The Covid Trauma Has Changed Economics-Maybe Forever

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOnce ideas about how to manage the economy become entrenched, it can take generations to dislodge them. Something big usually has to happen to jolt policy onto a different track. Something like Covid-19.

In 2020, when the pandemic hit and economies around the world went into lockdown, policymakers effectively short-circuited the business cycle without thinking twice. In the U.S. in particular, a blitz of public spending pulled the economy out of the deepest slump on record—faster than almost anyone expected—and put it on the verge of a boom. The result could be a tectonic transformation of economic theory and practice.

The Great Recession that followed the crash of 2008 had already triggered a rethink. But the overall approach—the framework in place since President Ronald Reagan and Federal Reserve Chair Paul Volcker steered U.S. economic policy in the 1980s—emerged relatively intact. Roughly speaking, that approach placed a priority on curbing inflation and managing the pace of economic growth by adjusting the cost of private borrowing rather than by spending public money.

The pandemic cast those conventions aside around the world. In the new economics, fiscal policy took over from monetary policy. Governments channeled cash directly to households and businesses and ran up record budget deficits. Central banks played a secondary and supportive role—buying up the ballooning government debt and other assets, keeping borrowing costs low, and insisting that this was no time to worry about inflation. Policymakers also started looking beyond aggregate metrics to data that show how income and jobs are distributed and who needs the most help.

While the flight from orthodoxy was most pronounced in the world’s richest countries, versions of this shift played out in emerging markets, too. Even institutions like the International Monetary Fund, longtime enforcers of the old rules of fiscal prudence, preached the benefits of government stimulus.

In the U.S., and to a lesser extent in other developed economies, the result has been a much faster recovery than after 2008. That success is opening a new phase in the fight over policy. Lessons have been learned about how to get out of a downturn. Now it’s time to figure out how to manage the boom.

FOR CENTURIES, theorists have pondered the recurring and inevitable swings that make up the business cycle. They’ve looked for causes in mass psychology, institutional complexity, and even weather patterns. According to the traditional laws of the cycle, it should’ve taken years for households to claw their way back from 2020’s sudden collapse in economic activity.

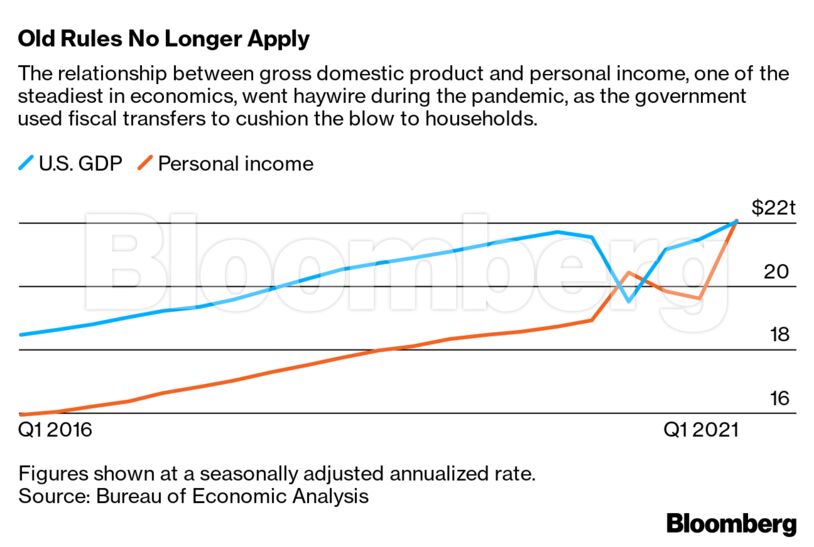

Instead, the U.S. government stepped in to insulate them from its worst effects in a way that hadn’t really been tried before: by replacing the wages that millions of newly out-of-work Americans were no longer receiving from employers. In the aggregate, benefit checks made up for all the lost paychecks and then some—even though creaky systems for delivering unemployment insurance or one-time stimulus payments meant that many people missed out.

The scale of this innovation is apparent in what Jan Hatzius, chief economist at Goldman Sachs Group Inc., has called “the most amazing statistic of this entire period.” In the second quarter of 2020, a time when economic activity—measured by the conventional gauge of gross domestic product—was shrinking at the fastest pace on record, U.S. household income actually went up.

U.S. politicians moved rapidly because they could see the calamity that would result if they didn’t. But pandemic-era policies were also shaped by regrets, which had been building for a decade, over the response to the last crisis in 2008. In hindsight, economists have come to regard that response as lopsided and inadequate. Bank bailouts fixed the financial system, but little was done to help debt-burdened homeowners, and household incomes were allowed to fall.

