Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“It’s different this time” is usually not true, but this time it is. Will we get amplifying extremes, or returns toward average? The feasible and likely scenario spells disaster.

It’s usually not true when someone says, “It’s different this time.” But it is true this time:

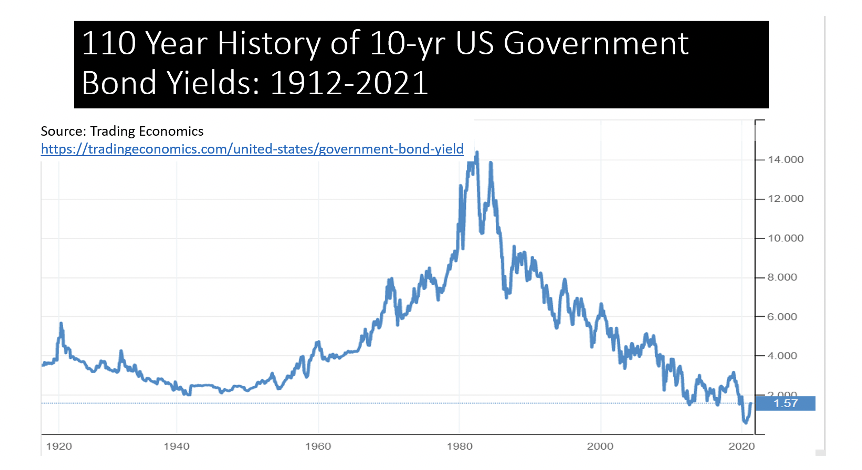

- Interest rates have never been lower.

- The U.S. government has never printed more money.

- Stock prices have never been higher.

- The wealth divide in the U.S. has never been wider.

- There has never been 78 million people simultaneously in the investment risk zone. Baby boomers are in the stage of their lives when their primary investment objective should be protecting their lifetime savings.

These are challenges that most people, especially baby boomers, are not prepared to deal with because most are not educated in finance and investing. Will Rogers said, “Everyone is stupid, but about different things.”

What could possibly go wrong? Here are the five possibilities:

- Low interest rates

The government is implementing a zero-interest rate policy (ZIRP). Unlike the past, retirees cannot earn a decent return on safe investments, so they’ve been forced into risky assets like stocks and risky bonds.

This manipulation is accomplished by Federal Reserve purchases of mass amounts of government bonds, financed with new money – money printing.

- Money printing

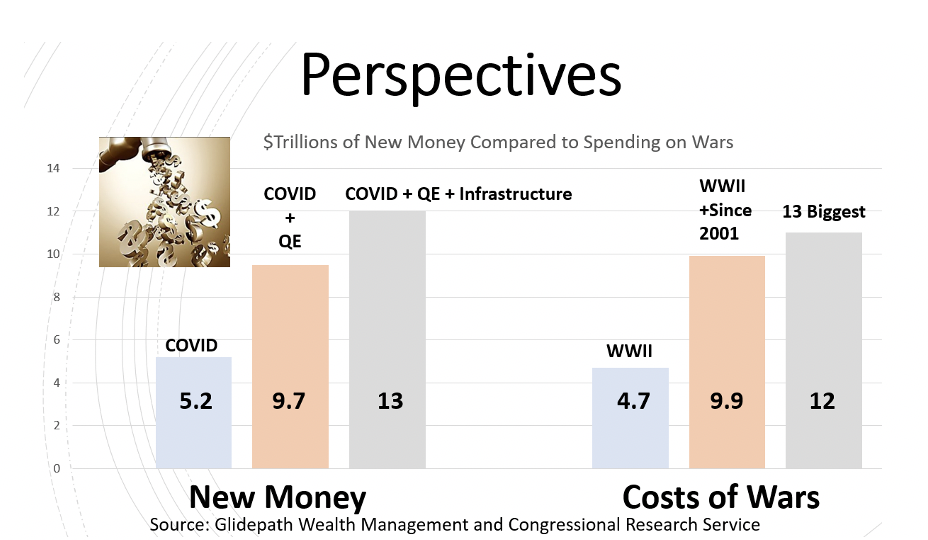

The U.S. government has spent $13 trillion (and more coming) in new money. For perspective, this is more than was spent on our 13 largest wars combined. World War II cost $4.7 trillion in today’s dollars.

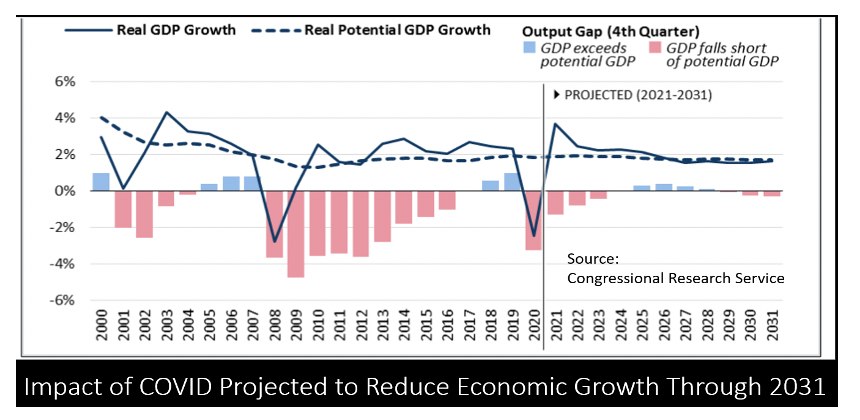

The U.S. government is poking the inflation bear, printing more and more until something breaks and relying on Japan’s experience in even more money printing.

Inflation undermines the value of savings. It could pop the stock market bubble. See “What Could Possibly Happen?” below.

