New research shows that funds that with an environmental, social and governance (ESG) mandate have factor exposures that differ significantly from the market, creating a challenge for investors who seek a specific factor loading for their overall allocations.

New research shows that funds that with an environmental, social and governance (ESG) mandate have factor exposures that differ significantly from the market, creating a challenge for investors who seek a specific factor loading for their overall allocations.

ESG considerations in investing have become mainstream. According to the Global Sustainable Investment Alliance, ESG investing now accounts for more than $12 trillion, one out of every four dollars under professional management in the U.S., and one out of every two dollars in Europe.1

Ananth Madhavan, Aleksander Sobczyk and Andrew Ang, authors of the study, “Toward ESG Alpha: Analyzing ESG Exposures through a Factor Lens,” published in the first quarter 2021 issue of the Financial Analysts Journal, examined how ESG attributes are linked to common equity factors. They began by noting, “if certain ESG scores are linked to positive, rewarded factor exposures, those ESG components are more likely to be associated with high excess returns. Investors might prefer managers whose ESG characteristics are associated with factors’ long-run risk-adjusted returns, which provides transparency into the economic sensibility for positive performance.” A second benefit is that analyzing factor exposures allows an investor to more properly measure risk-adjusted performance. For example, the authors explained, “If ESG-friendly funds have low returns in excess of their benchmark, they still might be beating those benchmarks on a risk-adjusted basis. Measuring how factor exposures are related to ESG scores allows investors to make these risk-adjusted comparisons.”

Using a data sample that included 1,312 U.S. active equity mutual funds with $3.9 trillion in assets under management (93% of assets in the active fund industry), they investigated the relationship between a fund’s bottom-up, holdings-based (as well as a time-series regression-based approach) ESG score and its alpha and factor loadings. They used holdings from June 30, 2014, to June 30, 2019, at a quarterly frequency. Their ESG data are from MSCI. Active returns were defined as fund returns minus prospectus benchmark returns and were measured net of fees. For their factor analysis, they used seven long-only factor portfolios, proxied by the following MSCI indexes:

- Value: MSCI USA Enhanced Value Index

- Size: MSCI USA Risk Weighted Index

- Quality: MSCI USA Sector Neutral Quality Index

- Momentum: MSCI USA Momentum Index

- Minimum volatility: MSCI USA Minimum Volatility Index

- Large-cap multifactor: MSCI USA Diversified Multiple-Factor Index

- Small-cap multifactor: MSCI USA Small Cap Diversified Multiple-Factor Index

Their analysis included examining results compared to both long-only (for investors who are constrained) and long-short factors, and the use of the Fama-French-Carhart four-factor model (beta, size, value and momentum) and the AQR six-factor model, which adds the BAB (betting against beta) and QMJ (quality minus junk) factors. Following is a summary of their findings using their holdings-based analysis:

- The mean active return across all funds was -1.19% per year. Weighted by AUM, however, this figure was -0.33% – larger funds had higher active returns.

- The overall negative return was driven by negative average active returns in eight of the nine style boxes – the only exception was small-cap growth.

- The mean expense ratio (unweighted) was 0.87%, and weighted by AUM, 0.60%.

- There was little dispersion in average ESG scores across the style boxes.

- The correlation between active returns and ESG scores was slightly negative (-0.06). There was, however, more of a relationship between active return and weighted carbon intensity, as funds with the highest active returns had significantly lower carbon intensity scores – 85.1 carbon emissions per dollar of sales versus 164.2 for the other nine deciles.

- Funds with significantly high ESG attributes – both as to aggregate ESG measures and to separate “E,” “S” and “G” components – had factor exposures that differ from the market in important respects.

Following is a summary of their time-series regression-based analysis:

- There were only small differences in the factor loadings of funds that scored high in terms of ESG metrics. And there was no relationship between active return and ESG score.

- The highest ESG decile funds generally had lower exposure to the market beta and less volatility, more focus on large companies and negative exposure to value.

- There was no significant relationship with security selection alpha or the Idiosyncratic ESG components not related to style factors.

