Given that we have entered a recession, should investors cut their equity allocation? Or move to larger stocks with good financial health? The answer is “no.”

Given that we have entered a recession, should investors cut their equity allocation? Or move to larger stocks with good financial health? The answer is “no.”

After falling at an annual rate of 5.0% in the first quarter of 2020, the Bureau of Economic Analysis announced that U.S. GDP fell at an annual rate of 32.9% in the second quarter. Two consecutive quarters of negative growth is how recessions are generally defined by economists. However, the official arbiter of recessions is the National Bureau of Economic Research (NBER). It was on June 8th that the NBER declared the U.S. economy was in recession. The Business Cycle Dating Committee of the NBER determined that a peak in monthly economic activity occurred in the U.S. in February 2020. The peak marks the end of the expansion that began in June 2009 and the beginning of a recession.

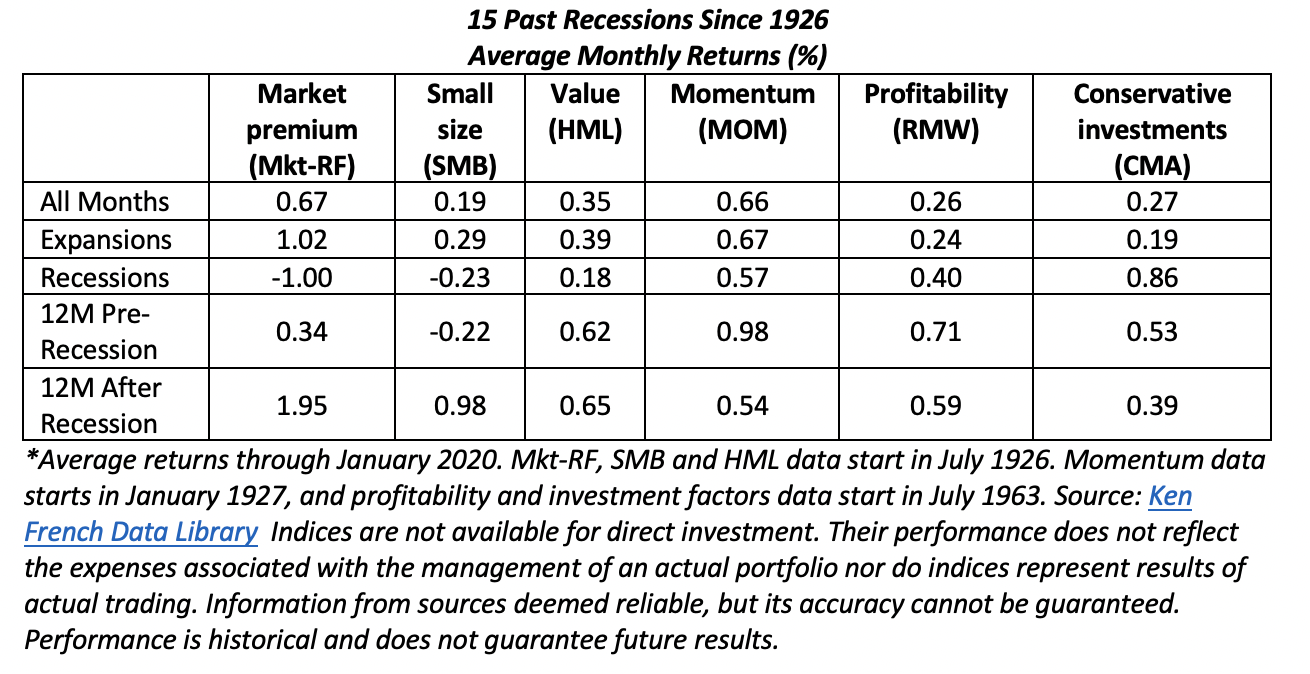

One of the more frequently asked questions I receive is how factors perform in recessions. Thanks to my friend and co-author Andrew Berkin of Bridgeway Capital Management, we have the answers. The table shows how factors perform in expansions, recessions, pre-recessions and post-recessions.

During expansions, all factors are economically significant; Berkin found them to be statistically significant. However, the story is somewhat different during recessions: Both the market’s excess return and small size returns are now negative, and value returns are notably reduced. However, the other three factors show economically significant premiums, showing the benefits of diversification across factors.

The reason to maintain your asset allocation is that timing recessions and their length is extremely difficult. For example, we often don’t learn that we are in a recession until well after it is officially declared. And we often don’t learn that a recession has ended until well after the fact.

The market is forward-looking. With that in mind, all economic forecasts are for positive growth for the remainder of this year and into next. For example, the Philadelphia Federal Reserve Survey of Professional Forecasts predicts GDP growth over the four quarters beginning with the third quarter of 2020 of 10.6%, 6.5%, 6.8% and 4.1%.

