Do Wide Divergences in ESG Ratings Doom Investors?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Six competing vendors rate how companies perform along environmental, social and governance (ESG) standards. But because those ratings differ widely across vendors, investors cannot reliably construct portfolios that meet their personal criteria.

Six competing vendors rate how companies perform along environmental, social and governance (ESG) standards. But because those ratings differ widely across vendors, investors cannot reliably construct portfolios that meet their personal criteria.

My August 24 and November 23, 2020, articles for Advisor Perspectives presented evidence from research demonstrating that ESG investors face considerable challenges in allocating assets because the data used to construct ESG portfolios differs widely among providers. The result is that funds may not be aligned with investor objectives and beliefs. In addition, the return and risk of ESG funds can differ significantly and are driven by fund-specific criteria rather than by a homogeneous ESG factor.

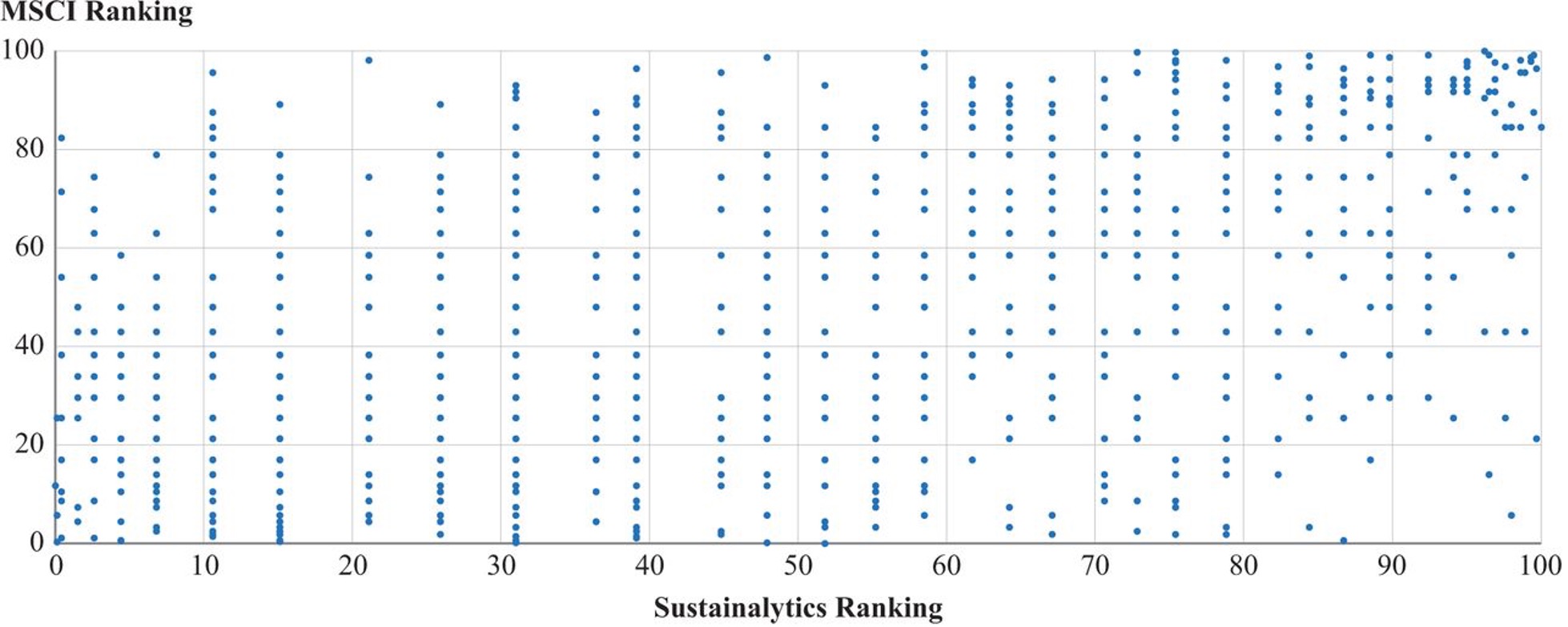

Elroy Dimson, Paul Marsh and Mike Staunton contribute to the ESG literature with their study, “Divergent ESG Ratings,” published in the November 2020 issue of The Journal of Portfolio Management. They found that while data is essential for making investment decisions, and most institutions rely wholly or partly on external providers of ESG data, there is minimal correlation between ESG ratings from alternative agencies. As the following chart that shows ratings from two of the leading raters demonstrates, there is a wide divergence in scores – companies with a high score from one rater often receive a middling or low score from another rater.

MSCI versus Sustainalytics Rankings at Start-2019

Source: Data from MSCI and Sustainalytics for 878 U.S. companies.

The following charts show the rankings of six companies by three providers. Companies can have dramatically divergent rankings by different providers on the same factor. For example, on the environmental factor, Facebook has a 1st percentile ranking by Sustainalytics and a 96th percentile ranking by MSCI.

Source: Data from MSCI, FTSE Russell, and Sustainalytics.

The next chart shows that the pairwise correlations of rankings are quite low. This is especially true for the individual components – for governance, they are virtually uncorrelated.

