Credit interval funds have become popular among advisors looking to increase the yield on their fixed-income allocations. New research illustrates the difficulty in quantifying the underlying fees in those investments.

Credit interval funds have become popular among advisors looking to increase the yield on their fixed-income allocations. New research illustrates the difficulty in quantifying the underlying fees in those investments.

Since the great financial crisis, there has been a fundamental shift in the fixed income landscape. Banking regulations implemented in 2008 limited the ability of traditional banks to make loans to U.S. middle-market businesses (generally defined as companies with EBITDA of $10 million to $100 million, those too small to access capital in broadly syndicated markets). The result was that non-bank lending, led by institutionally funded independent asset managers, emerged as a growing and formidable lending channel.

Characteristics of middle market loans

Loans typically have a five- to seven-year maturity and charge floating LIBOR-based rates (with a 1% floor) plus an interest rate spread to compensate for credit risk. Interest spread varies depending upon the perceived riskiness of the borrower, industry, loan-to-value ratio, seniority, covenants and other factors. Lenders also receive an “original issue discount” or “OID,” a one-time upfront fee for originating and underwriting the loan, typically 1 to 3% of the principal.

Private credit exposure can be a viable option for some investors seeking income in the current low interest rate environment. For example, as of July 16, 2021, while Vanguard’s High-Yield Corporate Fund (VWEHX), with a duration of about 2.7 years, was yielding about 4.3%, the largest private credit interval fund, PIMCO’s Flexible Credit Income Fund (PFLEX), with floating rate loans, was yielding about 3.5 percentage points more.

Unfortunately, not all credit interval funds offer the same value. Therefore, you should look beyond a shiny exterior and assess true value. My colleague, Sheldon McFarland, reviewed a June 2021 paper by Cliffwater LLC, which manages the second-largest private credit interval fund (CCLFX), that did just that and showed that credit interval funds can have significant variability in both asset mix and expense ratios, resulting in some funds offering more value to investors. (Disclosure: Buckingham Strategic Wealth includes CCLFX in many client portfolios.)

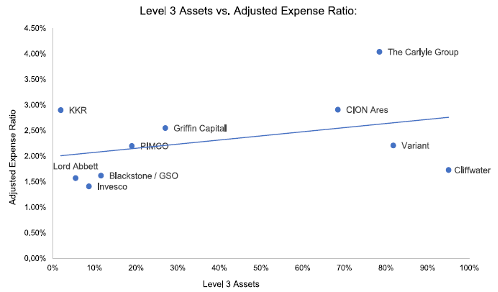

Cliffwater examined the 10 largest credit interval funds and found major differences in fees and private asset exposure. When examining credit interval fund fees, it is important to look beyond published expense ratios, which include the interest costs of leverage but not the interest income, to get a “true” picture of the ownership cost of these funds. It is also important to analyze the makeup of the lending portfolio to determine the amount allocated between public and private credit exposure, as the cost for private credit exposure should be less than that of managing public credit. To help investors differentiate among fund holdings, credit assets are split into three levels:

Level 1: Unadjusted quoted prices are available in active markets for identical securities.

Level 2: Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These observable inputs could include quoted prices of similar assets, or quoted prices of the same asset where trading activity may be otherwise limited or even absent (i.e., unlike Level 1 quoted prices).

Level 3: Unobservable pricing inputs that reflect the entity’s own assumptions regarding the pricing of fair value.

The chart above from the Cliffwater paper shows the amount of private credit measured by the amount of Level 3 assets plotted against the adjusted expense ratio for the 10 largest credit interval funds. Adjusted expense ratios, which are a measure of the “true” cost of fund ownership, ranged from 1.41% on the low end to 4.04% on the high end, with an average of 2.31%. In addition to the wide range of expenses, the Cliffwater paper also found major differences in private asset exposure ranging from 2% to 95%, with an average of just 40%. The chart shows that there is substantial variability between the true ownership cost and the amount of private credit for the 10 largest private credit funds.