How SPACs Destroy Investor Wealth

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Special-purpose acquisition companies (SPACs) should be illegal, according to Jeremy Grantham. Moreover, he says those structures are so speculative that investor enthusiasm for them is symptomatic of a pending collapse in equity prices.

Special-purpose acquisition companies (SPACs) should be illegal, according to Jeremy Grantham. Moreover, he says those structures are so speculative that investor enthusiasm for them is symptomatic of a pending collapse in equity prices.

Aside from Grantham, few observers have questioned the economic viability of SPACs, which have accounted for approximately half of the IPO volume in 2020.

That is why I was impressed when I read a recent study, A Sober Look at SPACs, by Michael Klausner of Stanford Law School and Michael Ohlrogge of the New York University School of Law. I also spoke with Ohlrogge last week to prepare this article.

Klausner and Ohlrogge exposed the central flaw in the SPAC structure. They also demonstrated that the performance of SPACs in the public markets has been unimpressive and that their purported benefits have been overstated or are nonexistent.

I will review their research. Because of the complexity of the SPAC structure, I will use an analogy to illustrate the destructive power they inflict on investors’ wealth.

I will conclude with an example of a properly structured SPAC that resolves the problems in the typical structure.

I will reference a recent SPAC whose target investments intersect with the financial planning profession (Lefteris, which targets “fin tech” investments) and those SPACs that target the acquisition of advisory practices.

What is a SPAC?

A SPAC is a corporation that raises money through a public offering to pursue a future acquisition. They are also known as “blank-check” companies because they raise funds before they identify the company they intend to acquire. A SPAC is led by a sponsor, and it has a board of directors and a management structure. Typically, the sponsor, board and management have worked together before in the industry they intend to target for an acquisition.

The IPO investors purchase shares at a standard price of $10, which also gives them rights and/or warrants that are usually exercisable at $11.50 per share. The sponsor receives 20% the post-IPO equity at essentially no cost. This is known as the “promote.” The sponsor typically also provides funding to the entity through the purchase of warrants exercisable at $11.50/share, often at a price of $1.00 to $1.50/share, which may approximate their fair market value.

The funds raised through the SPAC’s IPO are held in a trust that invests in short-term Treasury securities. The SPAC must execute a transaction within two years; if not, the trust is liquidated, and the funds are returned to the investors.

Once a transaction is announced, the investors have the option to redeem their shares for their $10 purchase price plus interest earned by the trust. If they do, they get to keep their rights and warrants. The actual transaction is a merger between the SPAC and a private company that retains the public company identity of the SPAC. Typically, the SPAC must raise additional funds through “PIPEs” (private placements) to adequately fund the purchase of the private company.

How SPACs destroy wealth

A SPAC is a get-rich-quick scheme that benefits the sponsor, and that comes at the expense of the non-redeeming shareholders.

To understand why this is the case, I will use an analogy.

Let’s assume we have three individuals – Moe, Larry and Curly. Moe is the sponsor, and he approaches Larry and Curly to invest sizeable sums in his SPAC. Moe explains that he will retain 20% ownership of the entity without contributing his own money. Larry and Curly make their investments at $10/share and receive their stock and rights and warrants.

Moe subsequently identifies a target company to acquire and presents the transaction to Larry and Curly.

Larry redeems his shares, but Curly does not.

The transaction proceeds, although Moe now has less capital to make the acquisition because of Larry’s redemption. The merger is completed, and the new entity begins life as a public company.

Moe is ecstatic with his newly acquired wealth as a share of the public company, for which he contributed no capital.

Larry is happy too. He earned a risk-free return on his $10 investment and retained the rights and warrants, which have value that will increase if the public entity thrives.

Curly is despondent. He discovers that his $10 investment is now worth only two-thirds of the price he paid for it. He was the victim of the dilution that came from the sponsor’s shares and the underwriting fees and other expenses incurred by the SPAC. A third of his wealth was destroyed.

This highly simplified analogy reflects exactly what Klausner and Ohlrogge found in their research.

