Corporate bonds are riskier than Treasury securities. The reward for accepting this risk is larger when spreads widen, but may be less than investors expect when spreads are modest.

Corporate bonds are riskier than Treasury securities. The reward for accepting this risk is larger when spreads widen, but may be less than investors expect when spreads are modest.

Investors take corporate-bond risk when they believe the reward is big enough to justify the variability in returns. But the reward for taking this risk is inconsistent. Investors should not expect to earn the yield spread between corporates and Treasury securities, and the risk may only be worth taking when the spread is wide enough to deliver a credit premium large enough to justify the risk.

It's common to see the yield spread between corporate bonds and Treasury bonds of a similar duration as an indication of the expected bonus an investor will receive. In fact, it is common in the financial press to use the term corporate bond returns when actually referring to their yields.

On October 7, 10-year Treasury securities yielded 0.81% and AAA corporate bond yield spread on 10-year constant maturity bonds was 1.61% according to the Federal Reserve Bank of St. Louis (FRED).

Does this mean that corporate bond returns will be 1.6% higher?

No. As we will see from the historical data, this is an important mistake that results in disappointment for investors whose future goals are tied to these performance expectations.

Why are yields on corporate bonds higher than on Treasury securities? A simple explanation is that corporate bond returns are riskier and investors need to be compensated for accepting risk (the credit risk premium) and the market expects some firms to go bankrupt or otherwise fail to make future bond payments (for example the embedded option to call bonds). Other explanations include exemption from state income taxes, credit downgrades, or differences in liquidity.

Historically, corporate bonds have outperformed Treasury securities so consistently that the excess returns were referred to as a credit-risk puzzle. Like the equity-premium puzzle, the United States markets have rewarded investors who were willing to accept greater risk in the 20th century.

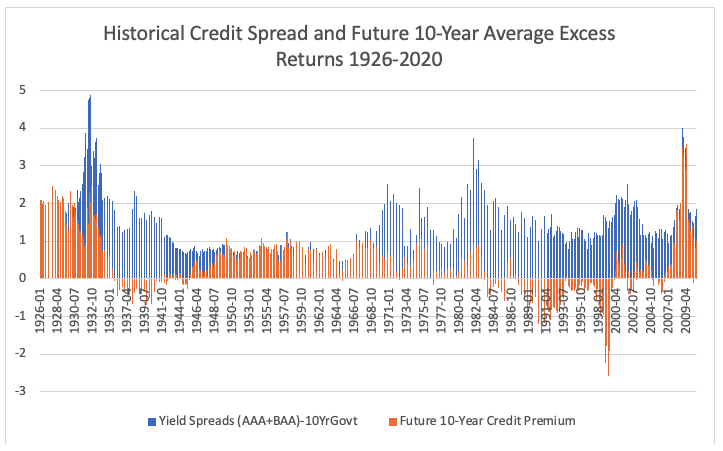

This figure shows (in blue) the current month’s credit spread measured as the difference between yields on long-term Treasury securities and the average of AAA and BBB-rated long-term corporate bonds between January 1926 and August 2020 using yield data from FRED and return data from Ibbotson SBBI indexes. The orange lines show the subsequent 10-year geometric return difference between corporate and Treasury securities. In other words, this graph shows the initial yield advantage for corporates over Treasury securities versus what actually happened.

There are 1,034 individual monthly starting dates and the final month is September 2010 to capture subsequent 10-year returns to August 2020.

When the orange line is positive, long term investors were rewarded for buying corporate bonds instead of Treasury securities. The difference between the blue and the orange line is the difference between the yields at the beginning of the period and subsequent 10-year excess annual returns. In other words, if corporate bonds yields were 1.5% higher than Treasury yields (blue line) how much extra return can investors expect over the next 10 years (orange line)? Since 1970, the yield spread has usually been far higher than the realized 10-year return difference in actual returns.

The chart shows a consistent, positive 10-year credit-risk premium for investors through most of the last 100 years. These positive excess returns for taking credit risk were, however, far more modest than the contemporaneous credit yield spread. AQR Principal Antti Ilmanen estimated that the actual credit premium after-the-fact was about one quarter of the yield spread between 1973 and 2009. After the 1980s, there were many periods where Treasury securities outperformed corporate bonds. In fact, other than those fortunate investors who bought bonds at the tail end of the global financial crisis, investors have seen very little evidence of a credit-risk premium.

Is the credit-risk premium predictable?

In a recent article, I provided evidence that 10-year stock returns have been surprisingly predictable using current valuations. Are corporate bond credit spreads equally as predictive of excess future returns? Can an advisor recommend a larger allocation to corporate bonds when spreads indicate a greater expected return from accepting this risk?

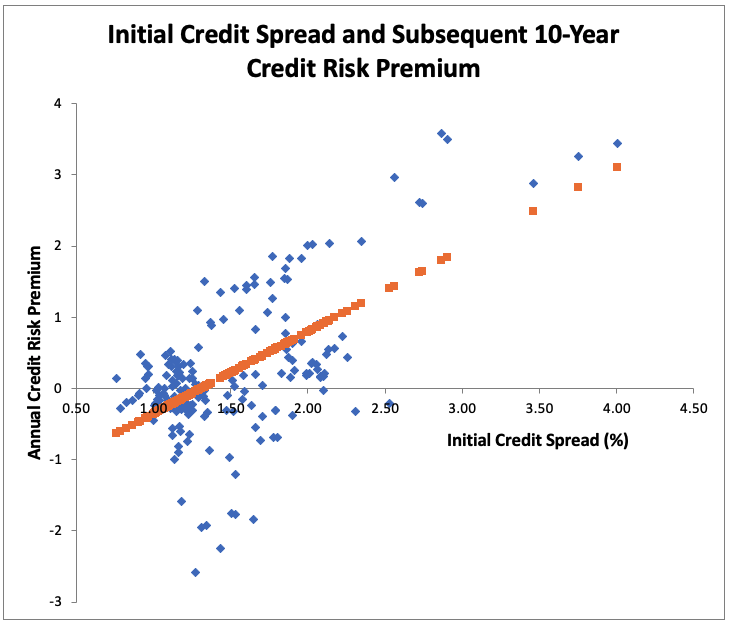

The above relationship between current spread in blue and subsequent credit-risk premium in orange shows that future returns are generally higher when spreads are greater and returns are lower when spreads are smaller. But this relationship is not consistent. However, there is a significant relationship between spreads and subsequent returns and this relationship has strengthened in recent decades.

