The GAO Takes on Target-Date Funds

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Two Congressional chairs have authorized a review of target-date funds (TDFs). The last such review was in 2009, and all that changed was that risk increased. It would be a shame if this initiative failed to produce results

On May 6, 2021, Senator Patty Murray (D-WA), chair of the Health, Education, Labor, and Pensions (HELP) committee, and Rep. Robert C. “Bobby” Scott (D-VA), chair of the House Education and Labor Committee, sent a letter to Gene Dodaro, comptroller the GAO. They were seeking answers to 10 questions dealing with concerns that some aspects of target-date funds (TDFs) may be placing American retirement savers at risk. They wrote:

…we write to request the General Accountability Office (GAO) conduct a review of target-date funds (TDFs). The employer-provided retirement system must effectively serve its participants and retirees, and we are concerned certain aspects of TDFs may be placing them at risk.

In the following and in this video I answer those 10 questions. The official answers will come from the GAO, but leave your comments on this article as to whether you agree with my answers.

Most of our 78 million baby boomers will spend much of this decade in the risk zone, when investment losses can irreparably spoil the rest of their lives. It is a risk with the potentially dire consequence of depleting lifetime savings that cannot be replenished with paychecks. Nor is there enough time to recover with investment gains. I wrote the book, Baby Boomer Investing in the Perilous Decade of the 2020s, to warn and protect boomer’s lifetime savings. Even “poor” baby boomers can live reasonably well, but not if they lose their lifetime savings.

Here are the 10 questions posed by Murray and Scott and my answers:

1. What percentage of total defined contribution (DC) plan assets are invested in TDFs? What percentage of plan participants are offered, and participate in, TDFs? What percentage of plan participants defaulted into TDFs?

According to Investopedia, as of 2020, more than 50% of 401(k) investors have all of their 401(k) assets in TDFs. More than 75% of investors have a portion of their money (retirement or non-retirement) in at least one TDF.

2. To what extent have participants approaching retirement age who are invested in TDFs been affected by market fluctuations as a result of the COVID-19 pandemic? How much variation is there in the performance of TDFs of the same vintage (i.e., target retirement year), particularly for TDFs at or near the target retirement date? To what extent have TDF providers taken steps to mitigate the volatility of TDF assets?

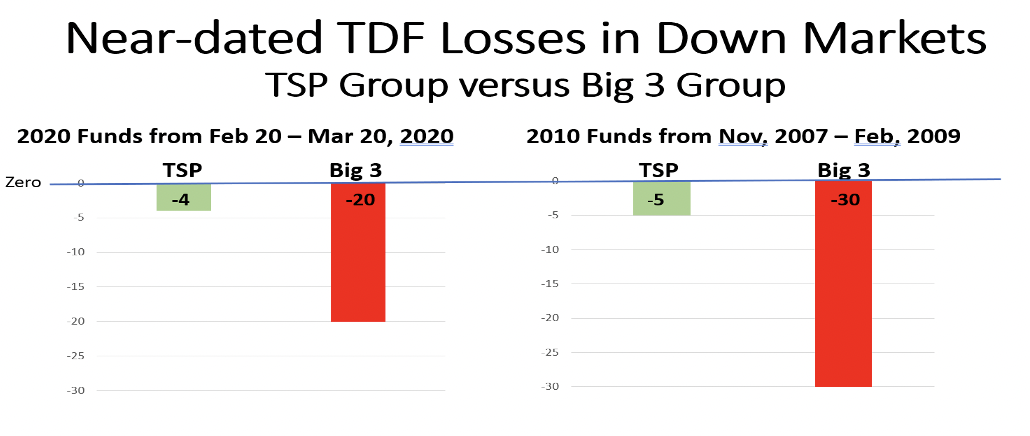

The Congressional letter singled out the federal Thrift Savings Plan (TSP) as an example of a plan that has defended well in market turbulence. With six million beneficiaries and $800 billion in assets, the TSP is the largest defined contribution plan in the world. And as a federal plan, Congress should at least consider the TSP as TDFs, in a category called “LfFunds.”

There are two distinct groups of TDFs. One group is very conservative at the target date and the other group is substantially more aggressive. The conservative group is anchored by TSP and has members like the SMART TDF Index and the Office and Professional Employees International Union (OPEIU). The TSP group has $200 billion in TDF assets.