They studied all 47 SPACs that merged between January 2019 and June 2020. They found that the mean SPAC, at the time it merges with its target, has only $6.67 in cash.

My analogy omits key elements in the life of a SPAC, such as the need for more than three quarters of them to raise additional funds through private placements. But, except for the non-redeeming shareholders1, no other entity in a SPAC transaction is exposed to the risk of dilution. The sponsor, redeeming shareholders, underwriters and legal counsel, private placement investors and shareholders in the target company will not suffer a certain loss through dilution.

Klausner and Ohlrogge found that the post-merger share prices dropped for a large majority of SPACs. Those price drops were highly correlated with the extent of dilution, or cash shortfall, in a SPAC.

“This implies that SPAC investors are bearing the cost of the dilution built into the SPAC structure, and, in effect, subsidizing the companies they bring public,” they wrote. “We question whether this is a sustainable situation.”

The complexity of the SPAC structure obscures the corrosive effect of the dilution. The Lefteris prospectus, for example, has approximately 160 pages, half of which are devoted to explaining the risks to investors. It requires a careful analysis to distill its economic structure and the effect on investors.

Indeed, Klausner and Ohlrogge spent three years researching this subject before publishing their paper.

The false promises of SPACs

Several arguments have been advanced to justify the value that SPACs can provide. Klausner and Ohlrogge show that those claims are unfounded.

SPACs do not perform well post-merger as a public entity

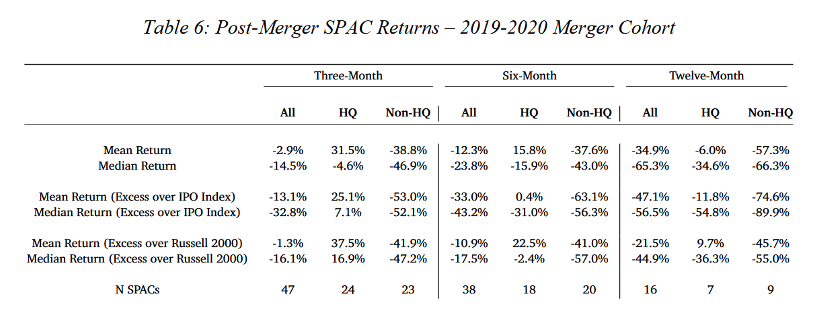

Let’s begin with the hype about post-merger performance. The table below is taken from their paper:

Across their sample, SPACs were losing propositions over three-, six- and 12-month timeframes, whether you look at the mean or median returns, and whether you compare those returns to the average of IPOs or to the Russell 2000.

They went further to investigate claims that certain SPAC sponsors deliver better performance. They divided their sample into high-quality (HQ) ones that were run by a Fortune 500 CEO or by a fund with more than $1 billion in assets. The HQ SPACs did slightly better than the non-HQ ones but were losing propositions over the full 12-month horizon. The only caveat is that the mean HQ SPAC had a positive return relative to the Russell 2000 over the 12-month horizon. But the median return was negative, implying that the mean return benefited from a small number of strong outperformers.

A study by McKinsey also documented better performance by operator-run SPACs. But that study had a smaller sample size and used less rigorous methodology than Klausner and Ohlrogge. One must also consider that there is a conflict of interest because of the consulting services McKinsey offers to the SPAC industry.

SPACs do not have a lower regulatory burden than IPOs

Some claim that SPACs enjoy an advantage, relative to an IPO, in that they face a lower regulatory burden, thereby making it easier for companies to go public.

Klausner and Ohlrogge explain why that is not true. They state, for example, “SPACs have slight disadvantages regarding Sarbanes Oxley compliance compared to firms going public via traditional IPOs, though the differences are not large.”

Companies that go public through a SPAC do need to register with the SEC. They also typically need to perform the “dog and pony” ritual of presenting to prospective investors. This is because SPACs almost always need to raise capital through private placements to replace the capital lost by redeeming shareholders.