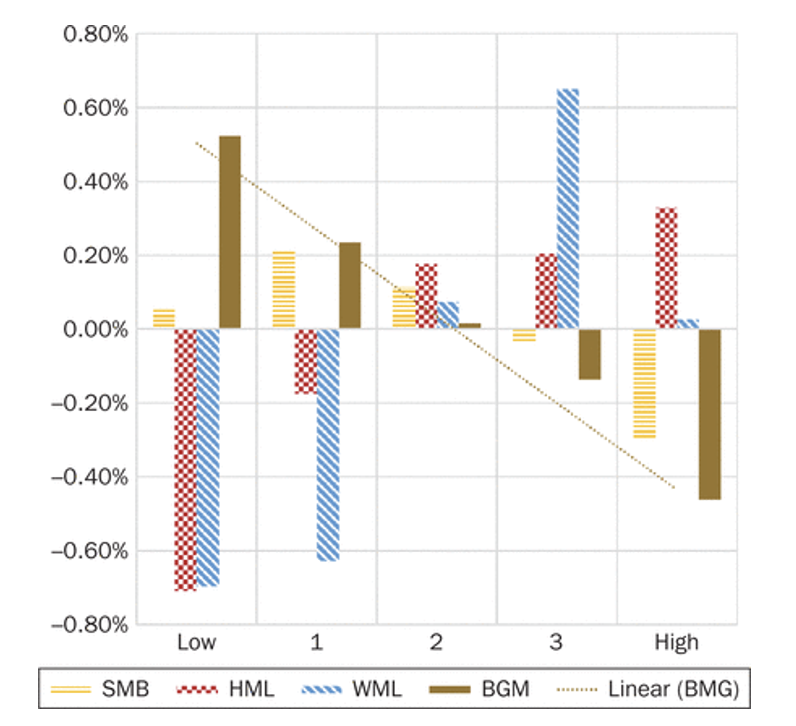

While noting that their sample covered only a short period, their findings led Madhavan, Sobczyk and Ang to conclude: “ESG outcomes are correlated with style factors – value, momentum, quality, minimum volatility, and size – and that funds with high ESG scores exhibit interesting patterns in relation to factors. In particular, funds with high environmental scores have particularly strong exposures to quality and momentum factors. We showed that fund alphas and active returns are linked to Factor ESG components, but we found no link between fund alphas and active returns to ESG components unrelated to style factors.”

Their finding that factor exposures explain much of the returns of ESG portfolios is consistent with the findings of Maximilian Görgen, Andrea Jacob, Martin Nerlinger, Ryan Riordan, Martin Rohleder and Marco Wilkens, authors of the 2019 study, “Carbon Risk.”

SMB (small minus big, the size factor); HML (high book-to-market minus low book-to-market, the value factor); WML (winners minus losers, the momentum factor); BMG (brown minus green, the carbon factor).

Takeways

For those investors seeking to build ESG portfolios, the main takeaway is that when you select funds with high ESG scores, those funds will tend to have significant factor exposures. Investors need to be aware of how ESG considerations may lead to factor tilts that differ from the market as a whole. Differences in factor exposures can lead to tracking variance regret, and the abandonment of even a well-thought-out plan, when the returns to those factors are negative. However, to the extent that factor exposures are desired, they may, over the long run, provide higher returns associated with the factor premiums. However, if the exposures are not desired, investors will need to adjust their portfolios while trying to maintain their ESG score. This highlights the importance of performing deep due diligence when selecting funds for an ESG-oriented portfolio.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners.

The information presented herein is for educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Certain information may be based on third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Performance is historical and does not guarantee future results. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party Web sites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of the Buckingham Strategic Wealth® or Buckingham Strategic Partners® (collectively Buckingham Wealth Partners). LSR-21-38

1Depending on how you identify ESG assets, those numbers are considerably less.

New research shows that funds that with an environmental, social and governance (ESG) mandate have factor exposures that differ significantly from the market, creating a challenge for investors who seek a specific factor loading for their overall allocations.

New research shows that funds that with an environmental, social and governance (ESG) mandate have factor exposures that differ significantly from the market, creating a challenge for investors who seek a specific factor loading for their overall allocations.