The other group is anchored by the “big three” TDF providers – Vanguard, Fidelity and T. Rowe Price – they collectively manage $1.5 trillion in TDF assets.

As shown in the following graph, the TSP group of conservative TDFs defended wealth in the COVID crisis and in the 2008 market collapse. By contrast, the big three group lost 20% in the COVID crisis and 30% in 2008. Professor Craig Israelsen opines, “A target-date fund that fails to protect account value as the target date approaches has failed in its primary task.”

Big three TDFs cannot and have not withstood major stock market turbulence, but the TSP group can and has. The answer to question four explains why.

3. How often do investors with default investment TDFs in their DC plans reassess their investments, and what, if any, is the cost of a passive investment stance in a tumultuous market? Are TDFs properly structured to withstand major stock turbulence?

Investors do not choose TDFs. Plan sponsors choose them, and rarely, if ever, reassess. See answer to question two for exposure to market turbulence

4. How does the asset allocation and fee structure vary across those TDFs used as default options in 401(k) plans? How do TDF fee structures compare with other investment products? In the years approaching retirement (i.e., age 55 and older), to what extent do TDFs shift the allocation of equities to more conservative investments like fixed income in order to protect these participants from losses near retirement?

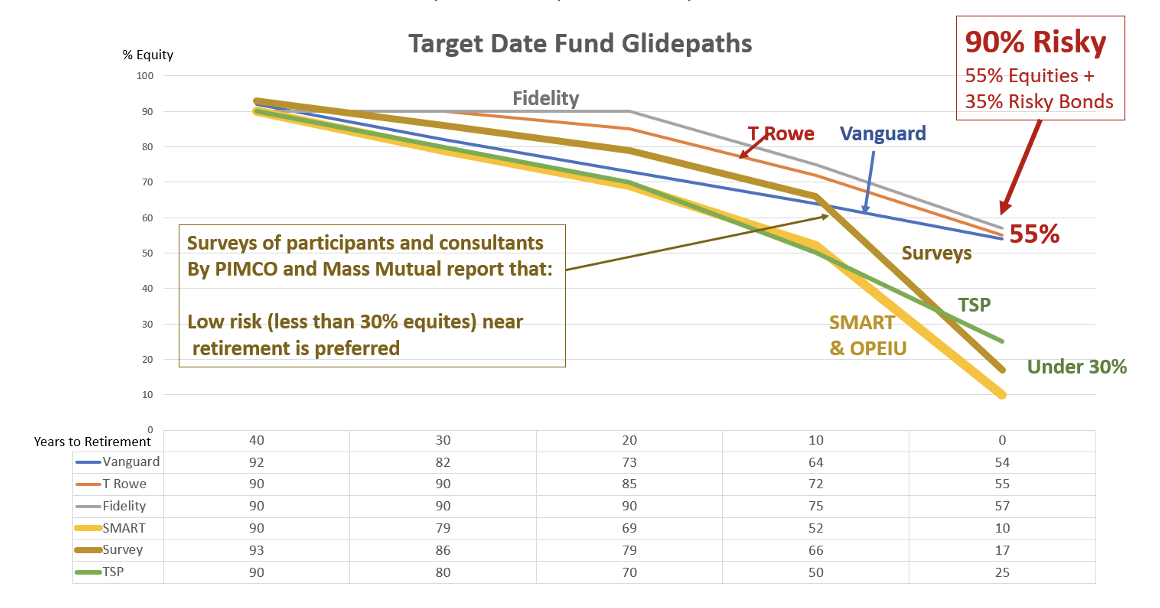

Fees average about 65 basis points, which is fairly low due mostly to successful lawsuits over excessive fees. The following picture shows glidepaths and contrasts them to surveys of beneficiaries and advisors by PIMCO and Mass Mutual. These surveys report a strong preference for conservatism near the target date, in line with the TSP group.

There is a clear difference of opinion that pertains to question nine.

5. How are TDFs marketed and advertised? Are participants sufficiently aware of the cost and asset allocation variation among TDFs?

Participants are generally unaware of TDF costs and allocations because they do not choose TDFs. TDFs are marketed to plan sponsors as one-size-fits-all-set-it-and-forget-it Qualified Default Investment Alternatives (QDIAs). They are the most popular choice of default investments because most plans use TDFs, and they seem so simple.