The next figure shows the results from a regression model that predicts future 10-year credit risk premium from today's credit spread from 1995 and 2020, a total of 187 monthly periods. Those credit spreads predicted 37% of variation in the future 10-year credit risk premium. Although the regression model doesn't do a perfect job of predicting the impact of spreads on the credit-risk premium, it does show a clear and linear positive relationship between the two.

If the initial spread was greater than 1.5%, then an investor was far more likely to experience a premium for accepting credit risk by investing in corporate bonds. When spreads fall below 1.5%, the investment in corporate bonds was not as likely to have been worth the risk.

Let’s go a little further back and use a 1.75% credit-spread screening mechanism, which is roughly the median of the 487 10-year periods between 1970 and 2020, to illustrate how the bet investors make when they invest in corporate bonds changes when spreads are either wide or narrow. These are the historical risk premia for investors in wide and narrow spread environments:

Imagine choosing a fixed income allocation in an investment portfolio to fund a child's college education in 10 years. The investor can either choose Treasury securities or in a mix of corporate bonds. Should an advisor consider today's credit risk spread when deciding which type of bonds to choose?

The statistical comparison of outcomes above says that the decision to choose corporates when spreads are narrow is a risky bet with a small expected payout and high volatility. In other words, more than half the time you will have less money in the college savings account if you invest in corporate bonds than if you invest in Treasury securities when spreads are narrow. Conversely, in a wider spread environment the investor may decide to take the risk and allocate their fixed income to corporate bonds. Even at the 20th percentile, she'll still have more money to pay for the college savings goal.

The decision to invest in corporate bonds is not often portrayed as a choice in which the investor trades off an expected premium and an expected amount of risk. The above analysis shows that there is more to the credit spread than a rationally priced compensation for increased future default risk. The risk premium is time varying. And if the risk premium is higher sometimes, investors should consider whether the risk is too high for the expected reward when investing in corporate bonds.

The notion that the market rewards investors who are willing to accept risk in corporate bonds when markets are in turmoil is borne out by a sharp correlation between stock volatility and credit spreads. When negative sentiment spikes in financial markets, investors need a greater reward for accepting risk on corporate bonds. Advisors can overweight corporate bonds within a fixed-income portfolio when spreads widen.

But be warned, AQR’s Ilmanen finds that the highest-yield, lowest-credit quality bond categories underperform over time. High credit spreads on quality bonds are an opportunity, but don’t be seduced by bonds that promise gaudy yields that won’t translate into higher returns.

Implications

Don’t assume that today’s corporate yields will result in higher returns on a bond portfolio. Likewise, don’t use a corporate bond yield curve to discount future cash flows, for example from a pension or an annuity. If a fully-funded pension offers a client a cash payout with an internal rate-of-return to expected lifespan at 3% when Treasury yields are 2% and corporate yields are 3.5%, do not recommend the payout option if the assets would be invested in bonds. The expected credit-risk premium since 1970 is only about 11 basis points above Treasury securities when credit spreads are less than 175 basis points.

When estimating returns on a fixed-income portfolio in a Monte Carlo analysis, it is also not appropriate to use today’s corporate yields. Even though yields on corporate bonds are close to 2.5%, a more realistic estimate of return from fixed-income portfolio returns is closer to 1%. Of course, that doesn’t include asset-management fees.

Corporate bonds may be dominated by Treasury securities in taxable accounts for clients who live in states with a high income tax. Compare, for example, a $10,000 investment in Vanguard’s long-term Treasury ETF (VGLT) in September 2010 to the 10-year return on Vanguard’s long-term corporate ETF (VCLT). On September 30, 2020 the Treasury ETF would be worth $19,850. The long-term corporate ETF rose to $20,467. The 30 basis point difference in annual 10-year return would easily be eaten up by any modest state income tax. And the 10-year corporate ETF return dipped below the Treasury ETF during the March market crash. This highlights the other shortcoming of corporate bonds – their correlations with equities rise when the stock market falls.

Being realistic about realized credit spreads also favors financial products that promise returns above Treasury rates with little volatility. For example, the guaranteed returns on life insurance and annuities are significantly higher than on Treasury securities and, in some cases, comparable to yields on high-quality corporate bonds. This is likely the result of the insurance companies’ desire to artificially smooth their prices in a declining interest-rate environment. These return guarantees are far more valuable than yields on a corporate bond whose subsequent returns that have historically given investors about 25% of the current spread.

I would like to thank David Blanchett for his comments and assistance with data and Larry Swedroe for additional comments.

Michael Finke, PhD, CFP®, is a professor of wealth management and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

More Global Markets Topics >

Corporate bonds are riskier than Treasury securities. The reward for accepting this risk is larger when spreads widen, but may be less than investors expect when spreads are modest.

Corporate bonds are riskier than Treasury securities. The reward for accepting this risk is larger when spreads widen, but may be less than investors expect when spreads are modest.