Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

With fixed income yields stubbornly low, should clients prepay their mortgage instead of investing in bonds? I argue this question is based on a false equivalence. Mortgages are not “negative bonds.” The prepayment decision goes well beyond interest savings and should consider asset allocation, risk tolerance, and liquidity.1

Prepaying a mortgage changes your asset allocation

It’s very common for clients to say prepaying a mortgage is akin to investing in bonds. This is because technically a mortgage, or indeed any borrowing, can be thought of as a short bond position. But this is myopic. A mortgage is not attached to a client’s bond portfolio any more than is a car loan or credit card balance.

There are two sensible ways of looking at a mortgage in the context of a client’s overall financial picture.

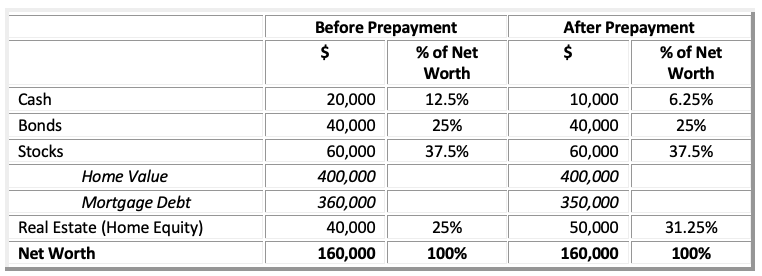

Since the mortgage is secured by a home, prepaying increases the percentage of net worth allocated to real estate. This example uses $10,000 cash to prepay some mortgage principal:

Net worth does not change because of the prepayment – we are simply reducing cash and increasing home equity by the same amount. As a percentage of net worth, home equity increases from 25% to over 31%. As an investment, therefore, a prepayment can be interpreted as reallocating a greater percentage of net worth to real estate.

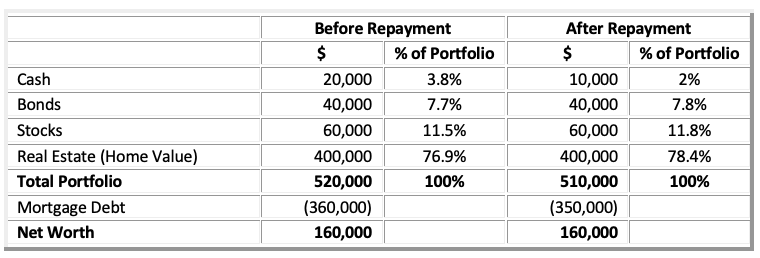

I prefer an alternative view. For practical purposes, clients are on the hook for repayment of a mortgage regardless of what happens with the value of the home.2 In other words, it is more appropriate to treat a mortgage as generic debt, not attached to a specific asset. Viewed this way, prepayment shifts the allocation from cash to the other asset classes pro rata.

From this perspective debt is an offset to the entire portfolio. Prepayment again does not change net worth, but as a percentage of the total portfolio the largest asset will increase most. For many households, the largest asset is the home.

Regardless of how you look at it, prepayment is not part of the bond allocation. We have to look at the impact on the total portfolio.

Prepayment is risk reduction

Apart from shifting asset allocation, prepaying a mortgage reduces risk. A mortgage is just borrowed money. Borrowing money to invest (in a home, stocks, or any asset) uses leverage, and leverage increases the risk of the investment. The client with a net worth of $160,000 and total assets (including the home) of $520,000 has a gross leverage ratio of 3.25:1. That’s twice as much leverage as the average hedge fund.3

Paying off any debt reduces leverage, and it generally makes sense to start with the most expensive (highest interest rate) debt. Compare rates on credit cards, student loans, auto loans, life insurance loans, or brokerage account margin loans; it may be better to pay those off first.

The financial return on prepaying a mortgage is its interest rate

This makes intuitive sense and the math bears it out, though it is sometimes overthought. To be clear: For every dollar of prepayment, over the remaining life of the loan the interest savings work out to a return equal to the interest rate. This is true even though the contractual mortgage payments remain the same. It’s just that there will be fewer of them. Moreover, for a fixed-rate mortgage the return is known. For a variable-rate mortgage, it is not.

The other side of the coin is the expected return on the money borrowed, taking into account risk. Prepaying the mortgage provides a risk-free return; if the money is instead invested, the expected return should include an appropriate risk premium. However, there is no reason to arbitrarily compare the interest rate paid on a mortgage to interest earned on bonds.

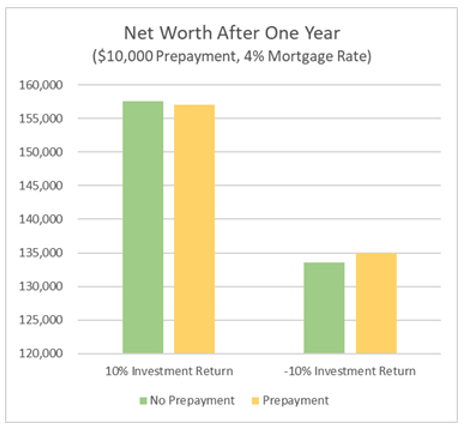

If the expected return compensates for risk, it may be a reason not to prepay. But this is effectively investing on margin, with the asymmetric payoff that comes with leverage. The choice is to borrow $10,000 from the mortgage company to invest in the hopes of earning more than the interest rate on the mortgage. If that rate is 4% and the investment return is 10%, the margin investor is ahead by 6% on the borrowed funds. If investment return is negative 10%, they are behind by 14%. By prepaying, they lock in a return of 4%.

Here is the impact on net worth after a year with all else equal (net worth declines in the example because interest costs on the total mortgage balance are more than the investment income on the portfolio).

Most people don’t take out a mortgage to invest in the stock market. They do it to afford a home. But once they accumulate enough assets to make prepayment an option, they should make sure that 1) the portfolio earns an appropriate premium over the mortgage rate, and 2) they are comfortable with the added risk of using leverage.

Prepaying reduces liquidity

Before writing a big check to the mortgage company, there is one risk that prepayment increases: liquidity risk. Liquidity risk is the risk of not being able to come up with cash when you need it. Because prepayment of a mortgage is not easily reversible, it’s important to have foreseeable (and unforeseeable) cash needs covered by other sources. The happy glow of becoming debt-free will quickly wear off for clients who prepay a mortgage only to find themselves having to carry a credit card balance or being forced to sell a highly appreciated stock six months down the road.

Peter Hofmann, CFA, is with Fieldmark Advisors, a registered investment advisor based in North Salem, N.Y.

1 There are other considerations that are not considered here, including taxes, the mortgage as an inflation hedge, and the “peace of mind” that many people report when eliminating debt.

2 It can be difficult to simply walk away from a home if the value drops below the mortgage principal and other assets are available to pay off the loan. The reasons include the impact on credit scores, legal requirements to make the lender whole, and reputational or ethical concerns.

3 A May 2017 study by the SEC found the average leverage ratio of over twelve thousand hedge funds to be 1.63x. See https://www.sec.gov/files/dera_hf-liquidity.pdf

Read more articles by Peter Hofmann