SPACs have some regulatory advantages. An IPO prospectus does not contain forward-looking projections because, if it did, the company would face legal vulnerability if those projections were wrong. But SPACs can and do provide projections because they have a “safe harbor” protection that IPO prospectuses do not. This may benefit SPACs that have businesses that are hard to understand or evaluate.

SPACs also have an advantage with respect to section 11 liability. Under that section of the 1933 securities act, a company undergoing an IPO can face lawsuits with respect to its misstatements or omissions in its disclosure statements. This has resulted in many lawsuits for IPOs. SPACs are insulated from section 11 and have faced very few legal challenges. But, as Klausner and Ohlrogge point out, this may be to the detriment of investors, because it could lead to “less due diligence and sloppier disclosure. The insulation of the underwriter in particular could reduce the discipline on the SPAC and its target to take care in its disclosures related to their merger.”

SPACs do not have greater price certainty when they go public than an IPO

The price of an IPO is set the day before the offering. Some claim that SPACs have an advantage because their price is set earlier, well before the merger.

But Klausner and Ohlrogge explain that is often not so. SPACs face uncertainty in the number of shares that will be redeemed, which affects the amount of cash the private company will receive. SPACs often must negotiate with private placement investors right up until weeks before the merger closes to ensure there is adequate capital to fund the deal.

“Overall, therefore, SPAC mergers do not inherently provide much price certainty, deal certainty, or certainty regarding how much total cash the target will receive,” the authors wrote. They also found that it is unlikely that a company can go public through a SPAC faster than through an IPO.

Another claim is that SPACs enjoy an advantage because they can raise funds through private placements, and those investors have greater access to information about the target company (in Wall Street parlance, they can go “over the wall.”) But Klausner and Ohlrogge explain that nothing prevents a company undergoing an IPO to also use private placements.

The issue of price certainty should be a major concern for the target companies a SPAC seeks to acquire, such as advisory practices. Given the incentive for IPO shareholders to redeem their shares, target companies cannot predict how much cash will be available in the SPAC to complete the acquisition. Redemptions are not known until the merger closes. Ohlrogge told me it is moderately common for the SPAC to have 100% redemptions. The target company must rely on the sponsor to provide funding through private placements.

Indeed, sometimes the sponsor negotiates a private placement, where the new investors buy in at a low price, say $8.00 per share or sometimes even less, according to Ohlrogge. In one case, private placement investors bought convertible notes. If you priced it all out, according to Ohlrogge, they bought in at effectively about $3.00 per share.

When there are very high redemptions, there will be a private placement that brings in new cash – but not always, according to Ohlrogge. In eight of the 47 SPACs in his sample, the SPAC had $10 million in cash or less by the time of the merger. A target is taking a big gamble by merging with a SPAC, hoping for low redemptions, but knowing if they get too high, it could be left with a bad deal.

An investor needs to ask itself, “How good must the deal look to the target, in order for it to be willing to take such a big risk?” According to Ohlrogge, it likely means that if redemptions are only 50% to 75%, the target is getting a great deal, and it's coming at the expense of SPAC investors.

It is more costly for a SPAC to go public than for an IPO

The underwriting fee for an IPO is typically 5% to 7%, versus 5.5% for a SPAC. But that is not the full story. The underwriters of an IPO routinely underprice the offering to ensure that it is fully subscribed. This leads to a “pop” on the first day of trading – roughly 20%, according to Klausner and Ohlrogge. Some observers may disagree, but that 20% is a cost to the company. Thus, the total cost of an IPO is 25% to 27%.

But what about a SPAC? Because approximately 73% of the shares in a SPAC are redeemed, its 5.5% underwriting fee should be applied to the remaining 27% of the IPO proceeds, not to the full amount. One must also consider the dilution imposed by the sponsor’s promote and the rights and warrants issued to redeeming and non-redeeming shareholders. Once those are considered, Klausner and Ohlrogge estimate the true cost of underwriting a SPAC is 50.4%

There is one notable feature of the Lefteris offering. Its prospectus states: “Unlike many other similarly structured blank check companies, our initial stockholders will receive additional shares of Class A common stock if we issue shares to consummate an initial business combination.” This clause imposes dilution on the non-redeeming shareholders beyond what Klausner and Ohlrogge analyzed in their study. This means that the sponsor will not face any dilution as a result of private placement funding. Among other things, this means that the non-redeeming shareholders and private placement lenders will absorb all the underwriting costs.