The new pandemic economics also shielded the financial system, but from the bottom up instead of the top down—a point repeatedly made by Neel Kashkari, who helped lead the rescue as a U.S. Department of the Treasury official in 2008 and who’s now head of the Federal Reserve Bank of Minneapolis. As their jobs vanished in the spring of 2020, Americans struggled to make rent, pay mortgages, and cover car payments. Without the government’s efforts to replace lost income, the health crisis that had already triggered a jobs crisis would have morphed into a financial crisis.

“How have Americans been able to pay all their bills? It’s because Congress has been so aggressive” with fiscal stimulus, Kashkari said in October on CNBC. “If they don’t continue that, these losses roll up into the banking sector, and nobody knows how big those losses will ultimately be.”

After an initial burst of spending, many countries quickly pivoted to reining in their budgets in the years after 2008, driven by concerns about rising public debt—a trend that was most pronounced in Europe. In the U.S., state and local government cutbacks resulted in mass job losses. In both cases, relatively high unemployment and low growth rates persisted for much of the decade.

In 2020 the doctrine of austerity went into rapid retreat all over the world. Germany, where politicians and central bankers have long been obsessed with fiscal discipline, scrapped a rule requiring balanced budgets and dropped its opposition to joint borrowing with other euro-area countries. The IMF noted concerns about rising debt levels but said a bigger risk was that governments would curtail their spending too soon.

In 2008, U.S. policymakers were overly selective about who should and shouldn’t receive aid and erred on the side of doing too little, according to Kashkari. In a Washington Post op-ed article published on March 27, 2020—the same day lawmakers passed the $2.2 trillion Cares Act, the main pandemic stimulus package—Kashkari reflected on those earlier efforts to help homeowners struggling to pay mortgages.

“By applying numerous criteria to make sure only ‘deserving’ families received help, we narrowed and slowed the programs dramatically, resulting in a deeper housing correction, with more foreclosures than had we flooded borrowers with assistance,” Kashkari wrote. “The American people ultimately paid more because of our attempts to save them money.”

By contrast, the logic of pandemic policy went more like this: Clearly no Americans thrown out of work by the pandemic—mostly low-paid workers in restaurants and other service industries—lost their jobs through any fault of their own. This made politicians comfortable supporting a big fiscal response. Unlike the Fed actions that dominated crisis firefighting in the past, government spending landed directly in people’s bank accounts.

Even before Covid-19, the plight of low-paid workers was increasingly a focus of economic policy. The depth of the Great Recession and the slow recovery—it took more than a decade to restore pre-2008 levels of employment—put issues such as economic inequality and racial justice in the spotlight. Wealth and income gaps, especially in the U.S., but in other developed countries, too, have been widening since the 1980s as government intervention in the economy was supplanted by an overreliance on the free market.

Direct payments to low-income households could be a powerful new tool to protect people at the bottom of the economic ladder from the wealth destruction that always accompanies downturns. Now that they’ve been used in one recession, it will be hard to argue that they shouldn’t be used in the next one, according to J.W. Mason, an associate professor at the John Jay College of Criminal Justice in New York.

“If you can replace 100% of the lost income in a crisis like this, why don’t we replace 100% of people’s lost income in every cyclical downturn?” he says. “What is the excuse for saying that because we have some sort of financial crisis—something’s gone wrong in the mortgage market, there’s been a stock market collapse—that ordinary people should see a fall in their living standards?”

