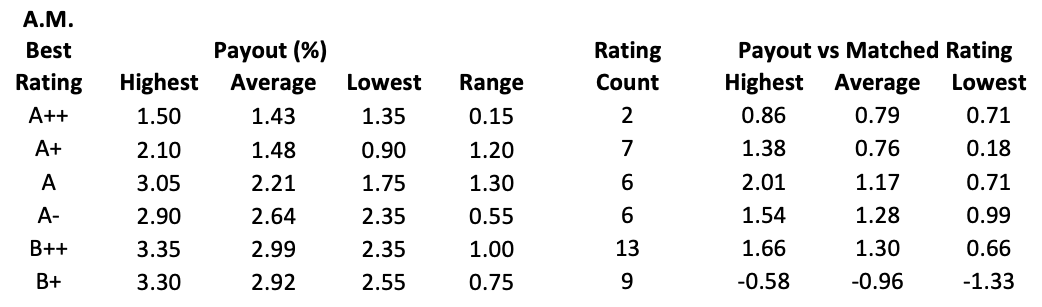

We obtained yields on MYGAs with a five-year term from Blueprint Income on October 11, 2020. The yields vary by quality, and are grouped by A.M. Best financial strength rating. The table includes information on highest, average, and lowest payout by credit rating, as well as how the yields differ from corporate bonds with the same approximate credit rating.2

There are notable variations in payouts, especially across A.M. Best financial strength ratings, where MYGA payout rates rise (significantly) as credit ratings decline. There is also a notable spread in the MYGA yields over corporate bond indexes, whether focusing on the highest, average or lowest payout among the MYGAs.

Similar to investing in corporate bonds, there is risk of default in MYGAs, which is a key reason yields increase as credit quality declines. Insurance companies issuing MYGAs have an additional backstop, state guaranty associations (as well as other insurers), that could limit losses.

MYGAs should benefit from an illiquidity premium, since the money is generally “locked up” over the investment period. However, the returns are still significantly higher than for CDs, which can have similar withdrawal restrictions.

Is it worth selecting a riskier insurer?

It depends. The average MYGA yield increases 157 basis points from the average A++ rated carrier to the average B++ rated carrier (the average B++ yield is higher than the average B+ yield). This would result in approximately 8% more wealth over the five-year term of the product. Therefore, as long as the expected loss associated with the B++ rated insurers (e.g., assuming a basket of products is used, similar to the diversification effects that investors obtain through purchasing indices) does not exceed 8%, an investor would have more wealth buying the higher yielding MYGA3.

While there is a strong relation between the MYGA rates and credit ratings (relatively monotonic), the relation between the payout rate from immediate annuities and credit ratings is significantly weaker.

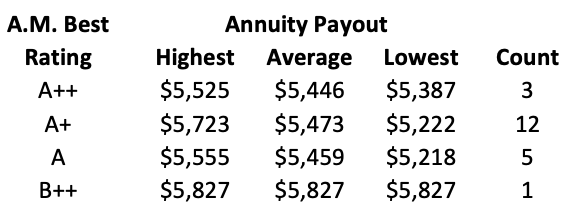

For example, below is information on annuity quotes obtained from CANNEX on October 11, 2020. The annuity is assumed to be life-only for a 65-year-old male with a $100,000 premium.

While annuity payouts increase for insurers with lower credit ratings, the relation is weaker than it is for MYGAs (fixed annuities), especially when focusing on the average payout. For example, there is virtually no difference in the average payout across A++, A+, and A rated insurers and the highest payout for an A+ rated insurer exceeds the highest payout for an A rated insurer. In contrast, there is a notable spread in the MYGA payouts for pretty much each A.M. Best rating level.

Implications

Given recent market volatility and government bond yields near 0%, many investors and financial advisors are looking for safe investments that can offer a higher “guaranteed” rate of return. MYGAs offer guarantees similar to CDs, but offer much higher returns. In fact, MYGAs yields exceed the yields from corporate bond indexes with similar credit ratings and maturity. Guaranteed returns higher than for comparable bonds is noteworthy. For example, the Bloomberg Barclays Corporate Baa intermediate-term bond index has a yield of 1.69%, which is alit more than half the 2.99% average MYGA payout for insurers with a B++ A.M. Best rating (the maximum is 3.35%).

MYGAs may be particularly attractive for clients near retirement who hold significant, nonqualified low-risk assets for the purpose of funding basic expenses after they retire. An investor in a high current tax bracket can turn $300,000 into $350,000 in five years and either cash out or use a 1035 exchange to purchase a SPIA at prevailing interest rates. Buying a MYGA smoothes their taxes over many years in retirement via the so-called exclusion ratio used to estimate the taxable portion of annuity payments. MYGAs are not suitable for clients who may be tempted to liquidate the contact prematurely.

The risk of MYGAs is harder to evaluate than the risk of corporate bonds or CDs. Historically, state guarantee funds have protected annuity owners in the event of a default. Even AIG policyholders didn’t suffer losses following its collapse during the global financial crisis. Although a mass of defaults could stretch state guaranty funds, the risk is modest given the promised high returns. The downside risk is significantly less than that of high-yield corporate bonds. This makes MYGAs worthy of consideration for clients seeking safety with a higher return.

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar’s Investment Management group and an Adjunct Professor of Wealth Management at The American College of Financial Services.

Views expressed are his own and do not necessary reflect the views of Morningstar Investment Management LLC. This blog is provided for informational purposes only and should not be construed by any person as a solicitation to effect, or attempt to effect transactions in securities or the rendering of investment advice.

Michael Finke, PhD, CFP®, is a professor of wealth management and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

1 Restrictions can apply to CDs and MYGAs and rules can vary significantly by product

2 Ratings differ from AM Best and the respective Bloomberg Barclays indices, which is why a direct comparison is not possible.

3 This is obviously a relatively simple analysis and doesn’t consider the distribution of outcomes and the utility associated with them

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All