SPACs are not a “poor man’s private equity”

Some contend that SPACs are a way for retail investors to make private-equity-like investments without having to pay the fees associated with private equity funds.

But approximately 85% of SPAC investors are institutions, typically hedge funds. Even among the 15% of holders that are not institutions, it is likely that many of them are wealthy individuals who do not need to disclose holdings through a 13F filing.

A group of those funds have become known as the “SPAC Mafia,” in that they routinely invest in SPACs and redeem their shares (retaining the rights and warrants they were issued). Klausner and Ohlrogge estimate the SPAC Mafia controls 70% of post-IPO capital. The median SPAC Mafia investor divests 97% of its shares once the merger is completed.

Through 13F disclosures, we know that two of Lefteris’ investors are hedge funds that fit the description of the SPAC Mafia (although that distinction is not a formal one). According to Ohlrogge, Weiss is quite large. From 2010 to 2019, it had at least 100,000 shares in 65 different SPACs and a "divestment rate" greater than 95%. Linden had 21 SPACs with at least 100,000 shares, and it retained about 35% of its IPO-stage holdings, which is uncommonly high.

Since Weiss and Linden control about two-thirds of Lefteris’ IPO shares, investors should expect substantial redemptions at the time a merger is announced.

Final thoughts

Ohlrogge told me that he did not receive any pushback on their paper. He has spoken with many people in the SPAC industry. Their response is often to acknowledge the problems he and Klausner identified, but to then claim that their SPAC will be “different.”

I showed a preliminary draft of this article to two SPAC sponsors. Neither identified any factual errors.

SPACs are a financial structure designed to bring a company public. That company will eventually merge with a private company to create a publicly held operating company. But by the time that merger has completed, most of the SPAC investors will be gone, either having redeemed their shares or sold them on the open market.

That post-merger company will be led by the SPAC sponsor, who will acquire substantial wealth through the “promote” – essentially free shares granted at the time of the SPAC’s IPO. The cost of that promote, and that of the warrants and rights still held by redeeming shareholders, and of the underwriting and other fees incurred by the SPAC will be paid disproportionately by the non-redeeming shareholders. Their wealth will be destroyed.

The SPAC sponsor may do a lot of work to consummate the merger. But a SPAC is still a get-rich-quick scheme when compared to traditional IPOs.

The problem with SPACs is a gross misalignment of incentives between the sponsor and the non-redeeming investors. This is built into the traditional SPAC structure.

But it does not have to be that way.

In July 2020, Pershing Square, a hedge fund run by Bill Ackman, launched a SPAC without any promote. It was the largest SPAC to date, and as part of the deal Pershing purchased warrants that were 20% out of the money and do not vest until three years after the merger. Pershing also committed to invest $1 billion at the time of the merger and another $2 billion later in exchange for further warrants.

Pershing’s SPAC also has unique redemption features. It issued warrants for only one-ninth of a share, far less than other SPACs. It also rewards non-redeeming shareholders with additional warrants. It has a “tontine” feature that allocates warrants from redeeming to non-redeeming shareholders. Those features are designed to eliminate the incentive to redeem shares.

The net effect of the Pershing SPAC structure is to align incentives between the sponsor and all its shareholders. A validation of the improvement in Pershing’s structure is that Seth Klarman’s Baupost Holdings purchased 17.5 million shares in its IPO.

Until regulatory reforms are imposed on the SPAC structure or more issuers adopt the Pershing template, investors in deals such as Lefteris should redeem their shares. Target companies should be extremely cautious about merging with a SPAC.

1 Public shareholders who bought stock on the open market pre-merger will also be victims of dilution. This could happen if, for example, the market price of the SPAC rises above $10 and initial IPO investors sell their stock.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All