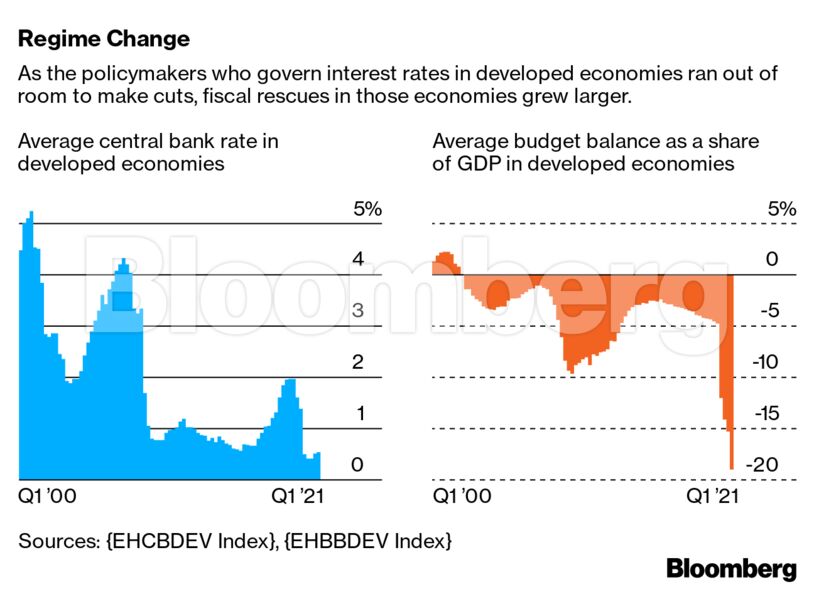

THE PROMINENCE of such transfer payments during the pandemic highlights another big shift in economics: the handover of power from monetary to fiscal policy and the receding role of the inflation-fighting central bank.

In the early ’80s under Volcker, the Fed kept interest rates high to stamp out the double-digit inflation that had taken hold in the previous decade. One effect was to make it prohibitively expensive—in the eyes of policymakers—to pursue social goals by running government budget deficits.

Now, after a long period of declining interest rates and largely absent inflation, the central bank is taking the opposite approach. Fed Chair Jerome Powell and his colleagues have been vocal supporters of deficit spending during the pandemic, and they’ve promised to keep interest rates near zero at least until pre-pandemic employment rates have been restored. In March 2020, as Congress met to authorize the largest fiscal package in history, House Speaker Nancy Pelosi said Powell encouraged her to “ think big” because “interest rates are as low as they’ll ever be.”

Even a year later, with trillions of dollars more spending approved or in the pipeline, the Fed’s message hasn’t changed. As President Joe Biden’s $1.9 trillion pandemic relief bill was passing through Congress in March 2021, Fed officials played down the inflation risks. White House economists say that if their spending plans, including the $4 trillion infrastructure and child-care packages they hope to pass next, do end up causing unacceptable levels of inflation, then the Fed can always step in and clean up the mess.

There’s a heated debate over how big of a risk inflation is. On one side, some economists and Wall Street investors point to households that are flush with cash as a result of pandemic stimulus and savings under lockdown—and itching to get out and spend the money in a reopening economy, as vaccination becomes more widespread. That’s a recipe for an inflationary boom, they say, an argument bolstered by April’s 4.2% inflation rate, the highest since 2008. Bond-market measures of expected inflation over the next five years are also at decade-highs, though after adjustment for the Fed’s preferred gauge they still suggest an inflation rate around where the central bank wants it to be.

Lawrence Summers, who served in the last two Democratic administrations (as treasury secretary under Bill Clinton and as director of the National Economic Council under Barack Obama), says Biden has poured too much money into the economy relative to the size of the hole caused by the pandemic. “You need to be progressive, but you also need to get the arithmetic right,” he said on Bloomberg TV in April. “I am worried that this program could overheat the economy.”

Conservative economists share the inflation concern, but they have a deeper objection to the new direction under Biden and Powell. They think it’s in danger of losing sight of some fundamental laws of economics.

“Fiscal policy has to confront the fact that we do have to pay for things in the long run,” R. Glenn Hubbard, dean emeritus at Columbia Business School who served as chairman of President George W. Bush’s Council of Economic Advisers, said on Bloomberg TV on April 29.

As for the Fed, its low-rates policy may struggle to deliver the desired level of employment in labor markets that are undergoing structural change as a result of the pandemic. “It’s an economy readjusting, and the Fed being easy isn’t going to help that,” Hubbard said. “It’s not really a matter of running the economy hot.”

In the opposite camp are economists in the Biden administration and the Fed, along with most Wall Street forecasters, as well as the investors who buy inflation-protected bonds. They all expect prices to stay relatively contained after a temporary spike.

