Investing based on environmental, social and governance (ESG) concerns should lead to lower returns, since the prices of those stocks will be bid up beyond their intrinsic value. But new research shows that by combining ESG- and momentum-based principles, investors can achieve higher risk-adjusted returns.

The increased popularity of ESG investing has been accompanied by heightened research into the subject. Matus Padysak contributes to the literature with his August 2020 paper, “ESG Scores and Price Momentum Are More Than Compatible.” Using optimization tools, he examined whether you could enhance the classic momentum strategy by making it more sustainable (weighting the momentum portfolio toward firms with positive momentum in their ESG scores). He also examined whether you could enhance an ESG strategy by weighting it toward stocks with positive momentum. ESG scores were from OWL Analytics. The dataset contained 691 U.S. stocks and covered the period April 2010 through October 2019. Portfolios were long only. Following is a summary of his findings:

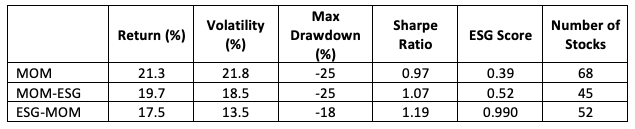

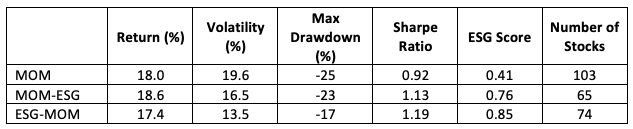

- A combined strategy that selects stocks with the highest momentum while maximizing ESG scores of the portfolios results in momentum portfolios that are significantly more responsible, with lower volatility and better risk-adjusted returns.

- A combined strategy that selects stocks with the highest ESG scores while maximizing momentum at the same time results in a more profitable ESG portfolio.

- The combined ESG-momentum strategy has the best risk-adjusted return, the lowest drawdown, the lowest volatility and the most consistent returns.

- Relative to the CAPM (market beta), the Fama and French three-factor (market beta, size and value) model, and the Fama and French five-factor (adding investment and profitability) model, the strategies have both economically and statistically significant (at the 1% confidence level) alphas – common market factors cannot explain performance.

The following table shows the results using the top 10% of stocks:

For the top 15% of stocks, the results were similar:

These findings led Padysak to conclude: “Momentum can be an ideal combination to be used with ESG scoring system.” He added: “Momentum strategies that are both popular and profitable are vulnerable to momentum crashes. ESG stocks tend to be less volatile, a characteristic that is vital in momentum portfolios.”

Padysak’s findings are consistent with those of Madelyn Antoncic, Geert Bekaert, Richard Rothenberg and Miquel Noguer, authors of the June 2020 study, “Sustainable Investment - Exploring the Linkage Between Alpha, ESG, and SDG’s.” They explored the possibility of creating an active portfolio that achieves the goals associated with ESG investing but still generates alpha. From the roughly 640 stocks in the MSCI USA Index, they created an active portfolio of about 50 stocks using the MSCI ESG ratings that showed positive “ESG momentum.” Their data sample covered the period 2013 through 2018. At the end of each year, stocks in each of 11 Global Industry Classification Standard (GICS) sectors were ranked on their absolute and relative ESG momentum, and the GICS 10% highest-ranking stocks were selected. These stocks were held for a full year, after which the portfolio was rebalanced. The stocks within each industry, and the industry portfolios themselves, were market-value weighted. They found that ESG momentum portfolios (both relative and absolute) outperformed the index. Specifically, the relative momentum portfolio generated a highly significant Fama-French three-factor (beta, size and value) alpha of 5.64% per year. Adding the two additional factors of investment and profitability did not change this conclusion.

The finding that combining momentum with ESG strategies improved performance should not be a surprise, as research, including such studies as “A Century of Evidence on Trend-Following Investing,” has found momentum to exist everywhere: in stocks, bonds, commodities and currencies as well as within and across industries. In addition, the increasing cash flows into ESG strategies have led to firms with high sustainable investing scores earning rising portfolio weights and thus momentum in their stocks.

Summary

While economic theory suggests that if a large enough proportion of investors choose to avoid the stocks of companies with low sustainability ratings, the share prices of such companies will be depressed. Thus, they would offer higher expected returns (which some investors may view as compensation for the emotional cost of exposure to what they consider offensive companies). With this knowledge, investors are positioned to pursue their financial goals in a manner that reflects their values and at the costs (in the form of lower expected returns) they are willing to bear to achieve those values.

However, the research points a way for ESG investors to “have their cake and eat it too.” By combining classic and ESG momentum, they can reduce drawdown and volatility risk while improving risk-adjusted returns. Another way to enhance returns of ESG strategies is to “tilt” portfolios to those sustainable firms with higher costs of capital.

When considering these findings, keep in mind that investor preferences (in this case for sustainable investments) lead to different short- and long-term impacts on asset prices and returns. Firms with high sustainable investing scores earn rising portfolio weights, leading to short-term capital gains for their stocks—realized returns rise temporarily. However, the long-term effect is that higher valuations reduce expected long-term returns. The result can be an increase in green-asset returns even though brown assets earn higher expected returns.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners.

Important Disclosure: The information contained in this article is for educational purposes only and should not be construed as specific investment, legal, tax, or accounting advice. Certain information contained in this article are based upon third party information and deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the third-party links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements, or representation whatsoever by us regarding third party websites. We are not responsible for the content, availability, or privacy policies, of these sites, and shall not be responsible or liable for any information, opinions, advice, products, or services available on or through them. LSR-21-54

Read more articles by Larry Swedroe