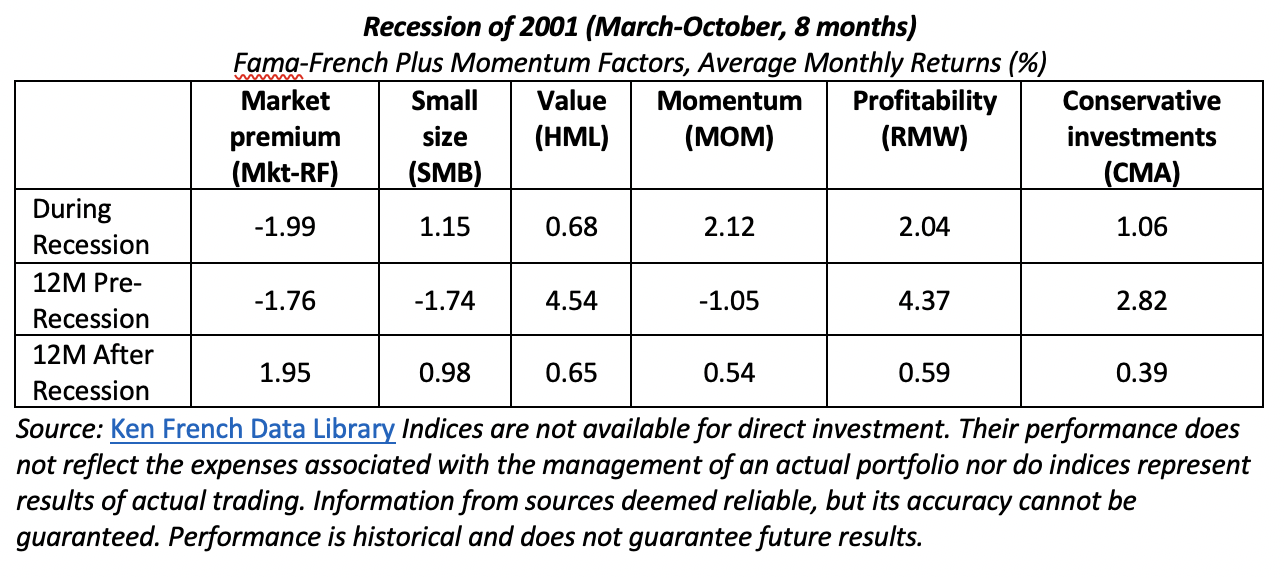

Another reason to avoid trying to time factor exposures is that each recession and subsequent expansion is different. Berkin demonstrated that by examining the period around the 2001 recession. He explained: “While small size (SMB) and value (HML) have typically been negative or weak during a recession, both factors had strong returns in the recession of 2001. Large cap and growth stocks had dominated in the tech bubble that grew during the last two years of the 1990s and the first quarter of 2000. Their collapse not only helped usher in the subsequent recession, but also set the stage for historically cheap and beaten down small and value stocks to recover strongly.”

There’s yet another reason to avoid trying to time factor exposures: Economic forecasting is extremely difficult. If you doubt that, consider the following evidence.

In his wonderful book “The Fortune Sellers,” William Sherden, an economist himself, reviewed economic forecasts. He found that economic forecasts are basically the equivalent of monkeys throwing darts. He even found that economists who directly or indirectly can influence the economy – the Federal Reserve, the Council of Economic Advisors and the Congressional Budget Office – had forecasting records that were worse than pure chance. He concluded that there are no economic forecasters who consistently lead the pack in forecasting accuracy. And consensus forecasts did not improve accuracy. Perhaps the most damaging of his findings was that just when the accuracy of a forecast is most important, at the turning points (when the economy shifts from being in a recession to not being in a recession – and vice versa), economic forecasts showed the least accuracy – of 48 predictions, 46 missed the turning points in the economy.

Further evidence is from the study, “How Accurate Are Forecasts in a Recession,” by Federal Reserve Bank of St. Louis economist Michael McCracken. He came to a similar conclusion. McCracken reviewed 26 years of quarterly, one-year-ahead mean Survey of Professional Forecasters forecasts and found that the forecasters’ errors were four times larger when the economy was in recession than when it was not. In other words, just when you would like to know when it is safe to buy stocks again, forecasting skill (which is not good to begin with) deteriorates significantly.

If that hasn’t convinced you, perhaps these words of wisdom from Warren Buffett might: “I don’t pay any attention to what economists say. If you look at the whole history of [economists], they don’t make a lot of money buying and selling stocks, but people who buy and sell stocks listen to them. I have a little trouble with that.” He also stated: “We have long felt that the only value of stock forecasters is to make fortune-tellers look good. Even now, Charlie (Munger) and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children.”

The evidence shows that active managers have an extremely difficult time exploiting a bear market. For example, Vanguard’s research team published a study on the performance of active managers in bear markets in the spring/summer 2009 issue of Vanguard Investment Perspectives. Defining a bear market as a loss of at least 10%, the study covered the period 1970-2008. The period included seven bear markets in the U.S. and six in Europe. Once adjusting for risk (exposure to different asset classes), Vanguard reached the conclusion that “whether an active manager is operating in a bear market, a bull market that precedes or follows it, or across longer-term market cycles, the combination of cost, security selection, and market-timing proves a difficult hurdle to overcome.” It also confirmed that “past success in overcoming this hurdle does not ensure future success.” Vanguard was able to reach this conclusion even though the data was biased in favor of active managers because it contained survivorship bias.

As further evidence, Lubos Pastor and Blair Vorsatz, authors of the July 2020 study, “Mutual Fund Performance and Flows During the COVID-19 Crisis,” found that active funds underperformed once again during the crisis.

Conclusion

If timing recessions is hard and picking which factors will do well even harder, what should you do? The answer is simple: Adhere to your well-thought-out plan and ignore the noise of the market and the butterflies in your stomach. To quote Warren Buffett one more time, in his 2004 Annual Letter to Berkshire Shareholders, he advised investors that they should never try to time the market, but, “if they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy only when others are fearful.”

Larry Swedroe is the chief research officer for Buckingham Wealth Partners.

The information in this article is for educational purposes only and should not be construed as specific investing, accounting, tax, and legal advice. Indices are not available for direct investment. Their performance does not reflect the expenses associated with an actual portfolio nor do indices represent results of actual trading. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. R-20-1269

Read more articles by Larry Swedroe

Given that we have entered a recession, should investors cut their equity allocation? Or move to larger stocks with good financial health? The answer is “no.”

Given that we have entered a recession, should investors cut their equity allocation? Or move to larger stocks with good financial health? The answer is “no.”