6. What percentage of plan sponsors select off-the-shelf TDFs? What percentage of plan sponsors select custom TDFs? Is there a material difference in the performance of off-the-shelf versus custom TDFs?

A 2019 Callan Associates survey reported that 87.3% of institutional defined contribution (DC) plans use target date strategies as their default investment vehicle and that 17.3% of plans are using “custom” target date strategies. Custom TDFs are a money grab by consultants. Morningstar finds little difference in their performance versus off-the-shelf

7. To what extent do TDFs include alternative assets, such as hedge funds or private equity? What information is typically available to participants and plan sponsors about the risks and benefits of asset allocations in TDFs? How do plan sponsors select and oversee TDFs to ensure these funds have a suitable risk level for participants?

There is little use of alternatives, mostly because they are expensive. Fund prospectuses are readily available so anyone can see risks and benefits, but these are rarely viewed. The answer to the next question addresses suitability.

8. What steps has the U.S. Department of Labor (DOL) taken to ensure that plan sponsors appropriately select and use TDFs and that sponsors provide appropriate information and education about these funds to plan participants?

The DOL has issued certain tips for TDFs, but it has left it to the industry to establish standards. There are trade-offs across TDF glidepaths between growth and safety . At long dates for young employees, growth is the appropriate emphasis, but there is substantial disagreement at the target retirement date.

DOL guidance says TDFs should be chosen based on the demographics of the workforce. This guidance should be directed to the demographics of defaulted beneficiaries since most TDF assets are those of defaulted participants. These beneficiaries have only one demographic in common: they are financially illiterate. The TSP group claims that these naïve beneficiaries need protection, so the risk of loss should be exceptionally low near the target date. Retirement researchers define a “risk zone” spanning the five to 10 years before and after retirement. Losses in this zone can spoil the remainder of life, even if markets subsequently recover. The TSP group believes that safety is paramount at the target retirement date. That is their standard.

By contrast the big three group operates as though people have not saved enough and they’re living longer so they need to earn more on their investments. More on this in the “goals” section below. As we approach retirement, whatever we’ve saved has to be “enough” because that’s all there is; paychecks stop. We make plans to make “enough” last a lifetime. Losing a significant part of “enough” is life altering. The big three standard is to compensate for inadequate savings with investment returns.

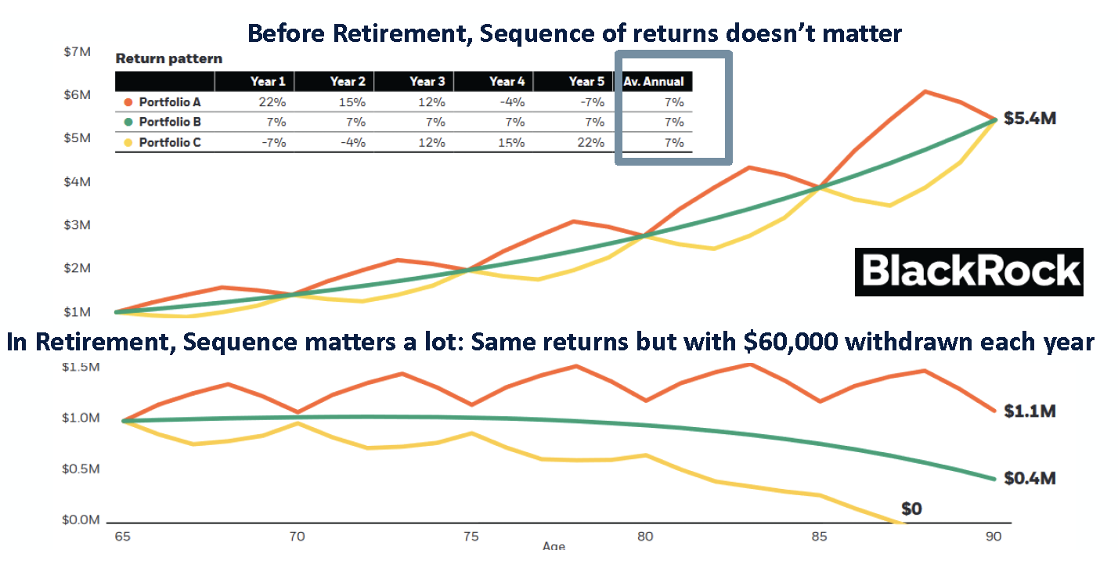

TDF providers do not make unsuspecting participants aware of the enormous risk of outliving one’s assets. At a minimum, the GAO should recommend a disclosure on this critical risk. Providers do not do so. Unknowing beneficiaries are exposed to Sequence-of-returns risk.