Source: Data from MSCI, FTSE Russell, and Sustainalytics.

Dimson, Marsh and Staunton explained that the divergences are caused by a variety of factors:

- There is a variety and inconsistency of the metrics that purport to measure much the same thing. The diversity of measures gives rise to considerable dissimilarity in ratings, reflecting firm-specific attributes, differing terminologies, metrics and units of measurement.

- There are differences in how raters define the benchmark for comparisons. For example, Sustainalytics compares companies to constituents of a broad market index, whereas S&P compares companies to industry peers.

- At the company level, ESG ratings are plagued by missing data. When a company does not reveal metrics, some raters assume the worst and assign a score of zero. Others impute a score that reflects peers that do report the data. More sophisticated approaches use statistical models to estimate missing metrics but are often unclear about why a company gets a low or high rating.

- Reflecting the expansion in the volume of public information and the lack of consensus on metrics, there is greater scope for raters to disagree about the scores for particular companies.

- As the following chart demonstrates, weighting schemes vary greatly.

Source: Data from MSCI and Sustainalytics.

Returns to ESG strategies

Dimson, Marsh and Staunton also examined the returns of ESG strategies and concluded that there was little evidence that ESG ratings lead to either outperformance or underperformance. They also noted that, as economic theory predicts, markets learn. They cited the 2001 study, “Corporate Governance and Equity Prices,” by Paul Gompers, Joy Ishii and Andrew Metrick, which found that companies with strong governance related to takeover defenses and shareholder rights had outperformed those with weak governance by 8.5 percentage points over the decade of the 1990s. However, the outperformance has since disappeared. Publication eliminated the anomaly as governance became more reflected in valuations – companies with good (poor) governance received higher (lower) valuations.

Dimson, Marsh and Staunton found the same pattern when they examined the research on corporate social responsibility (the S in ESG). They cited the 2015 study, “The Wages of Social Responsibility – Where Are They? A Critical Review of ESG Investing,” which found that, “the outperformance of a highly rated over a lowly rated portfolio was large and positive from 1990 to 2001, about half the size from 2002 to 2006, and completely absent from 2007 to 2012. This pattern resembles the findings for corporate governance. Investors learn over time, and markets become more efficient at discounting E&S information. The implications of ESG ratings may now be fully reflected in stock prices.”

Economic theory predicts the same pattern for the environmental factor. The hypothesis is that companies with high sustainability scores have better risk management and better compliance standards. The stronger controls lead to fewer extreme events such as environmental disasters, fraud, corruption and litigation (and their negative consequences). The result is a reduction in tail risk in high-scoring firms relative to the lowest-scoring firms. Thus, companies with high (low) sustainability scores should receive higher (lower) valuations. Higher (lower) valuations predict a “sin” premium. However, in the short term there can be conflicting forces at work.

Conflicting forces

Investor preferences lead to different short- and long-term impacts on asset prices and returns. Firms with high sustainable investing scores earn rising portfolio weights, leading to short-term capital gains for their stocks – realized returns rise temporarily. However, the long-term effect is that higher valuations reduce expected long-term returns.

If being a good corporate citizen leads to higher profitability and/or reduced risks, the market incorporates that information quickly into prices. Thus, investors cannot expect to profit from that information. In addition, there should be a “sin” premium, reflecting both investor preferences and risks.

Summarizing their findings, Dimson, Marsh and Staunton concluded, “ESG ratings should not be treated as a black box or used mechanically. Blanket use of ESG scores is not the solution. At best, they are a starting point. Analysts and fund managers need to understand how they are constructed and supplement them with their own scrutiny to build a holistic understanding of a company and hence ensure that their investments best reflect the values of their end-investors.”

In terms of returns, they stated: “For investors, there may well be, or at least have been, financially worthwhile opportunities from investing in companies based on their ESG credentials, at least for a period of time when prescient investors have identified price relevant characteristics that have not been fully recognized by the market. But such benefits are likely to be short-lived thanks to competition from other investors and by peers catching up. We have seen evidence in both the corporate governance and E&S fields that investors learn, and that this learning is in due course reflected in valuations, making markets more efficient.

“For a long-term investor, the perspective we take is that we lack unambiguous evidence that ESG screening enhances expected return or reduces risk. This remains true whether we look at the performance of companies based on their ratings or at ESG funds or indexes. Equally, however, we find no strong evidence of underperformance. For ESG investment strategies based on exclusions, the theory and evidence available so far suggest that the sacrifice made by ESG investors is a slight shortfall in expected return and a minor reduction in diversification. The price for ethical principles appears small, and one that many virtuous investors may be content to bear.”

While Dimson, Marsh and Staunton did not find unambiguous evidence of underperformance, that could reflect that the market has not yet reached a new equilibrium, as the increased demand for ESG style investing is still driving valuations. At some point, investor preferences, as well as the known risks, should be fully reflected in prices. At that point, a “sin” premium should persist – a premium that ESG investors should be prepared to accept.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners.

Important Disclosure: The information contained herein is for educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. The analysis contained is be based on third party information and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely at your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products, or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. R-20-XXX

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All