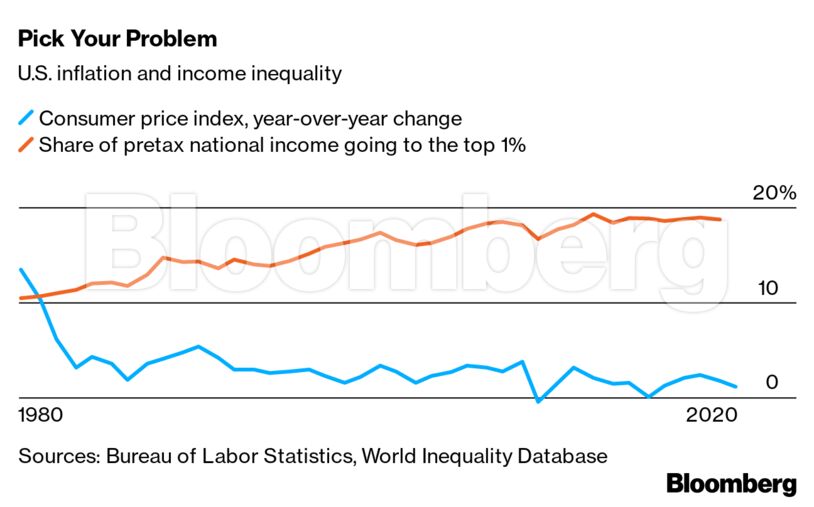

That view has been shaped by the decade before the pandemic. Higher inflation was supposed to show up in the early 2010s, as a result of post-crisis budget deficits and Fed money-printing—and in the late 2010s, when unemployment rates fell to the lowest levels in half a century. But it never did. Inflation has been declining all over the world for decades.

MANY OF THE PEOPLE in charge of central banks, finance ministries, or economics departments have some recollection of the inflationary 1970s and their aftermath. But their offices are increasingly staffed by younger economists who’ve never seen much price instability in the developed world—and who object to the single-minded focus on inflation at the expense of social priorities such as full employment and fairer distribution of income and wealth. These economists are more likely to see inequality as Public Enemy No. 1 than inflation.

That kind of thinking underlies the Fed’s strategy review, which last year resulted in a new framework for setting interest rates. The central bank will let inflation overshoot its target for a while before raising rates instead of taking preemptive action that might risk choking off an economic recovery. The idea is that this will allow the benefits of growth to reach every corner of the economy—even people who typically don’t reap gains until late in an expansion, such as low-wage earners. That’s a reversal from 2015, when the Fed began raising rates even though unemployment among Black Americans was 8.5%, almost double the rate for White Americans.

Biden’s team has embraced the new economics with fiscal proposals designed to combat inequality. He’s proposing higher taxes on the rich and more spending to benefit the poor, policies that have been out of favor since the ’70s. The administration is also backing a higher minimum wage, and there are signs that more generous unemployment benefits during the pandemic—coupled with some workers’ reluctance to return to work during a health crisis—are already pushing employers in low-wage industries to raise wages.

As rich-world policymakers take steps to reduce wealth disparities in their own countries, there’s a danger that the gap between those economies and those of the developing world is widening. Governments in poorer countries can’t spend as freely to help their populations during the pandemic without triggering inflation or scaring off international investors.

The Group of 20, the main international gathering of the world’s wealthiest nations, has supported a suspension of debt service payments for countries that request it, but private bondholders don’t have to accept it. Brazil and Turkey have been forced to raise interest rates to address surging inflation and the threat of capital flight, even though their economies are still getting squeezed by the pandemic.

In a March report, the United Nations Conference on Trade and Development listed some of the ideas that dominated global economic policymaking before the pandemic—“austerity, inflation targeting, trade and investment liberalization, innovative finance, and labor market flexibility”—and described some of their negative effects: “This path led to a world of growing economic inequalities, arrested development, financial fragility, and unsustainable use of natural resources before the pandemic hit.”

Of course, some say the new policies could come with damaging consequences of their own. The Fed’s low interest rates, for example, are often blamed for fueling rallies in assets such as stocks and housing that benefit the rich most and widen the wealth gap.

And while the new economics has the makings of an updated framework to deal with recessions, it has yet to grapple with the potential problems posed by surging growth. Adherents believe that inflationary pressures, the kind that the policy paradigm from 1980 to 2020 was designed to contain, simply aren’t going to arise anytime soon.

If inflation risks do materialize, there’s a debate about how they should be managed. Leaving the job to the Fed and a Volcker-style monetary policy would throw people out of work, hitting the most vulnerable the hardest. That would undermine the goal of achieving a more inclusive economy.

Alternative methods, such as the one advocated by Modern Monetary Theory proponents, are gaining traction. In the view of Stephanie Kelton, a professor at Stony Brook University in New York, the government should use fiscal and regulatory tools to manage inflation instead of the blunt instrument of interest rates. For instance, incentives to manufacturers can help avert production bottlenecks that push prices higher, and payroll taxes can be adjusted when consumer demand needs to be pumped up or reined in.

Post-pandemic, all of these discussions will likely range a little wider and freer than they might have a few years ago.

“We’ve had a generation where we’ve had macroeconomic policymaking dominated by these obsessive fears of doing too much,” says Mason, the heterodox economist. “The fear of inflation lurking around every corner, the fear of government debt passing some poorly specified but frightening limit, the fear that too much assistance to people who are out of work will undermine work incentives.

“In the past year,” he adds, “we seem to have broken out of that mindset.”

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All