9. When provided the option to invest in TDFs alongside an array of other investment fund options, how often and to what extent do plan participants rely primarily – or exclusively – on TDFs? In these scenarios, how many investment alternatives are provided? How many TDFs do plan sponsors generally offer in their investment options?

Most assets in TDFs are there by default so participants are not considering TDFs against an array of options. Most sponsors offer only one TDF, but a plan could offer TDF choices to non-defaulted participants. For example, the OPEIU plan offers participants a choice of conservative, moderate or growth glidepaths. The conservative path is the default.

10. What are possible legislative or regulatory options that would not only bolster the protection of plan participants, who are nearing retirement or are retired, but also achieve the intended goals of TDFs?

There is significant disagreement on what the goals of TDFs should be. The big three advertise goals of replacing pay and managing longevity risk. These are goals best achieved with adequate savings.

By contrast the TSP group’s goal is to deliver at retirement accumulated savings plus reasonable growth. This goal acknowledges their lack of control over savings.

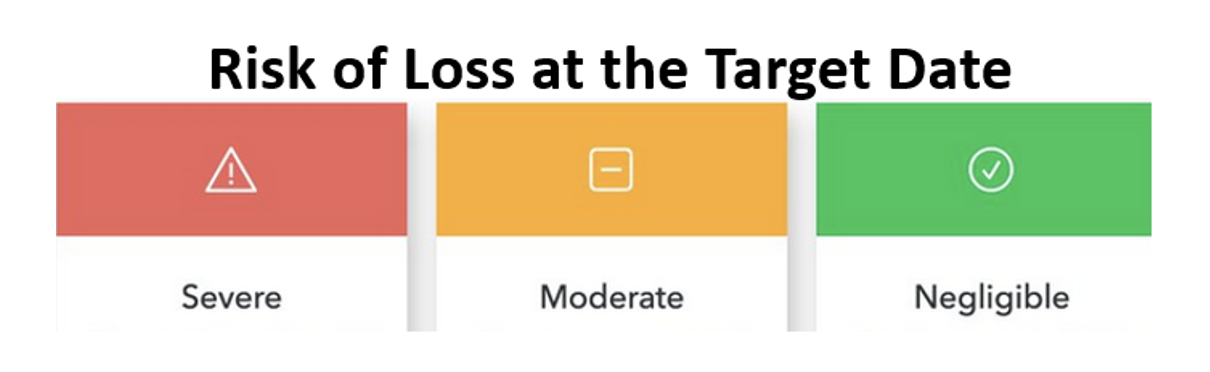

I recommend that Congress require clear and simple disclosures of TDF risk at the target date, developing rules/standards for straightforward risk assignments to negligible, moderate and severe risk of loss at the target date. Congress should appoint a committee to develop these standards, and investment companies should be required to report the resulting risk assignment in fund names: for example, “The ABC 2050 Fund with Moderate Risk of Loss at the Target Date.” Only negligible-risk TDFs should be chosen as QDIAs, with moderate and extreme versions offered as options to non-defaulted beneficiaries. Congress might not want to mandate acceptable risk for QDIAs, but it should require a standardized risk disclosure that it regulates.

Conclusion

Kudos to Chairpersons Murray and Scott for taking this initiative, proactively seeking to protect TDF beneficiaries. I look forward to seeing the GAO report.

Ron Surz is CEO of Target Date Solutions, Age Sage, GlidePath Wealth Management, and co-host of the Baby Boomer Investing Show that you can binge watch on Patreon.

Please watch and support our Baby Boomer Investing Show on Patreon and visit our Baby Boomer Libraries, our Target Date Fund blog, and our GlidePath blog.

For more guidance please see Bursting Bubbles Blast Baby Boomers and How to Minimize the Impact of Inflation, Recessions, and Stock Market Crashes.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All