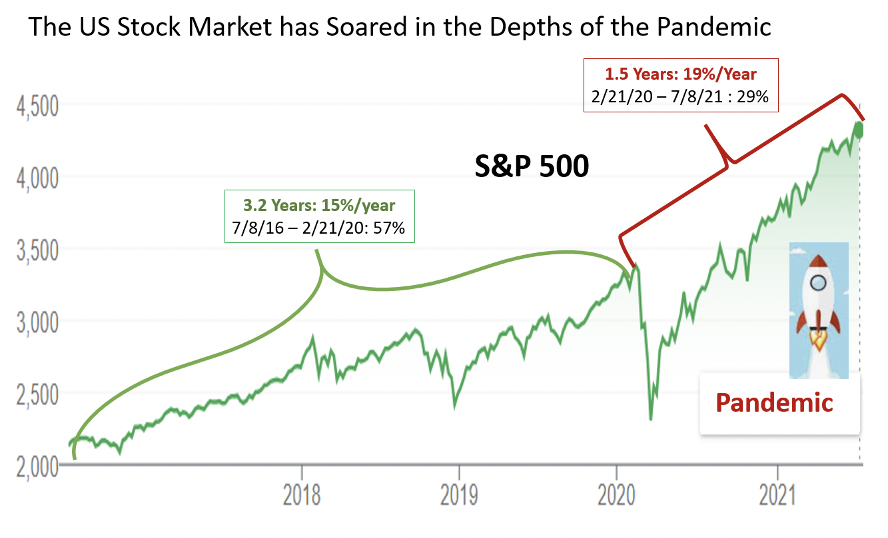

- Stock market bubble

Bubbles are usually identified after they burst. This one is unique in its ability to persist in the throes of the COVID pandemic.

The average S&P annual return over the past 95 years was 10%. It has earned twice that return (19%) in the face of COVID, despite a 30% loss in the month ending March 23.

Investor psychology (madness?) is the most likely explanation, including a belief in a rapid recovery even though experts forecast that COVID will impact the economy for the next decade.

Millennial investors have never suffered a market crash, but they are experiencing one of the consequences of money printing and quantitative easing, namely enriching the rich.

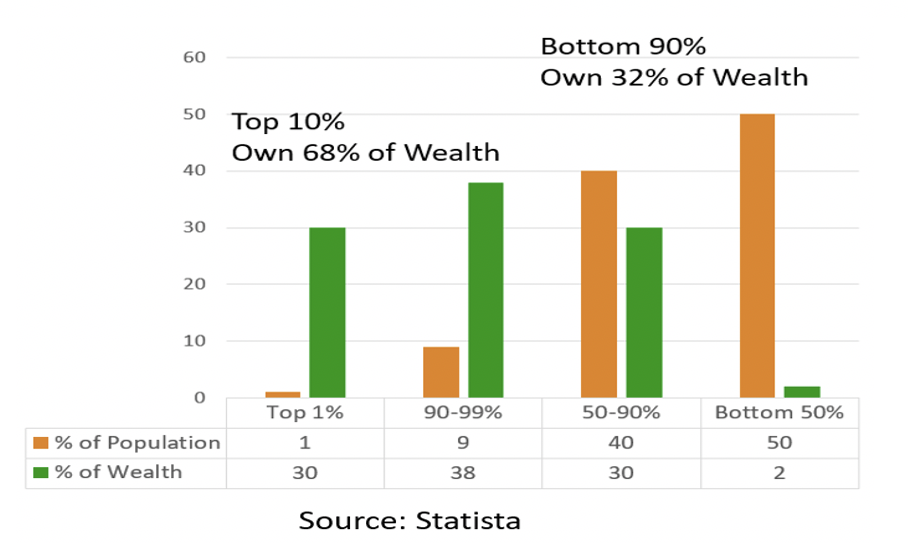

- The great wealth divide

Although the poor in the U.S. are better off than many in countries, the gap between rich and poor is huge, as summarized in the following:

Consequently, there is social unrest around the country, particularly in Seattle, Portland and Chicago. The not-so-rich are demanding more, and the government is responding with more free stuff, leading us down the path to socialism.

- Baby boomers in the crosshairs

Baby boomers are the first generation to be responsible for the investment of their savings. Previous generations were mostly covered by defined-benefit pension plans where employers made all the investment decisions. Unfortunately, baby boomers are invested 60/40 stocks/bonds on average. This is a mistake for most because baby boomers are in the “risk zone” spanning the 5-10 years before and after retirement when investment losses can irreparably ruin the rest of their lives.

Most importantly, baby boomers should not “stay the course” as they are frequently advised. Most are on the wrong course and exposed to serious investment losses at this most critical time in their investment life. There are no do-overs.

What could possibly go wrong?

Danger does not always lead to disaster. The five reasons above for concern might be resolved, but here is one realistic scenario. There are others.

Possible scenario

- Massive money printing brings inflation. This is a controversial but feasible outcome.

- Inflation forces interest rates to rise, eliminating ZIRP.

- Rising interest rates cause stock prices to fall because (1) forecasted earnings are discounted at a higher rate and (2) bonds become competitive to stocks again.

- Interest service on government debt increases, forcing reductions in other spending like Social Security and Medicare, and leading to a “debt spiral” of even more money printing.

Conclusion

Baby boomers should be protecting themselves regardless of the threats. This protection should include inflation. The next correction could last long, say a decade. Non-boomers are likely to come through the next correction, but it could take a long time.

I wrote “Baby Boomer Investing in the Perilous Decade of the 2020s” to educate boomeers on protecting their lifetime savings: save and protect.

Ron Surz is co-host of the Baby Boomer Investing Show and president of Target Date Solutions and Age Sage, and CEO of GlidePath Wealth Management

Read more articles by Ron Surz